A generation that has significantly shaped the world as we know it, the Baby Boomers, are now stepping into the next phase of their lives – retirement. They are making waves in the retirement narrative, drastically shifting societal and economic patterns.

In this blog post, we delve deep into the intriguing phenomena of Baby Boomer retiring statistics, their implications, and the surprising trends that emerge. Whether you’re a Baby Boomer yourself, a concerned family member, a policy maker, or simply a curious observer, this comprehensive exploration promises enlightening insights into this significant generational shift.

The Latest Baby Boomer Retiring Statistics Unveiled

The number of retiring baby boomers will double over the next decade to 10,000 a day.

Diving into the world of Baby Boomer Retirement Statistics, one number surges ahead, commanding attention like a blinking neon sign. Picture this – the count of retiring baby boomers is set to skyrocket – yes, double is the term – in the mere span of a decade to reach an astounding 10,000 a day.

This escalating digit isn’t just a statistic, it’s a pulsating, vivid forecast of a seismic shift in the demographic landscape that will have ripple effects on economies, healthcare services, real estate markets, and indeed, the fabric of our society. So, as we dissect the figures and trends of baby boomer retirements, this augury of what’s to come adds a potent perspective, vital for understanding the magnitude and implications of this generational transition.

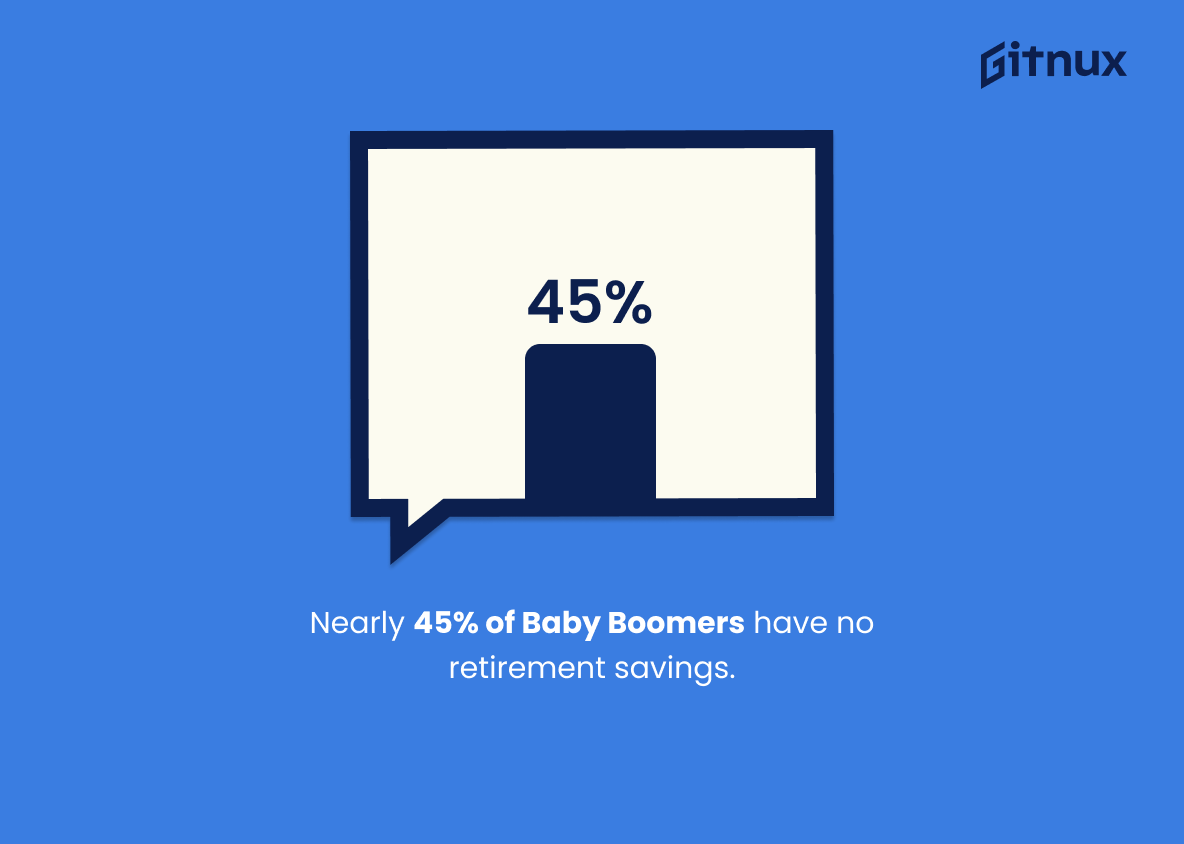

Nearly half (45%) of Baby Boomers have no retirement savings.

Delving into the world of Baby Boomer retiree statistics, the revelation that a staggering 45% of Baby Boomers have no retirement savings is a veritable iceberg in seemingly calm waters. This number signifies almost half of an entire generation nearing retirement age that could potentially face financial struggle. In essence, devoid of any nest egg, they are inadvertently sprinkling uncertainty onto their golden years.

This intriguing data point lights a beacon on the necessity for enhanced financial planning, indicating a possible systemic issue that needs immediate attention. Moreover, it underscores the potential socio-economic challenges looming on the horizon – from increased reliance on government-funded programs to potential inadequacies in the quality of life among retiring Boomers. This single statistic tells a story – a tale of potential financial hardship, that unfurls a destined roadmap for upcoming generations, and adds fuel to the burning discussion needed around retirement readiness.

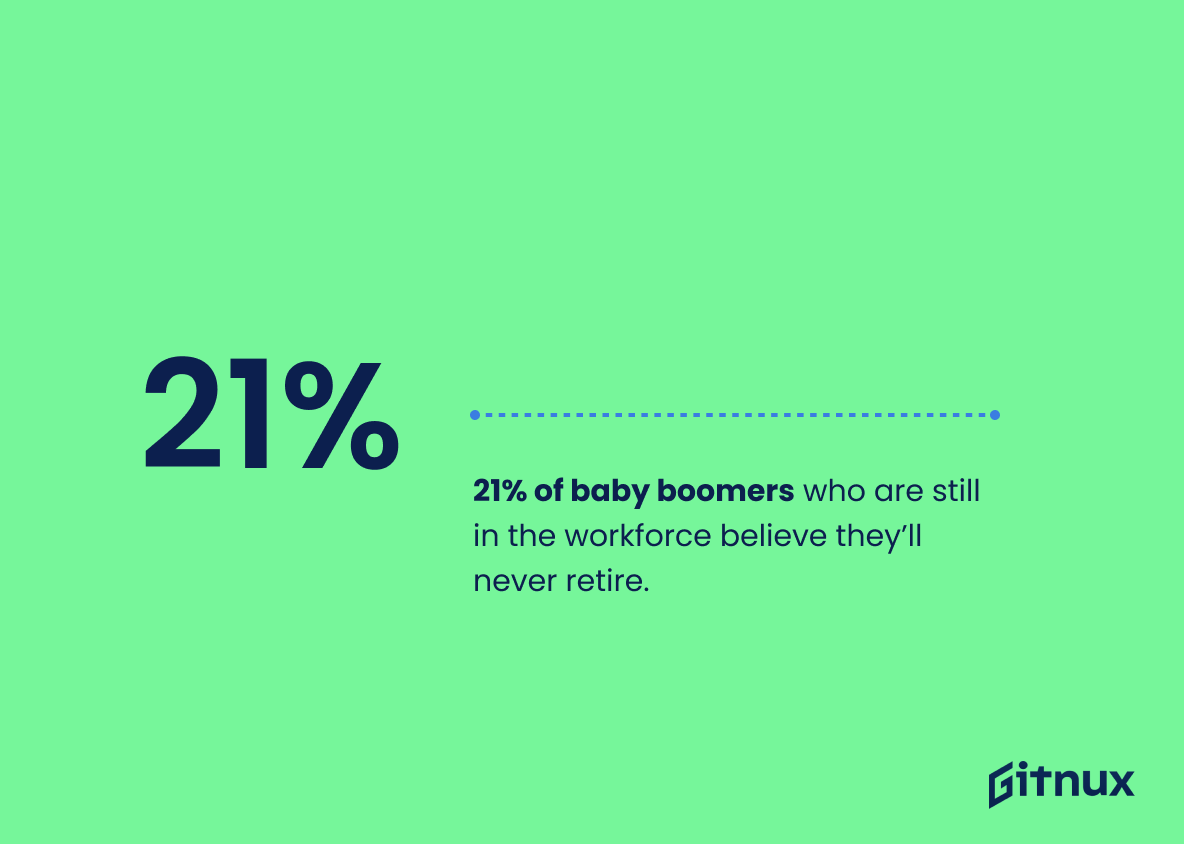

21% of baby boomers who are still in the workforce believe they’ll never retire.

The illumination of this numeric gem, indicating that 21% of baby boomers in the workforce envision a perpetual tenure in their jobs, triggers profound implications for our understanding of retirement trends among this populous generation. Within the canvas of Baby Boomer Retiring Statistics, it paints a telling picture, giving the blog post an intense hue of credibility and relevance.

It underscores the wave of change rippling through this demographic, highlighting the shift from traditional retirement plans to a new era of indefinite employment. It leaves thoughtful echoes regarding the perpetuity of work, the economic strain of retirement, or perhaps, these boomers’ undying enthusiasm for their professions. This percentage hence doesn’t just sit as a numeric factoid but pulses as a concrete testament to the intricacies of the boomer retirement narrative, making it an invaluable piece of the puzzle for readers keen to understand this phenomenon.

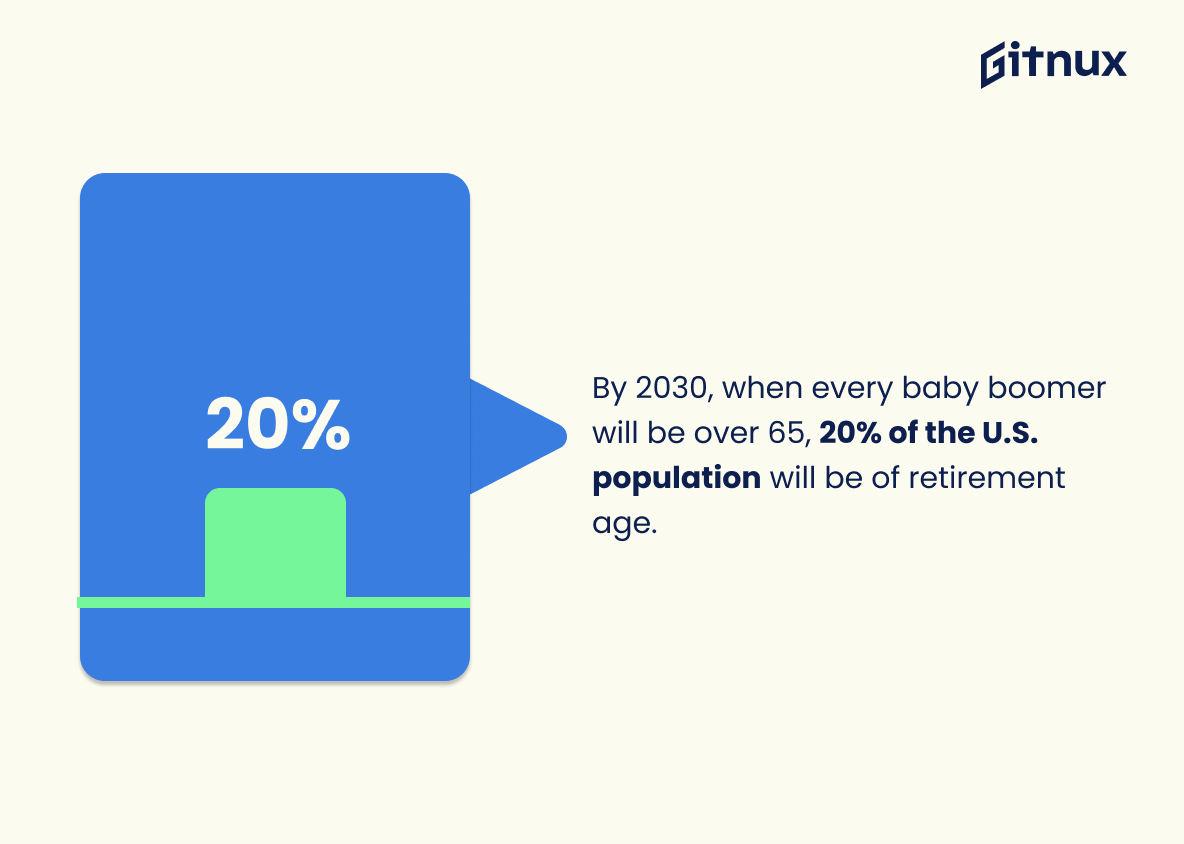

By 2030, when every baby boomer will be over 65, 20% of the U.S. population will be of retirement age.

This captivating statistic paints a vivid picture of the looming demographic shift awaiting us in the near future. As the sun sets on the baby boomer generation’s work era and every individual crosses the 65-year threshold by 2030, we will witness a dramatic swell in the country’s retirement age population. An upsurge to the tune of 20% of the American inhabitants retiring entails profound societal, economic, and healthcare ramifications.

This burgeoning share of retirees may instigate unique challenges and opportunities that demand our prudence today. A thorough understanding of such statistical projections can steer our preparation and strategic planning, ensuring this wave of baby boomer retirements does not catch us unawares.

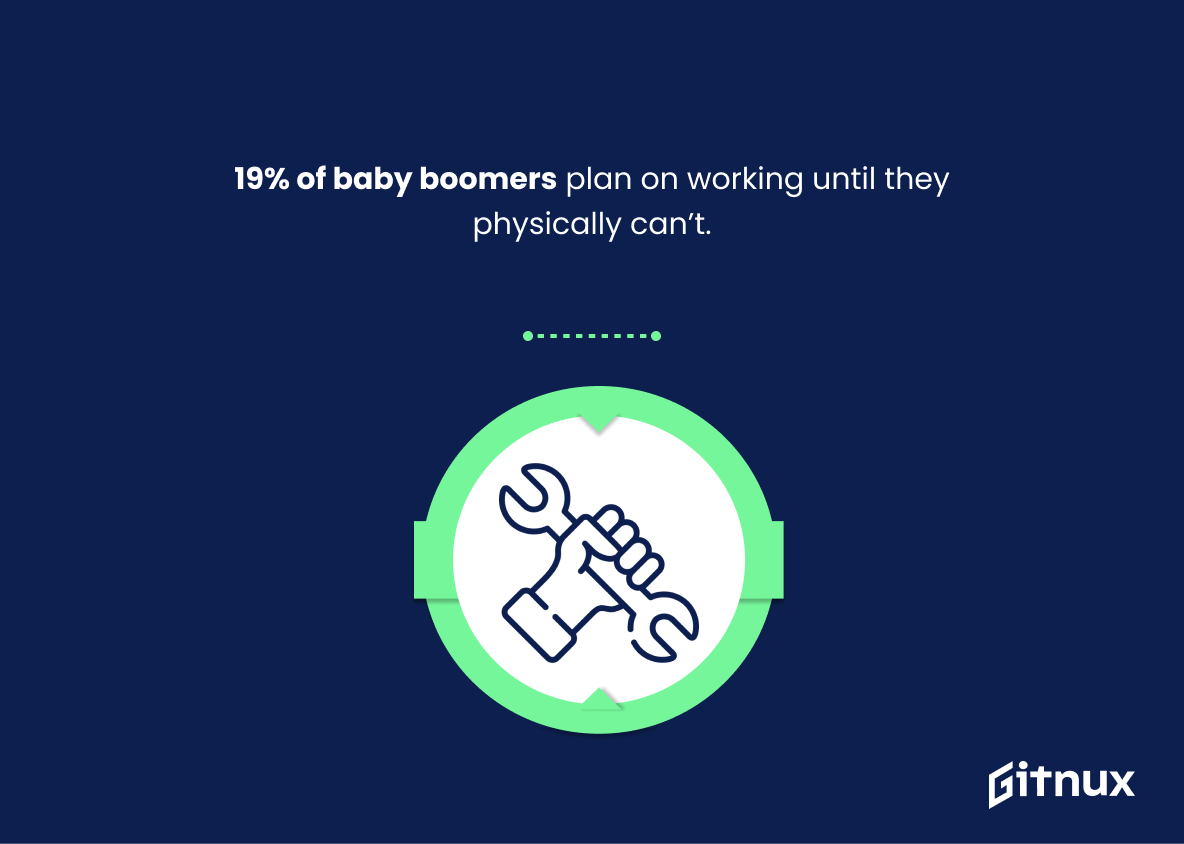

19% of baby boomers plan on working until they physically can’t.

This intriguing statistic sheds light on a profound paradigm shift that’s enveloping the Baby Boomer era. It underscores the extent to which 19% of this generation intend to remain in the workforce indefinitely. This challenges conventional retirement norms, providing a fresh perspective on the social and economic impacts of this generation’s work-life decisions.

In the wider context, it explores a unique narrative about the Baby Boomers’ retirement plans, enriching our understanding of their resilience, work ethics and the potential impacts on the provision of social services and labor market dynamics.

Around 10,000 baby boomers retire every day in the United States.

Delving into the headline statistic that approximately 10,000 baby boomers shift into the sphere of retirement each day in the United States offers us significant insights. First, this cyclical flow profoundly influences the socio-economic dynamics of the nation. Here’s an intriguing perspective: Think of this wave akin to a daily mini-city, rich in experience and wisdom, stepping off the labor market’s hustle onto the retirement field.

With an almost tectonic demographic shift, the ripple effects are numerous and impactful. This shift significantly influences sectors like healthcare, real estate, and the economy in ways that are both expansive and radical. The dramatic increase in retirees translates to increased strain on social security and healthcare systems. In terms of the labor market, an exodus of seasoned employees could potentially open more slots for the younger generations, effectively reshaping the workforce composition and industry expertise levels.

Imagine this insightful statistic as a pulsating heart, its beats sending out implications that resonating across the labor market, healthcare, economy, and generational transitions. It underscores the need for innovative solutions and planning at all levels, from individuals building right-sized nest eggs, to businesses and policymakers crafting strategies for an evolving demographic landscape.

About 38% of baby boomers have a defined benefit retirement plan.

Delving into the heart of baby boomer retirement statistics, the spotlight shines brightly on the illustrative fact that roughly 38% of this generation enjoys the security of a defined benefit retirement plan. This piece of data holds great significance as it underscores the financial preparedness of nearly two-fifths of baby boomers, providing them with a shield of security in their non-working years.

Further, it peppers in a touch of comparison, showing where this generation stands in contrast to others in terms of retirement resources. This quantifiable assurance of post-retirement stability paves the path for a deeper understanding of baby boomer economic trends in their twilight years.

26% of baby boomers are still paying off a primary mortgage.

Shining a spotlight on the striking fact that over a quarter of baby boomers still shoulder the burden of a primary mortgage payments, we weave an important thread into the complex tapestry of baby boomer retirement trends. This intriguing statistic infuses a dose of reality into the dreamy narrative of leisure-filled retirement, fundamentally altering our understanding of the financial stability of this demographic.

In the grand scheme of retirement planning, it underscores the persistent struggles many boomers face, challenging conventional wisdom, and provoking thought about the wider societal and economic implications of such a trend. This unexpected detail elevates our comprehension of the financial panorama spanning boomers’ retirements, encouraging further inquiry, and prompting discussions on better strategies.

Nearly one-third of baby boomers had made a hardship withdrawal from their retirement plan as of 2019.

The given statistic casts a spotlight on an alarming trend pervading the Baby Boomer generation’s retirement planning strategy; the not-so-insignificant strain of hardship withdrawals. According to these figures from 2019, almost a third of Boomers found themselves tapping into retirement savings prematurely, a maneuver often earmarked as a financial measure of last resort. In a discourse on Baby Boomer Retirement Statistics, this facet can’t be shunted aside, as it underscores the precarious financial situations many Baby Boomers may find themselves confronting during their golden years.

Furthermore, this statistic imparts a cautionary tale for younger generations about retirement preparation. It potentially triggers conversations about the efficacy of present pension plans, social security benefits, threat of emergencies and unexpected expenses, as well as the escalating costs of healthcare and living that people may encounter as they age. Thus, this revelation subtly invites readers to ponder over future-proofing retirement strategies, and that is unquestionably a part of its wider significance.

On average, baby boomers believe they’ll need $658,000 in their retirement savings, but the median amount saved is $200,000.

The stunning contrast between the desired retirement savings of $658,000 by baby boomers and their median savings of only $200,000 paints a vivid picture around a critical concern looming in the Baby Boomer Retiring Statistics. This discrepancy serves as an alarming wake-up call, thrusting into the spotlight some harsh realities facing baby boomers as they approach, or have entered, their retirement years.

It’s as if we’re witnessing a ticking time bomb, signaling the existence of an upcoming retirement crisis where the aspirations and preparedness for retirement are drastically mismatched. This stark numeric disparity adds considerably to the weight and urgency of the discussions around baby boomers’ retirement readiness, ensuring the readers grasp the magnitude of the issue and heightening the relevance of the blog post.

Over 50% of baby boomers plan to work past age 65 or do not plan to retire.

Peering into this insightful statistic, it’s evident that over half of the baby boomer population are scripting a new narrative for their retirement, by either prolonging their working years beyond 65 or ruling out retirement altogether. This unorthodox trend significantly redefines traditional retirement concepts and sheds light on several compelling facets, including social, economic, and health perspectives.

A blog focused on ‘Baby Boomer Retiring Statistics’ would profit from this data by delivering a fresh outlook on the evolving retirement norms. It helps broaden the discourse on baby boomers’ goals, aspirations, financial readiness, and the impact of their choices on the society and economy. Therefore, this statistic is a pivotal cornerstone to establishing a broader, forward-thinking conversation around retirement.

Baby boomers estimate that their health care costs in retirement will come to about $5,500 a year per person, but the reality is closer to $14,000.

Highlighting the statistic, “Baby boomers estimate their health care costs in retirement to be around $5,500 a year per person, but the reality is closer to $14,000”, punctuates the urgent need for reevaluation of financial planning among boomers. In a blog post about Baby Boomer Retiring Statistics, this figure serves as a stark wake-up call for boomers on the cusp of retirement.

It reveals a potentially hazardous discrepancy between expectations and the financial realities they may face in retirement, particularly with respect to health care expenses. In essence, this figure underscores the risk of underestimating retirement costs, ignites the conversation around more strategic financial planning, and encourages baby boomers to equip themselves with a more accurate estimate of health-related expenses in their twilight years.

47% of baby boomers who are still working have reported job loss or reduced hours due to the Covid-19 pandemic, which could impact their retirement.

Peering through this provocative stat – 47% of toiling baby boomers disclosed job loss or cut-back on working hours amid the Covid-19 pandemic, one can infer its potential to cast a ripple, even a tempest, on their imminent retirement prospects. In the theatre of a blog post on Baby Boomer Retirement Statistics, it manifests as a gripping scene-stealer, underscoring the generational shockwaves of the pandemic’s economic fallout.

A closer reading of this statistic brings to life not only the pandemic-induced insecurities these mature workers are wrestling with but also hints at the consequent changes to their retirement paradigm, thereby enriching and adding a sense of urgency to the overall narrative.

Conclusion

In essence, the retirement situation for Baby Boomers is undoubtedly evolving. We’ve learned through the data and statistics that Baby Boomers are not only redefining retirement but are also facing unique challenges such as healthcare costs, managing retirement savings, and overcoming retirement anxieties. Undoubtedly, these retiring Baby Boomers are changing the face of older living and challenging societal norms by striving for more active, fulfilled post-career lives.

Fresh strategies, solutions and approaches are important to adequately accommodate this large demographic and their distinct needs. As the landscape of retirement continues to evolve, it’s crucial that we keep an eye on these trends in order to better plan for the future and make informed decisions.

References

0. – https://www.www.fidelity.com

1. – https://www.www.urban.org

2. – https://www.financebuzz.com

3. – https://www.www.cnbc.com

4. – https://www.www.pewresearch.org

5. – https://www.www.fool.com

6. – https://www.www.bankrate.com

7. – https://www.www.businesswire.com

8. – https://www.www.businessinsider.com

9. – https://www.www.transamericacenter.org