Elderly Americans face financial challenges in retirement. The median income for elderly households was $25,601 in 2019, and the poverty rate reached 12.8%. Social Security benefits are crucial, with 33% relying on them for 90% or more of their income.

The average benefit is $1,503 per month as of December 2019. Other income sources include pensions (36%), dividends/interest (40%), and employment (14%). Medical expenses can lead to debt, with 56.4% of bankruptcy filers citing medical bills as the primary reason in 2011. Interestingly, 6.5% are not considered low-income by the Supplemental Poverty Measure, despite having incomes below the federal poverty level.

However, overall household incomes have increased by 85% after adjusting for inflation between 1990 and 2016, mainly due to higher pension coverage for those aged 65-69 compared to those aged 75+. Looking ahead to 2045, it is expected that average annual earnings for elderly Americans will increase by 29%, potentially easing economic pressures in this population. Let’s take a closer look at the most important statistics about the financial challenges faced by elderly Americans.

Elderly Income Statistics Overview

In 2018, 33% of elderly adults relied on Social Security for 90% or more of their income.

This statistic is a stark reminder of the financial fragility of elderly adults in the United States. It highlights the fact that a large portion of elderly adults are relying on Social Security for the majority of their income, leaving them vulnerable to any changes in the system or economic downturns. It is a powerful illustration of the need for more secure and reliable sources of income for elderly adults.

As of December 2019, the average Social Security benefit for a retired worker was $1,503 per month.

This statistic is a crucial indicator of the financial well-being of elderly individuals in the United States. It provides insight into the amount of money that retirees are receiving from Social Security, which is often their primary source of income. This statistic is especially important in the context of elderly income statistics, as it can help to inform policy decisions and provide a better understanding of the economic situation of elderly individuals.

Approximately 36% of the elderly population in the United States relies on income from pensions, annuities, or individual retirement accounts (IRAs).

This statistic is a stark reminder of the financial realities faced by many elderly Americans. It highlights the importance of pensions, annuities, and IRAs in providing a steady source of income for a large portion of the elderly population. It also serves as a reminder of the need for financial planning and security for those approaching retirement age.

Of adults aged 65 and older, 14% were still in the labor force in 2019.

This statistic is a telling indication of the financial situation of elderly individuals in the United States. It shows that a significant portion of the elderly population is still actively working, likely due to the need for additional income. This statistic is a reminder that many elderly individuals are struggling to make ends meet and are relying on their labor to supplement their income.

The median income for elderly male workers was approximately $38,000 in 2021, while the median income for elderly female workers was about $26,000.

This statistic is a stark reminder of the gender wage gap that persists in the elderly population. It highlights the fact that elderly female workers are earning significantly less than their male counterparts, despite having the same qualifications and experience. This discrepancy in income can have a significant impact on the quality of life of elderly women, as they may not be able to afford the same level of healthcare, housing, and other necessities as their male counterparts. This statistic is an important reminder of the need to address the gender wage gap in order to ensure that elderly women are able to live with dignity and security.

Nearly 25% of elderly Americans consume more than their income in retirement, which potentially leads to a reduction in net worth.

This statistic is a stark reminder of the financial struggles that elderly Americans face in retirement. It highlights the fact that a significant portion of elderly Americans are unable to sustain their lifestyle with their income, leading to a decrease in their net worth. This is an important issue to consider when discussing elderly income statistics, as it can have a major impact on the financial security of elderly Americans.

Retirees without pensions or annuities have, on average, an income shortfall of $10,000 per year.

This statistic is a stark reminder of the financial struggles that many retirees face without the security of a pension or annuity. It highlights the need for more resources and support for those who are unable to rely on these sources of income in their retirement. It also serves as a warning to those who are planning for their retirement to ensure they have adequate savings and investments to cover their needs.

In 2011, more than half of older Americans (56.4%) who filed for bankruptcy cited medical and credit card debts as the primary reason.

This statistic is a stark reminder of the financial burden that medical and credit card debts can place on elderly Americans. It highlights the need for greater financial security and support for those in later life, particularly when it comes to managing debt. It also serves as a warning to those approaching retirement age to be mindful of their financial situation and to plan ahead for any potential medical costs.

In 2020, 45.8 million Americans aged 65 and older received Social Security benefits.

This statistic is a powerful reminder of the importance of Social Security benefits for elderly Americans. It highlights the sheer number of people who rely on these benefits to make ends meet, and underscores the need for continued support for this population. It also serves as a reminder of the importance of financial planning for retirement, as Social Security benefits may not be enough to cover all of an elderly person’s expenses.

The employment rate for elderly adults, ages 65 to 74, increased from 16.3% in 1990 to 27.3% in 2020.

This statistic is a testament to the changing times and the increasing importance of elderly adults in the workforce. It shows that more and more elderly adults are taking on jobs and contributing to the economy, which is a positive sign for the future of elderly income statistics. It also indicates that the elderly population is becoming more active and engaged in the workforce, which is beneficial for both the elderly and the economy.

The average income for elderly adults in the United States is expected to grow by 29% by 2045.

This statistic is a powerful indicator of the future of elderly adults in the United States. It suggests that, in the coming years, elderly adults can expect to see a significant increase in their income, allowing them to maintain a higher standard of living and greater financial security. This is an important development for elderly adults, as it can help them to better prepare for retirement and ensure that they have the resources they need to live comfortably.

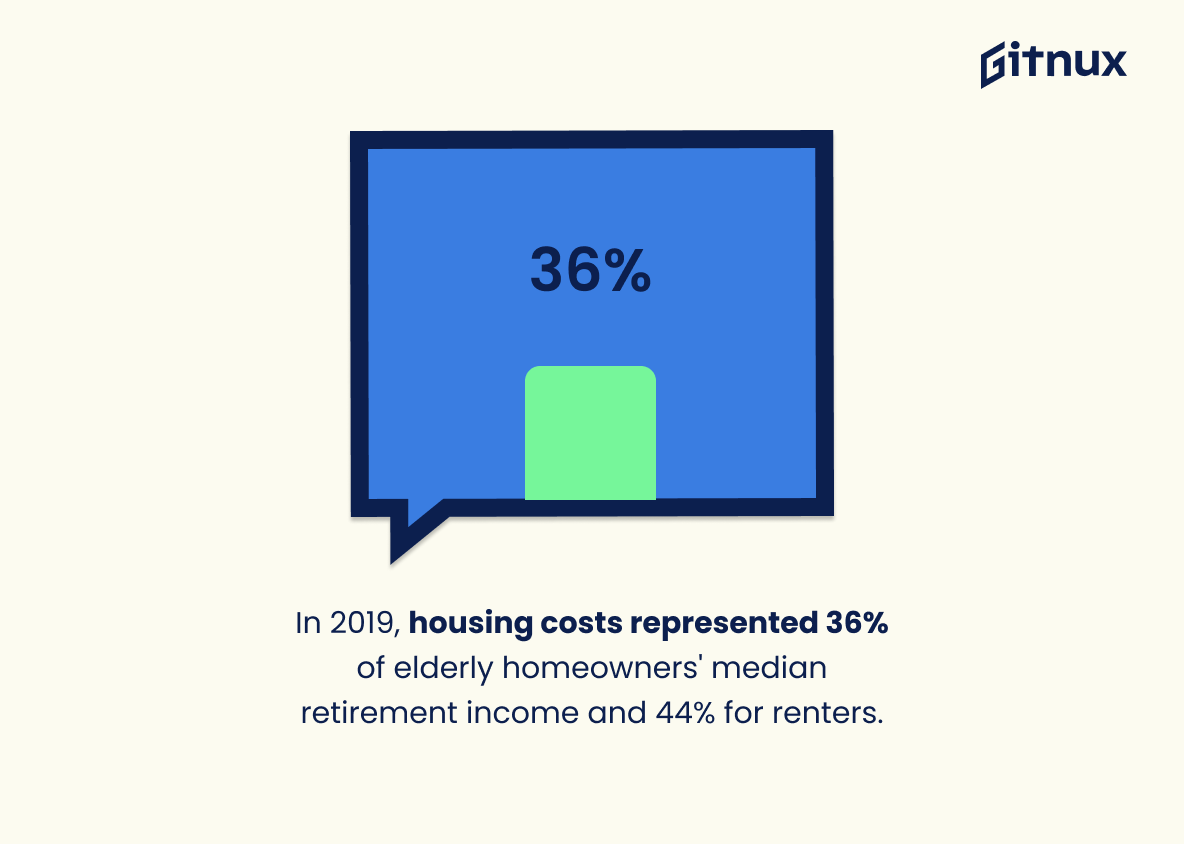

In 2019, housing costs consumed 36% of the median retirement income for elderly homeowners and 44% of the median retirement income for elderly renters.

This statistic is a stark reminder of the financial burden that elderly homeowners and renters face when it comes to housing costs. It highlights the fact that a significant portion of their retirement income is being taken up by housing costs, leaving them with less money to cover other expenses. This is an important issue to consider when discussing elderly income statistics, as it can have a major impact on their quality of life.

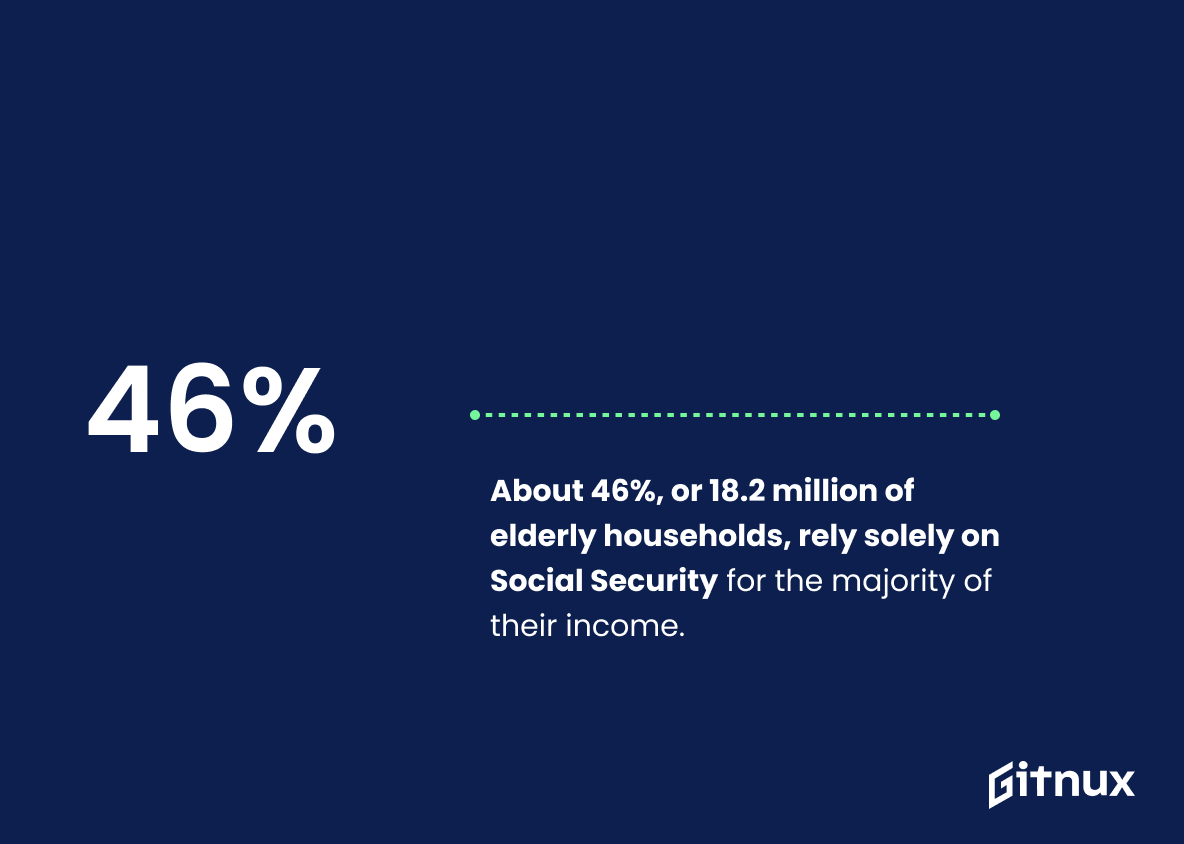

About 46%, or 18.2 million of elderly households, rely solely on Social Security for the majority of their income.

This statistic is a stark reminder of the financial fragility of elderly households in the United States. It highlights the fact that nearly half of elderly households are relying on Social Security as their primary source of income, leaving them vulnerable to any changes in the system or economic downturns. It is a sobering reminder of the importance of ensuring that elderly households have access to adequate and reliable sources of income.

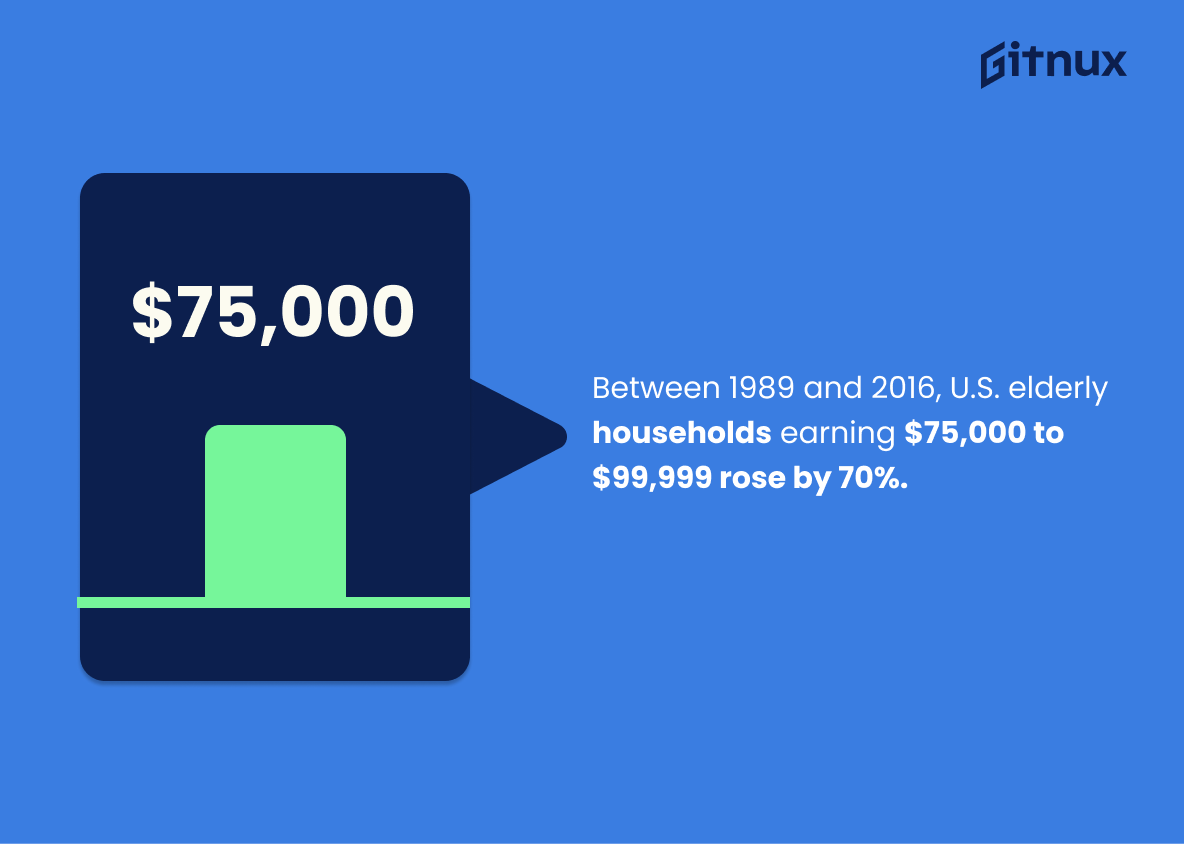

The number of elderly households in the United States with incomes between $75,000 and $99,999 increased by 70% between 1989 and 2016.

This statistic is a powerful indicator of the changing economic landscape for elderly households in the United States. It shows that, over the past 27 years, there has been a significant increase in the number of elderly households with incomes in the upper-middle range. This is an important development, as it suggests that more elderly households are able to maintain a comfortable lifestyle and are less likely to be living in poverty. This statistic is a testament to the progress that has been made in providing financial security for elderly households in the United States.

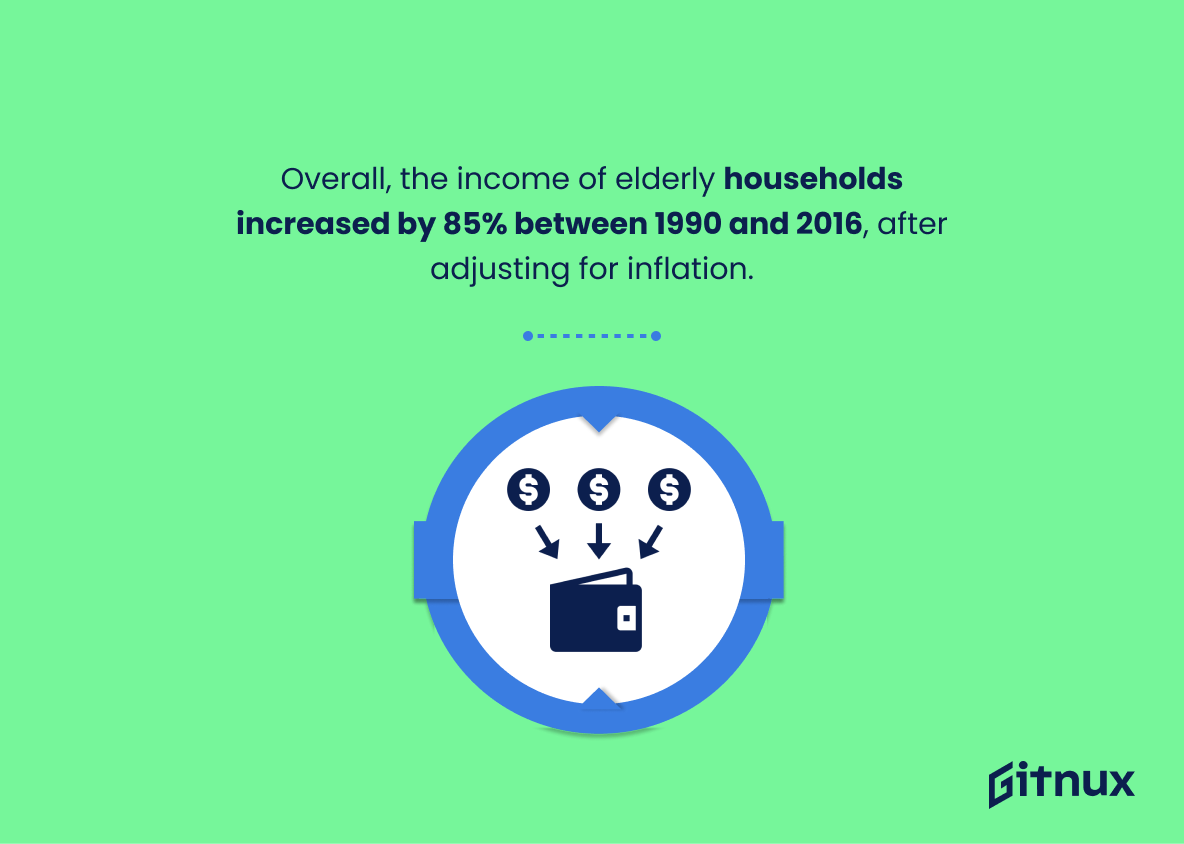

Overall, the income of elderly households increased by 85% between 1990 and 2016, after adjusting for inflation.

This statistic is a powerful indicator of the progress made in improving the financial security of elderly households over the past 26 years. It shows that, despite the effects of inflation, elderly households have seen a significant increase in their income, allowing them to better provide for their needs and enjoy a higher quality of life.

Conclusion

The statistics in this blog post show the financial challenges faced by elderly Americans. In 2019, the median income for the elderly was $25,601, and their poverty rates increased from 9.7% to 12.8%. Social Security provides an average monthly benefit of $1,503 for many older adults. Additionally, 36% rely on pensions, annuities, and IRAs for income, while 14% continue working at age 65 or older.

Dividend and interest incomes from stocks or mutual funds make up 40% of their income, but 25% spend more than they earn annually, leading to reduced net worth over time. Retirees without pensions face a $10k annual shortfall, which can result in medical debt-related bankruptcies if not managed properly.

Currently, 45 million people receive Social Security benefits, and the employment rate for older adults has increased by 11 percentage points since 1990. However, it still lags other age groups due to health issues that limit work capacity late in life. Household incomes have risen by 85% after adjusting for inflation between 1990-2016, but 6% still fall below the federal poverty line when using the Supplemental Poverty Measure criteria.

These figures highlight both positive trends, such as increased access to pension plans and rising wages, and negative ones, such as growing gender inequality with median incomes of $38k for males and $26k for females. They also indicate areas where policymakers could focus on improving economic security among the aging population, including reducing healthcare costs associated with bankruptcy and providing additional support through programs like SSI.

References

0. – https://www.census.gov

1. – https://www.bls.gov

2. – https://www.urban.org

3. – https://www.consumerreports.org

4. – https://www.ssa.gov

5. – https://www.aarp.org

6. – https://www.datausa.io

7. – https://www.jchs.harvard.edu

8. – https://www.dol.gov