Mortgage debt in the United States has been steadily increasing over the years, reaching a total of $10.9 trillion in the first quarter of 2021. As of April 2021, the average interest rate for a 30-year fixed-rate mortgage was 3.06%, and 63.3% of all mortgage applications were for purchase loans that same year. The median down payment for first-time homebuyers was 6%, while the average loan size reached $286,176 in 2020 – an increase from 2019’s figure at $280,826.

In addition to this data on mortgages taken out by individuals or households, other statistics include 4.44% being currently enrolled in forbearance programs as well as homeownership rates standing at 65%. Furthermore 31% have no mortgage debt whatsoever and 33% refinanced their mortgages last year alone; with VA loans accounting for 10.8%. Subprime mortgages also saw an increase to 1 .18 trillion dollars whilst existing homes sold totaled 5 million three hundred thousand units during 2020 – resulting in a delinquency rate set at 6 .66 % (1 .4 million seriously delinquent). Refinancing activity hit 2 .2 trillion dollars with cash outs making up 65 percent ,while down payments averaged 46 thousand eight hundred US Dollars across America’s lenders last year too..

This statistic is a telling indication of the immense financial burden that many Americans are facing. It highlights the fact that mortgage debt is a major issue in the US, and that it is continuing to grow. This is an important point to consider when discussing mortgage statistics, as it provides a clear picture of the current state of the housing market.

As of April 2021, the average interest rate for a 30-year fixed-rate mortgage in the United States was 3.06%.

This statistic is a crucial indicator of the current state of the mortgage market in the United States. It provides insight into the average cost of borrowing money for a 30-year fixed-rate mortgage, which is an important factor for potential homebuyers to consider when making decisions about their finances. By understanding the average interest rate for a 30-year fixed-rate mortgage, readers of the blog post can gain a better understanding of the current mortgage market and make more informed decisions about their own mortgage needs.

Morgage Statistics Overview

In 2020, approximately 63.3% of mortgage applications in the United States were for purchase loans.

This statistic is a telling indication of the current state of the mortgage market in the United States. It reveals that the majority of mortgage applications are for purchase loans, indicating that the housing market is still strong despite the economic downturn caused by the pandemic. This statistic is important for anyone interested in understanding the current state of the mortgage market and the overall health of the housing market.

In 2019, the median down payment for first-time homebuyers in the United States was 6%.

This statistic is a telling indication of the current state of the housing market in the United States. It reveals that the majority of first-time homebuyers are making relatively small down payments, which could be indicative of a lack of financial resources or a lack of confidence in the housing market. This statistic is an important piece of information for anyone looking to understand the current state of the mortgage market.

In 2020, the average mortgage loan size in the United States reached $286,176.

This statistic is a telling indication of the current state of the mortgage market in the United States. It reveals that the average loan size has increased significantly since previous years, indicating that more people are taking out larger mortgages to purchase homes. This is an important insight for anyone interested in understanding the current trends in the mortgage market and how they may affect their own decisions.

As of April 2021, approximately 4.44% of mortgages in the United States were in forbearance.

This statistic is a telling indication of the current state of the mortgage market in the United States. With nearly 4.5% of mortgages in forbearance, it is clear that the pandemic has had a significant impact on the ability of many homeowners to make their payments. This statistic is a stark reminder of the economic hardship that many Americans are facing, and it serves as a reminder of the importance of understanding the mortgage market and the potential risks associated with it.

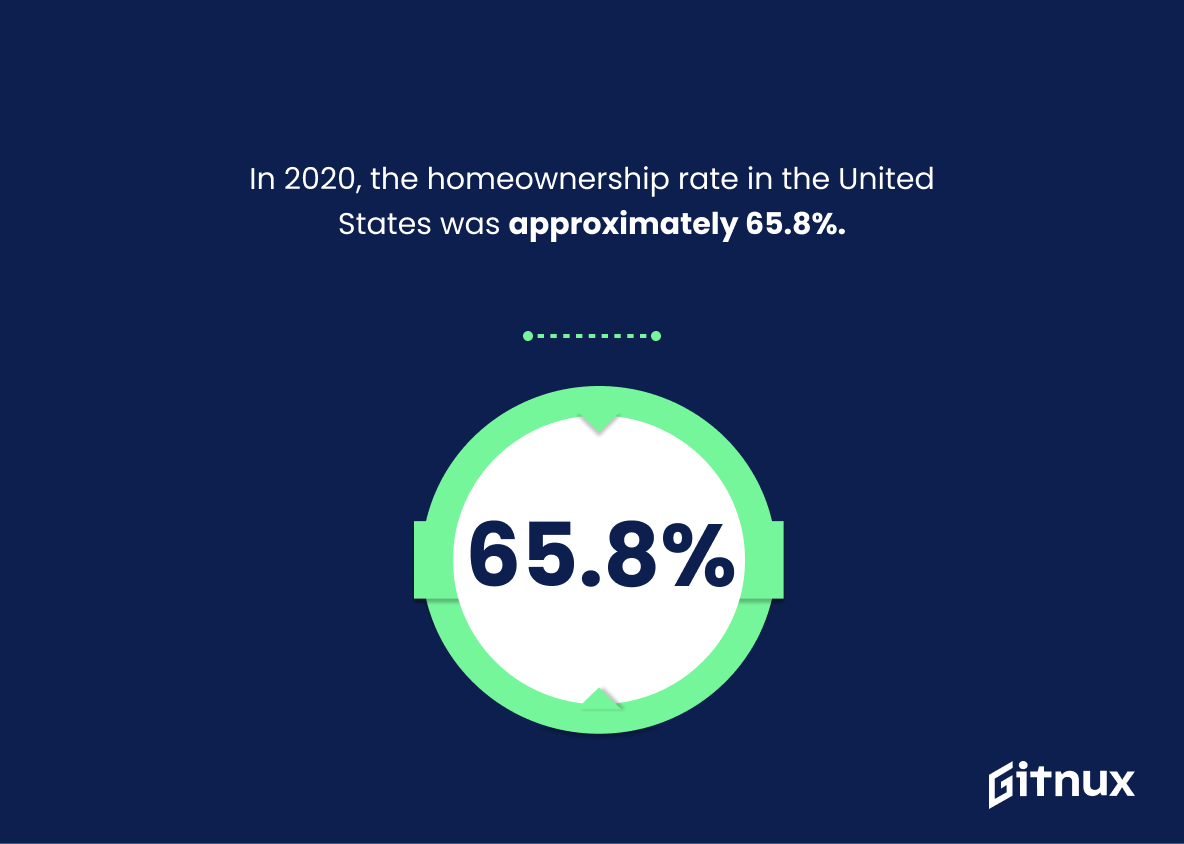

In 2020, the homeownership rate in the United States was approximately 65.8%.

The homeownership rate in the United States in 2020 is a telling statistic when it comes to mortgage statistics. It provides insight into the current state of the housing market and the ability of Americans to purchase homes. This statistic can be used to gauge the success of mortgage programs and the overall health of the housing market. It can also be used to identify areas of improvement and potential opportunities for growth. Understanding the homeownership rate is essential for anyone interested in the mortgage industry.

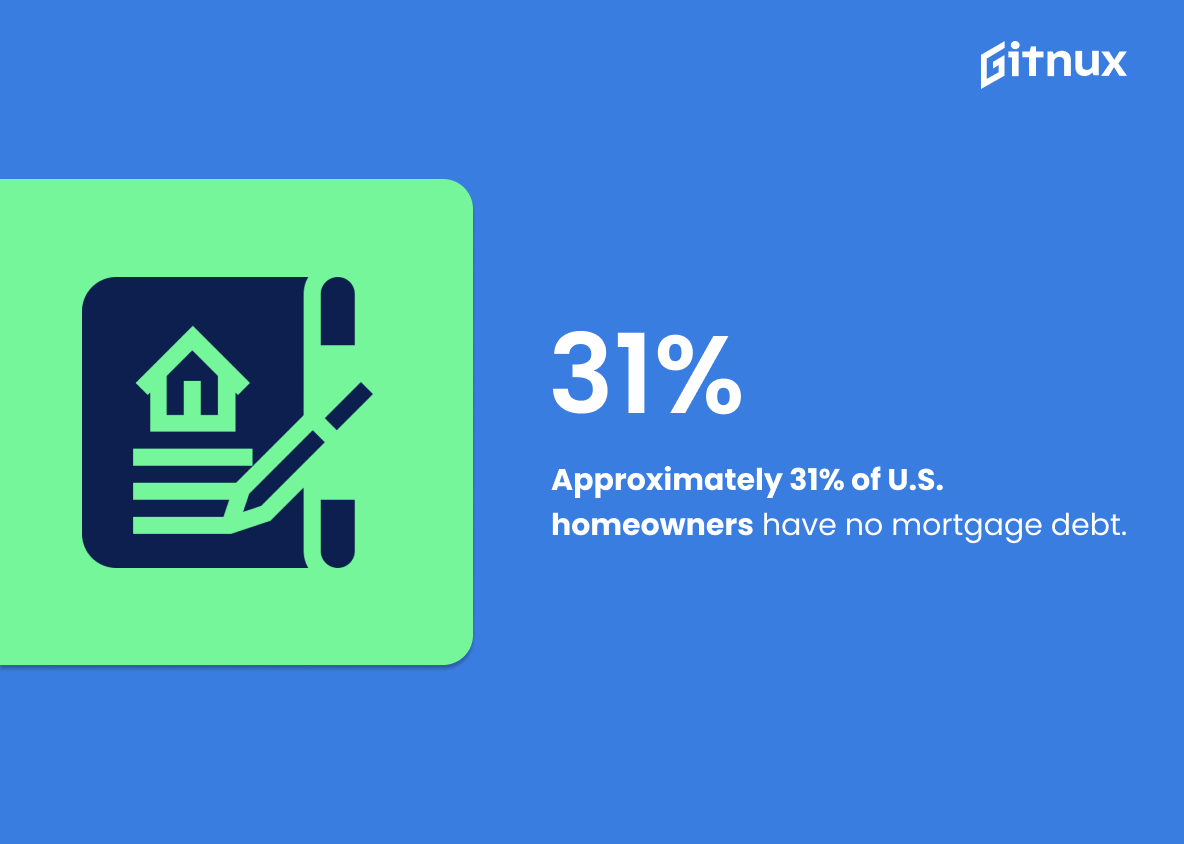

Approximately 31% of U.S. homeowners have no mortgage debt.

This statistic is significant in the context of a blog post about Mortgage Statistics because it highlights the fact that a large portion of U.S. homeowners are not burdened by mortgage debt. This indicates that many homeowners have either paid off their mortgages or have chosen to purchase their homes outright. This statistic is a testament to the financial stability of many U.S. homeowners and provides a positive outlook for the housing market.

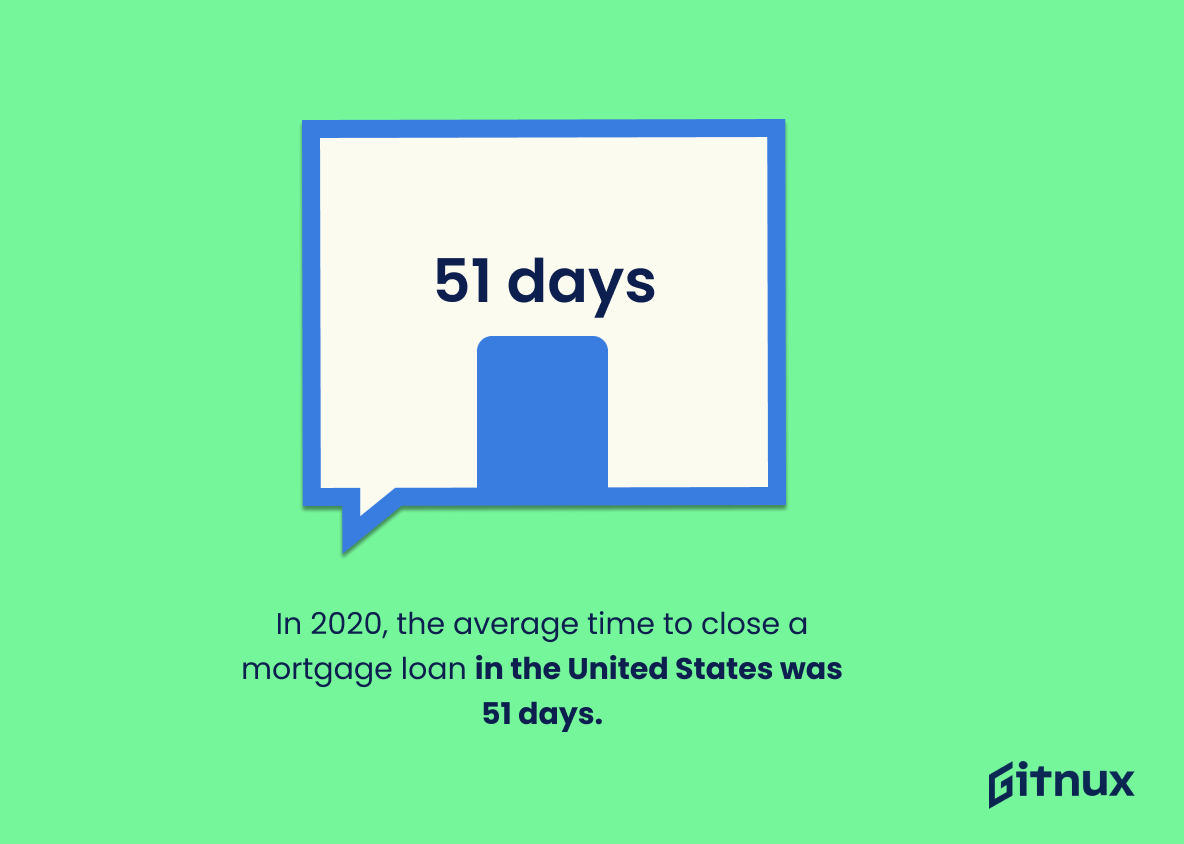

In 2020, the average time to close a mortgage loan in the United States was 51 days.

This statistic is a telling indication of the current state of the mortgage market in the United States. It reveals that the process of obtaining a mortgage loan is relatively quick and efficient, taking an average of just 51 days to close. This is important information for potential homebuyers, as it provides insight into the timeline of the mortgage process and can help them plan accordingly.

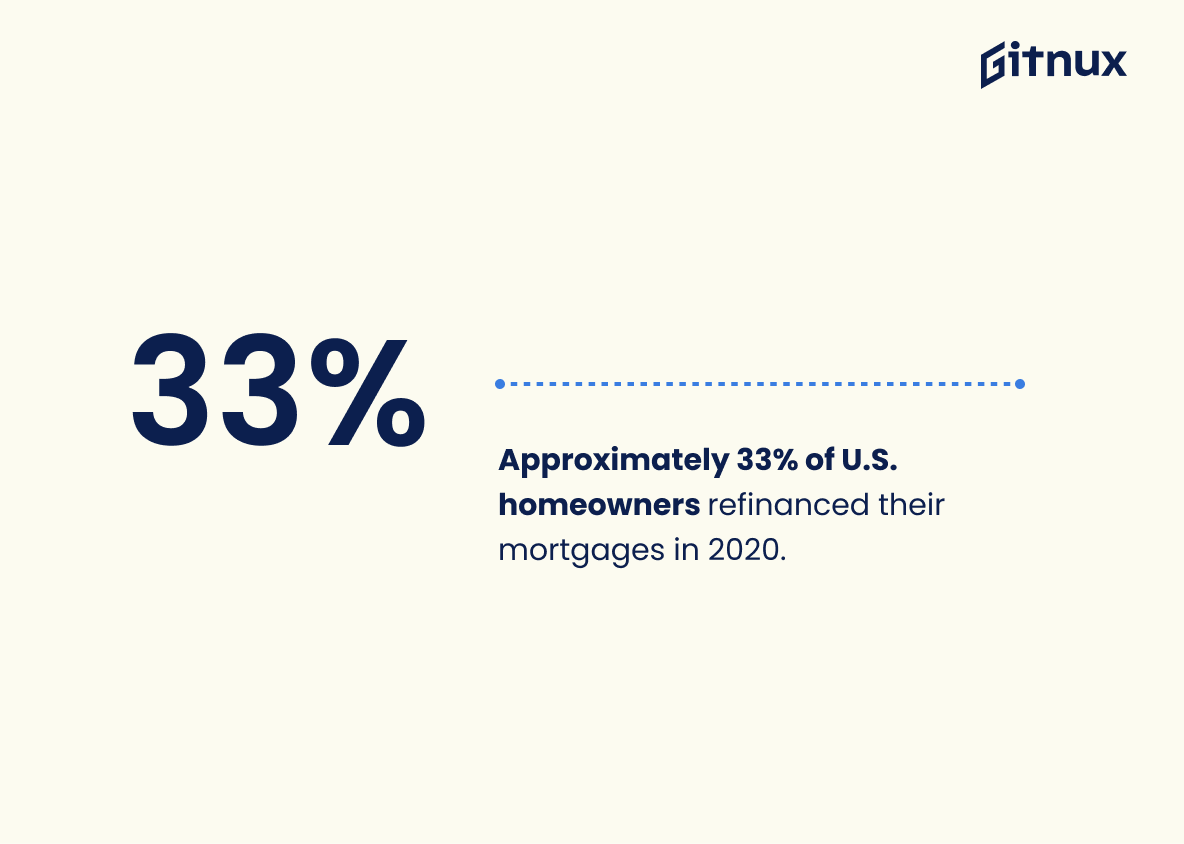

Approximately 33% of U.S. homeowners refinanced their mortgages in 2020.

This statistic is a telling indication of the state of the U.S. mortgage market in 2020. It shows that a significant portion of homeowners took advantage of the low interest rates and refinanced their mortgages, which could be a sign of financial stability and confidence in the market. This statistic is important to consider when discussing mortgage statistics, as it provides insight into the decisions of homeowners and the overall health of the mortgage market.

In 2020, the average credit score for an approved mortgage loan in the United States was 753.

This statistic is a telling indication of the current state of the mortgage market in the United States. It reveals that the average credit score for an approved mortgage loan is relatively high, indicating that lenders are being more stringent in their lending criteria. This statistic is important for anyone considering applying for a mortgage loan, as it provides insight into the level of creditworthiness that is required to be approved for a loan.

In 2020, the top three mortgage lenders in the United States were Quicken Loans (now Rocket Mortgage), Wells Fargo, and Chase.

This statistic is significant in the context of a blog post about Mortgage Statistics because it provides a snapshot of the current mortgage market in the United States. It reveals which lenders are dominating the market and which ones are the most popular among borrowers. This information can be used to inform readers about the current state of the mortgage industry and help them make informed decisions when selecting a lender.

In 2020, VA loans accounted for approximately 10.8% of all mortgage originations in the United States.

This statistic is a testament to the importance of VA loans in the mortgage industry. It shows that VA loans are a major player in the mortgage origination market, and that they are a viable option for those looking to purchase a home. This statistic is especially relevant in a blog post about mortgage statistics, as it provides a snapshot of the current state of the mortgage industry and the role VA loans play in it.

In 2020, the total value of subprime mortgage loans in the United States reached $1.18 trillion.

This statistic is a telling indication of the state of the mortgage market in the United States. It highlights the fact that subprime mortgage loans are still a major part of the market, and that the total value of these loans has grown significantly in recent years. This is an important point to consider when discussing mortgage statistics, as it shows that the market is still heavily reliant on subprime loans, and that this reliance is growing.

In 2020, approximately 5.3 million existing homes were sold in the United States.

This statistic is a telling indication of the state of the housing market in the United States. It shows that despite the economic downturn caused by the pandemic, there was still a significant amount of existing homes sold in 2020. This is an important piece of information for anyone interested in mortgage statistics, as it provides insight into the current market conditions and the potential for future growth.

In the third quarter of 2020, the mortgage delinquency rate in the United States was 6.66%.

This statistic is a telling indicator of the state of the mortgage market in the United States. It reveals that, despite the economic downturn caused by the pandemic, the mortgage delinquency rate remains relatively low. This is a positive sign for the housing market, as it suggests that homeowners are managing to keep up with their payments. This statistic is an important piece of information for anyone interested in the mortgage market, as it provides insight into the current state of the market and its potential future.

In 2020, the total volume of mortgage refinancings in the United States was over $2.2 trillion.

This statistic is a testament to the immense impact that mortgage refinancings had on the US economy in 2020. It highlights the sheer magnitude of the refinancing activity that took place, and the significant role it played in helping to stabilize the economy during a tumultuous year. This statistic is a powerful reminder of the importance of mortgage refinancings in the US, and serves as a reminder of the importance of understanding and staying up to date with mortgage statistics.

In 2020, the average down payment on a mortgage in the United States was approximately $46,800.

This statistic is a telling indication of the current state of the mortgage market in the United States. It reveals that the average down payment on a mortgage is quite substantial, indicating that potential homeowners need to have a significant amount of money saved up in order to purchase a home. This statistic is important to consider when discussing mortgage statistics, as it provides insight into the financial requirements of homeownership.

Conclusion

The mortgage market in the United States is a complex and ever-changing landscape. In 2021, total mortgage debt reached $10.9 trillion, with an average interest rate of 3.06%. Purchase loans accounted for 63.3% of all applications while first-time homebuyers typically put down 6%, on average, as their initial payment towards their new homes.

The median loan size was $286,176 and 4.44% of mortgages were in forbearance at one point or another during 2020; however homeownership rates still remained high at 65.8%. Additionally 31% of U.S homeowners have no mortgage debt whatsoever while 33% refinanced last year alone – often taking out cash from these refinances (65%). Average credit scores for approved mortgages were 753 and closing times averaged 51 days throughout 2020; VA loans made up 10 .8 %of originations that same year with subprime lending totaling 1 .18 trillion dollars by the end of it all.

Finally 5 .3 million existing homes sold in 2020 alongside a delinquency rate hovering around 6 .66 % ,with serious delinquencies reaching 2 .9 % by May 2021 Overall this data paints a picture showing how Americans are managing to stay afloat despite economic uncertainty brought about by COVID 19 pandemic – whether through purchase loans or refinancing options such as cash outs – proving that there’s hope yet when it comes to navigating our current financial climate successfully

References

0. – https://www.emlaklobisi.com

1. – https://www.statista.com

2. – https://www.fred.stlouisfed.org

3. – https://www.housingwire.com

4. – https://www.fool.com

5. – https://www.nar.realtor

6. – https://www.va.gov

7. – https://www.mba.org

8. – https://www.businessinsider.com