Navigating the complex financial world of mortgages can be daunting for seniors who desire to age gracefully within the comfort of their homes. Enter the reverse mortgage – a unique financial vehicle designed to ease this burden. This often misunderstood tool provides homeowners aged 62 and above an opportunity to convert a portion of their home equity into cash, whilst retaining their homeownership status. However, as this industry continues to evolve, understanding the current trends and statistics becomes necessity. In this blog post, we’ll dive into the multifaceted realm of reverse mortgages, unraveling the key industry statistics to help you comprehend the massive impact and future potential of reverse mortgages. Whether you are considering to procure a reverse mortgage, a finance student, a research enthusiast, or a financial planner, the insights and data statistics offered in this piece will shed light on the intricacies governing the reverse mortgage sector.

The Latest Reverse Mortgage Industry Statistics Unveiled

There were about 423,000 messages sent in 2020 targeting reverse mortgage leads, which is a 445% increase from the year prior.

The meteoric rise in messages targeting reverse mortgage leads in 2020, boasting a whopping 445% increase from the previous year, paints a vivid picture of a dynamic and rapidly evolving reverse mortgage industry. This statistic firmly places the spotlight on an escalating trend of pro-activity in the sector. Clearly indicating an aggressive and renewed interest in this specific market, it echoes an industry’s strategic pivot towards capitalizing on reverse mortgage potential. It’s an unmistakable shift that hints at a surging demand and potentially promising profits on the horizon. This illuminating data point, therefore, is invaluable in gleaning insights into the contemporary trends and upcoming trajectory of the reverse mortgage industry, making it a vital pulse-check in this analytical exercise.

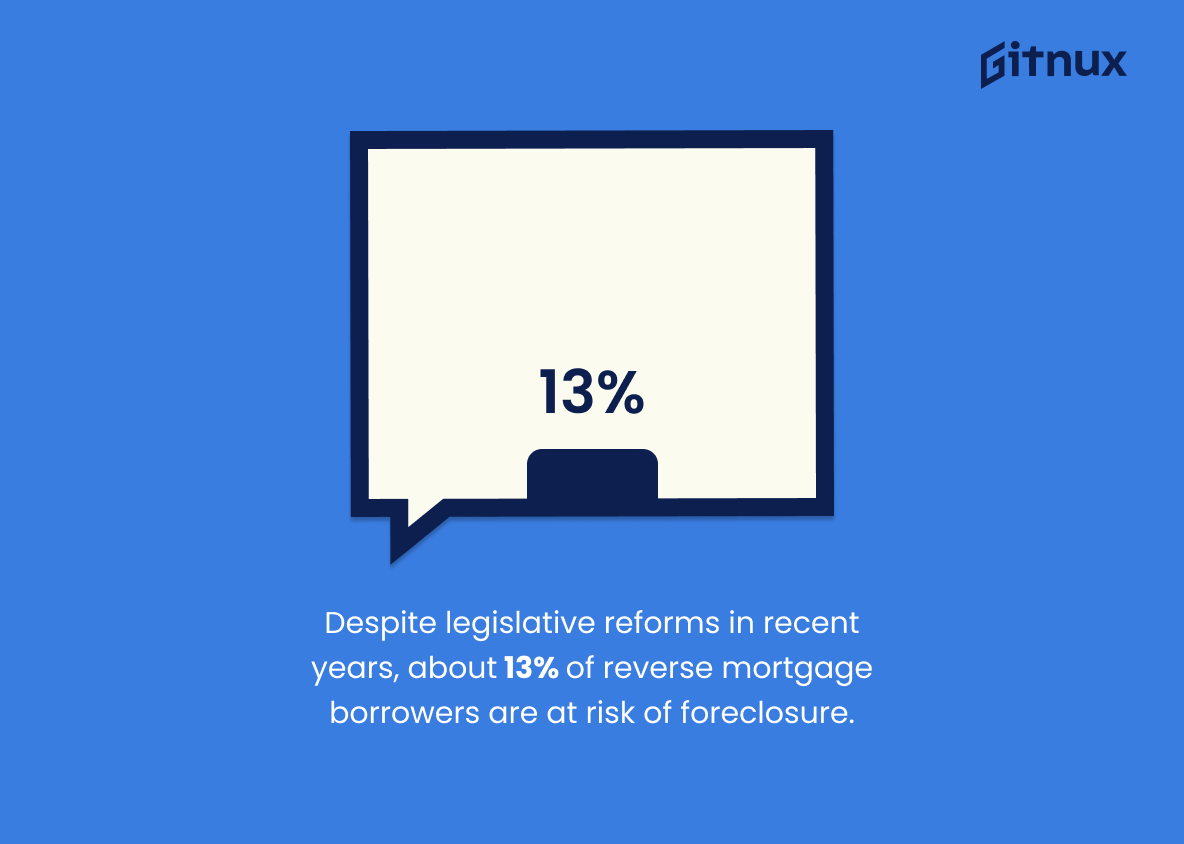

Despite legislative reforms in recent years, about 13% of reverse mortgage borrowers are at risk of foreclosure due to unpaid taxes and insurance.

Delving into the dynamics of the reverse mortgage industry, one cannot ignore the startling revelation that, despite substantial legislative developments, approximately 13% of reverse mortgage borrowers tread on the brink of foreclosure due to unpaid taxes and insurance. This metric casts a harsh light upon the paradoxical reality of secure retirement funding versus potentially losing one’s home. It layers the conversation around reverse mortgages with a note of caution, subtle but insistent, directing our attention to the potential hazards that lay concealed amidst the touted benefits of these financial products. This statistic, therefore, becomes an indispensable anchor in our explorative journey through the maze of reverse mortgage industry statistics, molding perceptions and setting the stage for a complex but comprehensive understanding of the industry.

The total volume of reverse mortgages fell by 31.6% for the fiscal year 2019 compared to the previous year.

Diving headfirst into the intricate universe of Reverse Mortgage Industry Statistics, one can’t ignore the startling descent of 31.6% in the total volume of reverse mortgages for the fiscal year 2019. This significant drop tells an intriguing tale of the fluctuations within the industry, painting a nuanced picture of shifting trends and fortunes. It’s akin to the heartbeat of the reverse mortgage market, whose pulse seemed to have slowed dramatically during this period. From a bird’s eye view, this decremental trend may represent a challenge or an opportunity – a possible red flag signaling caution to reverse mortgage providers, or a call-to-arms for industry strategists seeking to reinvigorate the market. Thus, this notable statistic serves as a compass guiding our understanding and interpretation of the industry’s health and trajectory.

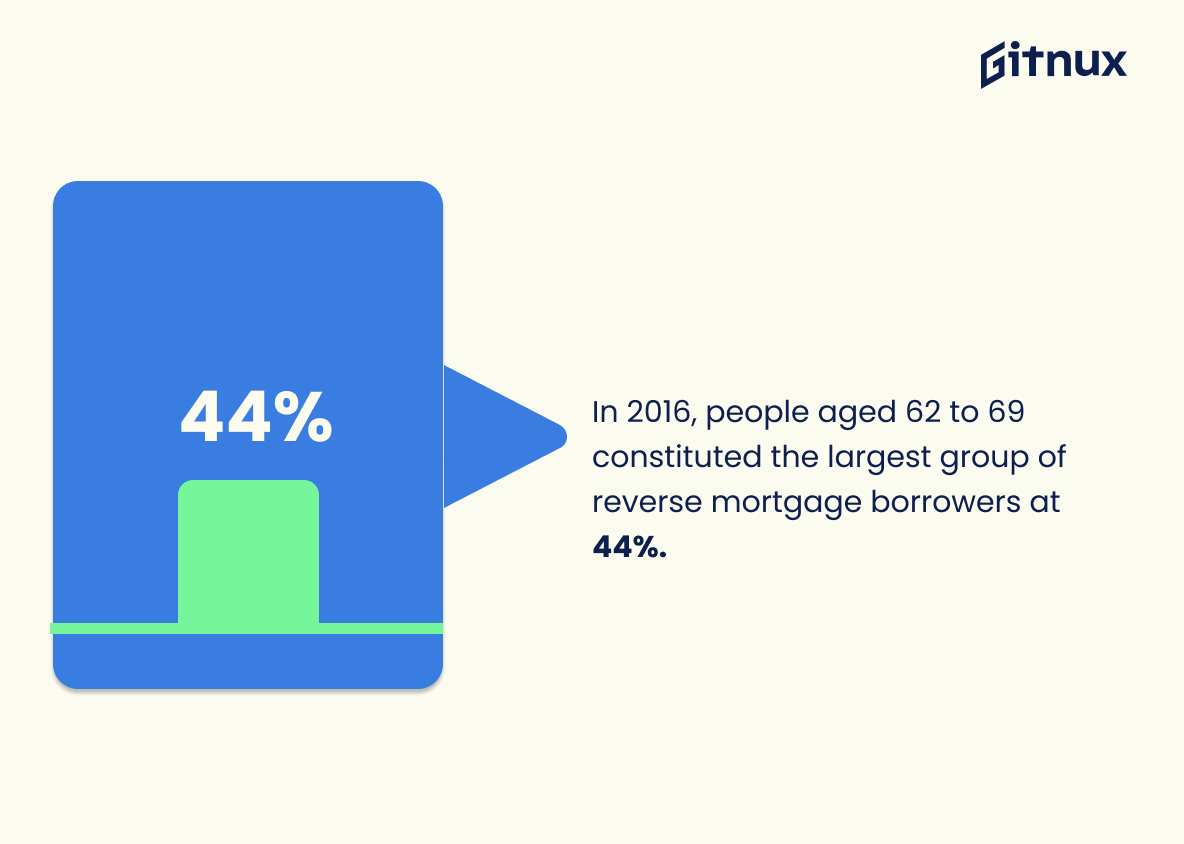

In 2016, people aged 62 to 69 constituted the largest group of reverse mortgage borrowers at 44%.

Examining the numbers, a clear trend emerges from 2016 figures, illustrating that those between 62 to 69 were the dominant demographic opening up their doors to reverse mortgages, capturing 44% of the borrower market. What does this highlight? The aging population is actively utilizing this avenue as a financial strategy. Evidently, this age band – in their retirement years, yet still agile and active – see reverse mortgages as a viable option to sufficiently finance their later life needs. This dominant demographic presents significant implications for the direction of the reverse mortgage industry. These figures could possibly influence the industry’s future trajectory, marketing strategies, and further product innovations, tailoring them accordingly to cater to this influential age group.

As of 2017, Florida ranked first in the US with over 7000 reverse mortgages.

Florida’s dominating prevalence of over 7000 reverse mortgages back in 2017 allows us to glean critical insight into the reverse mortgage industry. It illuminates the high demand for this financial instrument in areas with a significant older population. This nugget of information acts as a precedent, helping industry experts predict future market trends, understand regional preferences, inform services, and strategize their marketing efforts. Consequently, it contributes significantly to shaping the narrative of reverse mortgage industry statistics.

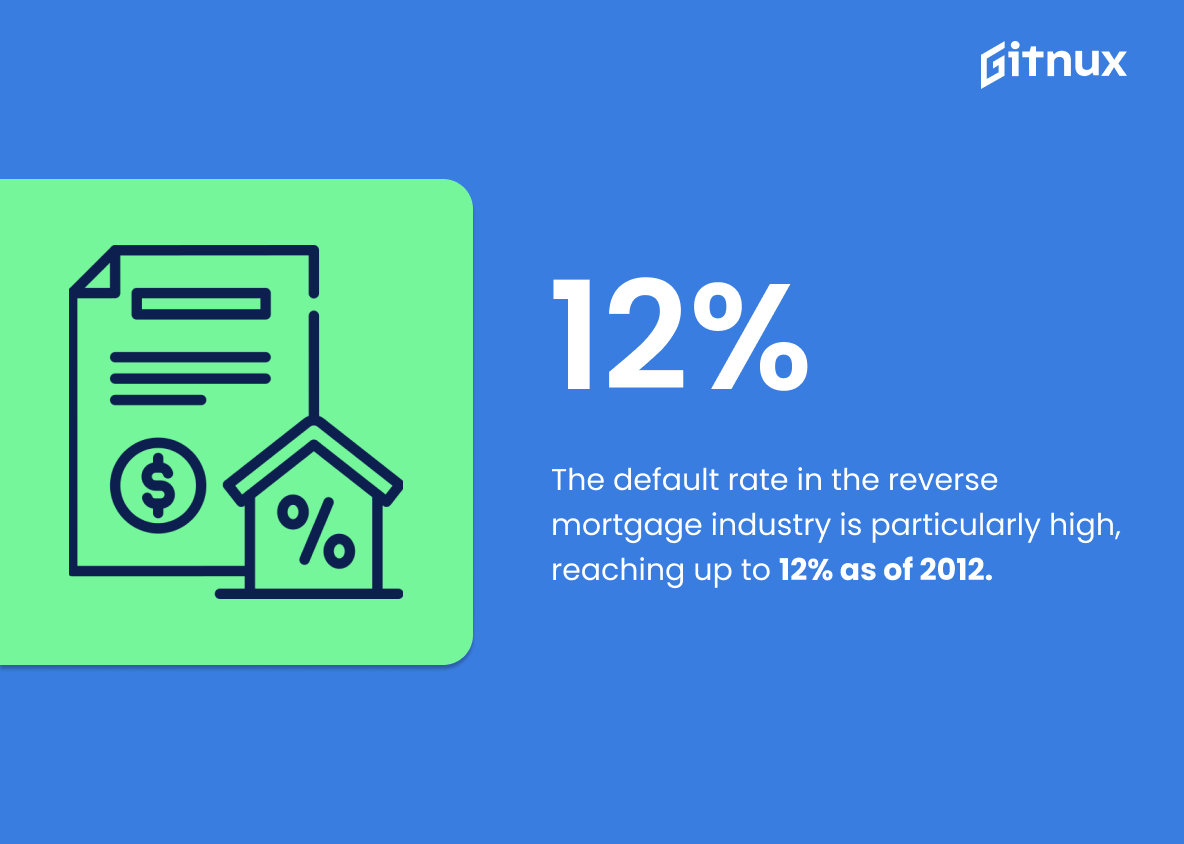

The default rate in the reverse mortgage industry is particularly high, reaching up to 12% as of 2012.

Highlighting the statistic of a default rate reaching as high as 12% in the reverse mortgage industry in 2012 casts an intricate light on the risks inherent in this sector. It’s akin to a wake-up call for potential clients, investors and analysts, driving them to dig deeper into the causes and consequences of such a scenario.

In tandem with other statistical data, it offers a thorough understanding of the market dynamics within the reverse mortgage landscape. This can aid potential borrowers to comprehend the gravity of their commitments and perhaps encourage them to meticulously strategize their financial decisions.

Furthermore, the data reverberates its implications to policymakers and industry leaders, prompting them to review and reinforce their strategies in mitigating default risks. The statistic serves as an important cornerstone of a blog post on Reverse Mortgage Industry Statistics, providing context, stirring conversation, and triggering critical thought around the industry’s challenges.

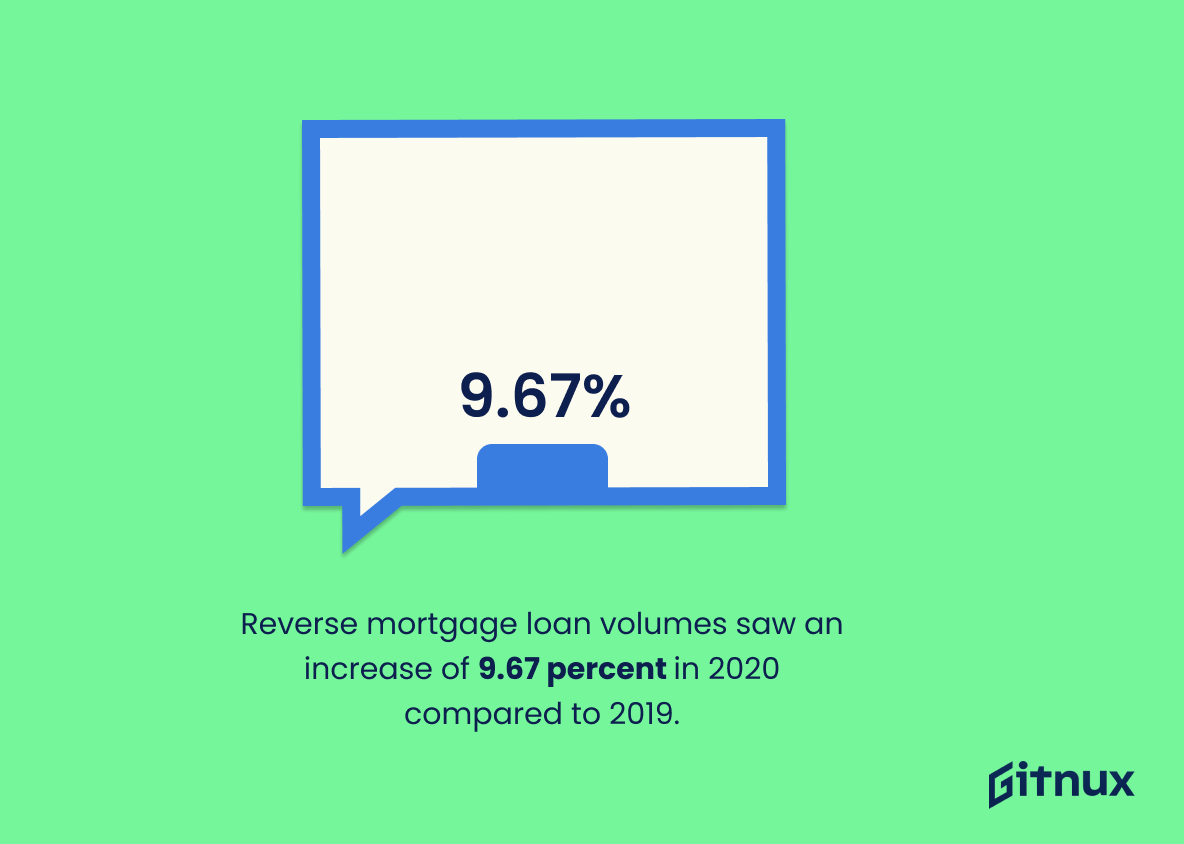

Reverse mortgage loan volumes saw an increase of 9.67 percent in 2020 compared to 2019.

The rise of 9.67 percent in reverse mortgage loan volumes between 2019 and 2020 serves as a potent pulse-check for the state of the reverse mortgage industry. More than merely numbers, this uptick points towards the escalating acceptance and reliance on reverse mortgages as a financial tool among the senior population. It offers a window into the evolving market dynamics, hinting at an insatiable demand for such loans in the face of an aging population. Further, it acts as a testament to the industry’s resilience and its capacity to thrive in unpredictable economic landscapes, showing its relevance and unarguably immense potential for growth.

The industry has remained on a consistent upward trajectory since 2020, with a total increase of 17% year-over-year.

Reflecting on this compelling statistical shift, it’s evident that the Reverse Mortgage Industry is not just repeating history, but rewriting it since 2020. With a consistent upward trajectory and an impressive overall growth of 17% year-over-year, this enhancement validates the increasing trust and dependency on reverse mortgages by older homeowners. This dynamic shift underlines the growing importance of reverse mortgages as a viable financial strategy in people’s lives, particularly those seeking a steady income stream during their golden years.

As of 2017, HUD revealed that more than 18% of reverse mortgage loans taken out from 2009 to June 2016 are expected to go into default because of unpaid taxes and insurance.

Unveiling a stark piece of information, HUD’s report in 2017 shares a sobering insight for the Reverse Mortgage Industry, indicating a potential red flag. The report estimates that over 18% of reverse mortgage loans, originated between 2009 to June 2016, lie on the precipice of default, owed to unpaid taxes and insurance.

Undeniably, this percentage is a significant marker for the industry, influencing the landscape of default risk assessments. It sends a strong warning signal to both the lenders and borrowers about the looming fiscal responsibility associated with these loans.

From a lender’s perspective, this might trigger a need to devise robust underwriting guidelines and loss mitigation strategies. Equally, for prospective borrowers, it emphasizes the criticality of having enough financial capacity to manage loan obligations, including taxes and insurance.

Hence, this statistic strikes as both a cautionary tale, and a call for action in the Reverse Mortgage Industry. Its implications range from shaping regulatory frameworks to influencing consumer education strategies, thereby making it an indispensable part of discussing Reverse Mortgage Industry Statistics.

In January 2020, total Home Equity Conversion Mortgage (HECM) endorsements were up 158.2% to 4,300 loans.

In the complex tapestry of Reverse Mortgage Industry statistics, the surge of HECM endorsements by 158.2% to 4,300 loans in January 2020 serves as an intriguing highlight. This number provides a lens to gauge the buoyant interest and uptake of such mortgages, pointing towards a spectacular shift in sentiment and behavior among homeowners. This significant uptake acts as a barometer of the industry’s health, signaling to stakeholders, such as lenders and investors, the vibrancy and potential growth within this segment. In essence, such a statistic stands as a lighthouse amidst the sea of data, guiding our understanding of this industry’s dynamics.

Around 49,000 seniors took out reverse mortgages in 2018.

Shedding light on this significant figure; approximately 49,000 seniors initiated reverse mortgages in 2018. This substantial number not only underscores the growing popularity of this financial option among mature adults, it also signals the vibrancy and relative influence of the reverse mortgage industry within the broader housing market. Embedded within this raw data, there is a compelling narrative, one that speaks to the evolving financial strategies of seniors and the pivotal role that reverse mortgages can play in shaping their economic futures. In short, this statistic forms an essential piece of the broader narrative that reveals the reverse mortgage industry’s narrative, impact, and growth trajectory.

As of April 2021, there was an 86.1% increase in reverse mortgage loan applications compared to the same period in 2020.

Immersing ourselves in the heart of the Reverse Mortgage Industry, we dive deep into revealing numbers that speak volumes. Our attention is drawn towards the power-packed statistic – a dramatic 86.1% increase in reverse mortgage loan applications as of April 2021 as compared to the same period in 2020. It’s like a beacon, shedding light on the rapidly evolving trends and consumer behavior in this niche.

This decisive shift punctuates several critical insights into the industry. Firstly, it suggests a growing consumer confidence and acceptance of reverse mortgage loans as a viable financial tool. This spike could be driven by the year-long economic uncertainty precipitated by the global pandemic which has nudged many homeowners, particularly seniors, to explore tapping into their home equity for increased financial security.

This uptick further underscores increasing market opportunities for lenders and the need for industry players to step up and accommodate this surge. Additionally, government bodies and regulators would be pressed to ensure consumer protection in this escalating market.

Thus, this all-important statistic unfurls a ripple effect throughout the industry and beyond, indicating not only where we are today but potentially illuminating the path ahead. The knowledge of this surge equips all stakeholders including borrowers, lenders, and regulators with the vital grasp of the direction in which the industry ship is sailing.

42% of reverse mortgage loans were used to pay off a traditional mortgage in 2016.

Painting a compelling portrait of the state of the reverse mortgage industry in 2016, this statistic shows that nearly half of all reverse mortgage loans were being earmarked to combat existing traditional mortgage debt. This important trend underscores the potential impact of the industry’s services in providing an effective, alternative solution for homeowners to juggle mortgage obligations. Also, this surprising revelation further illustrates how vital reverse mortgages can be in providing financial flexibility and stability to a growing number of customers struggling with traditional mortgage debt.

Overall, the demand for reverse mortgages is expected to rise due to an increase in home equity amongst seniors, reaching $9.2 trillion in 2021.

Nestled within the heart of this poignant statistic lies the pulse of the reverse mortgage industry. As a beacon, it illuminates the profound and undeniable impact of the growing home equity amongst seniors, which is estimated to reach a colossal $9.2 trillion in 2021. This promising development not only maps the future trajectory of the industry, illustrating a surge in the demand for reverse mortgages, but also uncovers a treasury of opportunities ripe for exploration. Ultimately, this statistic serves as a compelling narrative in itself, underscoring the progressive evolution of the reverse mortgage industry while painting a prosperous panorama for its future.

In 2018, 73% of reverse mortgagers were homeowners.

When crafting a narrative on Reverse Mortgage Industry Statistics, the stunning revelation that 73% of reverse mortgagers in 2018 were homeowners offers a significant insight into the industry’s landscape. This vibrant statistic illuminates the noteworthy interplay between homeownership and the reverse mortgage market. It underscores the fact that the vast majority of people engaging in reverse mortgages are individuals who own homes, highlighting homeowners as a principal demographic in this market. This paints an anecdotal picture of who’s truly involved in reverse mortgages, helping to better understand market segmentation, trends, customer needs, and the home equity conversion mindset.

59% of reverse mortgage borrowers in 2020 were over 70 years of age.

Highlighting the data point that a substantial 59% of 2020’s reverse mortgage borrowers were above 70 years of age provides an illuminating lens on the demographics driving the Reverse Mortgage Industry. It underscores a strong correlation between the age bracket of 70 and above and propensity to seek reverse mortgage solutions, indicating that this industry is relying significantly on senior citizens for its growth. Understanding this core client group delves us deeper into their specific needs and challenges, invaluable for fine-tuning service offerings and shaping future industry strategies. This ballpark figure further paves the way for trend analysis, facilitating predictions and enabling proactive adaptation to market shifts.

Reverse mortgages were 11.7% of all mortgages in the U.S. in 2019.

The figure, ‘Reverse mortgages accounting for 11.7% of all U.S. mortgages in 2019,’ serves as a powerful indicator of the evolving direction the mortgage industry is taking. It underscores the growing prominence of reverse mortgages as a crucial player in the financial sector. This shift paints a vibrant picture about US homeowners, especially seniors, who increasingly leverage their home equity for various financial needs. Hence, this data point holds center stage in the narrative of the reverse mortgage industry, providing valuable insights into the industry’s current landscape, its trajectory, and potential future course.

According to the CFPB, nearly 70% of complaints about reverse mortgages are related to borrowers’ inability to make changes to them once they are agreed upon.

Shedding light on the plight of borrowers, a shocking insight from the Consumer Financial Protection Bureau (CFPB) underscores a significant issue marring the reverse mortgage industry. It reveals that nearly 70% of complaints arise due to rigid terms hindering borrowers from modifying their reverse mortgages post-agreement. Delving into the crux of the problem, this striking figure is not merely a statistic. It spotlights the critical need for industry reforms and points towards the necessity for a more flexible and empathetic approach towards borrowers.

Such an alarming statistic also doubles as a cautionary advice for potential borrowers who must carefully examine the conditions of their reverse mortgage agreements. It paints a somewhat grim picture of the absence of flexibility within the industry—a strong deterrent for potential clients considering reverse mortgages. Indeed, this statistic intricately weaves together a narrative of the current issues at hand and the imminent need for transformation within the reverse mortgage industry.

Of the 1,300,000 reverse mortgages taken out between 1989 and 2018, approximately 18% ended up in foreclosure.

Dissecting the fabric of the Reverse Mortgage Industry, the statistic that around 18% of the 1.3 million reverse mortgages from 1989 to 2018 ended in foreclosure serves as a crucial beacon light for understanding the industry’s landscape. It not only exposes the level of risk involved, but also underlines the significant proportion of homeowners unable to fulfill their obligations, leading to foreclosure. Such a figure infuses our understanding with a realistic viewpoint of the industry’s undercurrents, reshaping both consumer expectations and the industry’s mitigation strategies. Equally significant is its potential to stimulate policy modifications aimed at reducing foreclosure rates, thereby improving the industry’s health and reliability for future borrowers.

Conclusion

In closing, the Reverse Mortgage Industry Statistics reveal a dynamic and evolving marketplace. This financial service provides seniors with the opportunity to leverage their home equity for additional income during retirement years, leading to an increase in demand. Whether you are a homeowner, financial advisor, or industry professional, understanding these statistics is crucial. They not only illustrate the current state of the industry but also provide useful insights into future trends. As demographics shift and more people become eligible, it’s clear that the reverse mortgage industry is poised for significant growth. Staying updated on these statistics can empower individuals to make informed decisions and maximize the benefits of this unique financial tool.

References

0. – https://www.www.aarp.org

1. – https://www.www.forbes.com

2. – https://www.www.nationalmortgagenews.com

3. – https://www.www.nbcnews.com

4. – https://www.www.consumerfinance.gov

5. – https://www.www.businesswire.com

6. – https://www.www.mortgageloan.com

7. – https://www.www.martindale.com

8. – https://www.www.cnbc.com

9. – https://www.reversemortgagedaily.com

10. – https://www.www.usatoday.com

11. – https://www.www.reporter.am

12. – https://www.rminsight.net

13. – https://www.www.chicagotribune.com