As the Baby Boomer generation continues to age, it is important to understand the financial implications of this population. This blog post will explore the financial statistics of Baby Boomers and how their financial decisions may impact the economy. We will look at the amount of wealth Baby Boomers have accumulated, the amount of debt they are carrying, and the types of investments they are making.

We will also discuss the potential implications of Baby Boomers’ financial decisions on the economy and the financial markets. Finally, we will explore how Baby Boomers can best manage their finances to ensure their financial security in retirement.

Financial Realities of Baby Boomers: Important Statistics

$84.4 trillion of wealth will be transferred through 2045, with $72.6 trillion going to heirs and $11.9 trillion to charities.

78% of Baby Boomers increased their usage of fintech tools in 2022.

Financial Realities of Baby Boomers: Statistics Overview

Baby Boomers hold 70% of the disposable income in the U.S. and spend over $548 billion a year, more than any other generation.

Baby Boomers have the highest purchasing power of any generation, which makes them a key target market for businesses and marketers.

The typical Baby Boomer has a median net worth of $206,700. This statistic matters because it gives us an indication of the financial health of Baby Boomers.

On average, Baby Boomers have a significant amount of wealth, which can be used to support their retirement and other financial needs.

$84.4 trillion of wealth will be transferred through 2045, with $72.6 trillion going to heirs and $11.9 trillion to charities.

This highlights the potential for a large transfer of wealth from Baby Boomers to their heirs and to charities. This could have a significant impact on the distribution of wealth in the coming years, as well as on the financial stability of charities.

Baby Boomers now own 27% of all U.S. wealth, up from 20% three decades ago, and their wealth is 157% of the U.S. GDP.

Baby Boomers have accumulated a large amount of wealth over the past three decades, and their wealth is significantly larger than the U.S. GDP. This indicates that Baby Boomers have a large amount of financial power and influence in the U.S. economy.

23% of Baby Boomers prefer digital wallets over traditional methods of transferring money.

Baby Boomers are increasingly embracing digital technology for their financial needs, which is important for businesses to recognize when targeting this demographic.

78% of Baby Boomers increased their usage of fintech tools in 2022.

Baby Boomers are increasingly using technology to manage their finances, which is a significant shift from traditional methods. This shift is likely to have a positive impact on their financial security and well-being, as fintech tools can provide more efficient and secure ways to manage finances.

48% of Baby Boomers feel comfortable with their savings, 20% are ahead of the game, 14% are just getting started, 13% feel behind, and 5% are lost and confused.

The majority of Baby Boomers are in a good financial position, but there is still a significant portion that are struggling and need help. This can help inform policy makers and financial advisors on how to best help Baby Boomers manage their finances.

The median retirement savings balance among Baby Boomers is $202,000, which is a small amount of income on an annual basis.

Baby Boomers are not adequately prepared for retirement, as their savings are not enough to provide a comfortable lifestyle. This could lead to financial insecurity in their later years, and could have a significant impact on their quality of life.

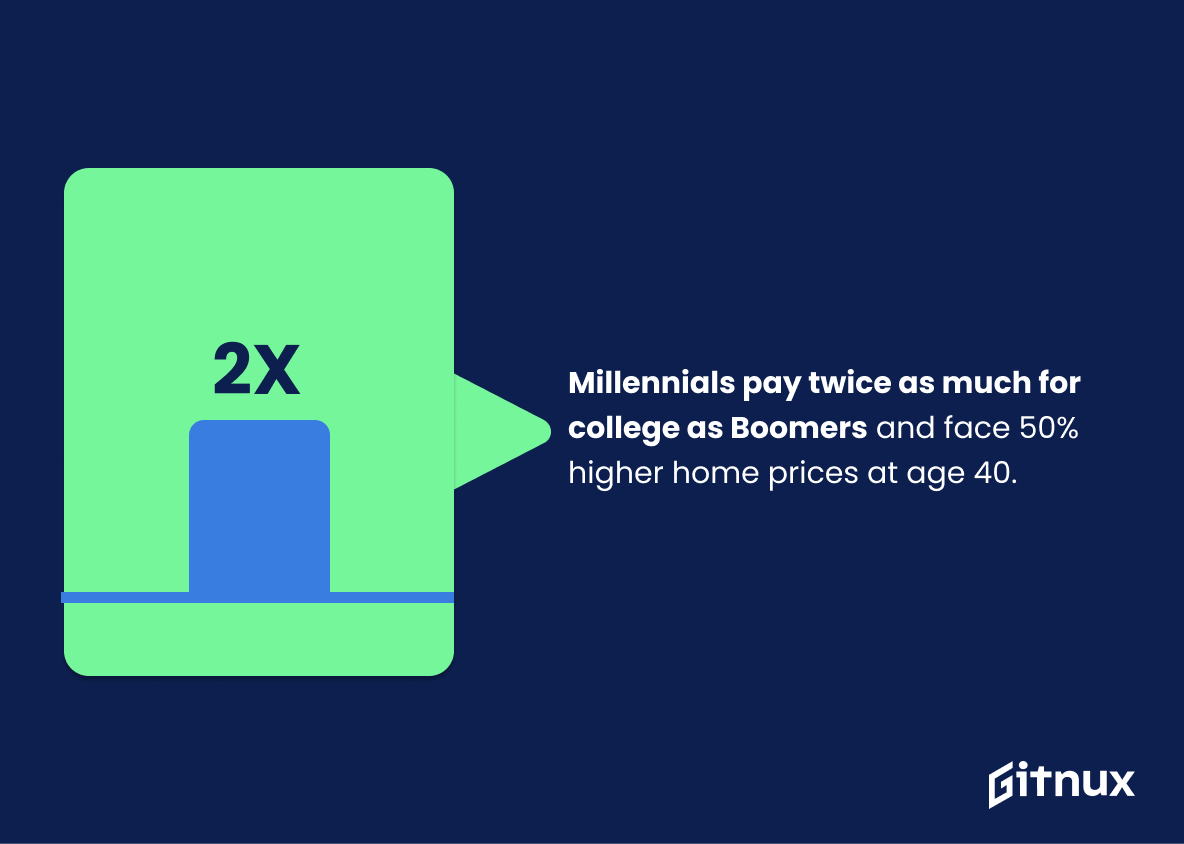

Millennials pay over double the cost of college that Boomers paid, and the median cost of a home has increased by over 50% since Boomers were 40.

This highlights the financial disparities between Millennials and Boomers. Millennials are facing a much higher cost of college than Boomers did, and the cost of a home has increased significantly since Boomers were 40.

This has implications for Millennials’ ability to save for retirement and purchase a home, which could have long-term financial consequences.

The average Baby Boomer was 65% richer than previous generations by age 60.

Baby Boomers have been able to accumulate more wealth than previous generations. This is important because it shows that Baby Boomers have been able to save more money and have more financial security in retirement. This could be due to higher wages, increased savings, or other factors.

Supplementary Statistics

Baby Boomers hold over 50% of the total household wealth in the United States.

This speaks to the immense economic influence Baby Boomers have, and the potential for them to shape the future of the country’s economy. It also highlights the importance of understanding the financial habits and needs of Baby Boomers, so that their wealth can be managed responsibly and used to benefit the nation as a whole.

The median retirement savings for Baby Boomers is $144,000.

It reveals that the median retirement savings for this generation is a substantial amount, suggesting that many Baby Boomers have been able to save a significant amount of money for their retirement. This statistic is important to consider when discussing the financial state of Baby Boomers, as it provides insight into the financial security of this generation.

13% of Baby Boomers have no retirement savings at all.

This is a stark reminder of the financial struggles that Baby Boomers face as they approach retirement. It highlights the need for more financial education and planning to ensure that Baby Boomers are able to secure their financial future.

Baby Boomers represent about 73% of charitable donors in the United States.

It highlights the importance of this generation in terms of their financial contributions to the greater good. It also serves as a reminder of the importance of understanding the financial habits of Baby Boomers in order to ensure that their generosity continues to benefit those in need.

Baby Boomers are expected to transfer $30 trillion in wealth to younger generations over the next few decades.

This speaks to the sheer magnitude of wealth that will be transferred, and the potential for generational wealth to be created. It also highlights the importance of financial planning for Baby Boomers, as they will be responsible for the financial well-being of their heirs. This statistic is a reminder of the importance of Baby Boomers in the economy and the need to ensure their financial security.

66% of Baby Boomers own stocks or stock mutual funds.

The majority of this generation has invested in stocks or stock mutual funds, which suggests that they are taking steps to ensure their financial stability. This is an important statistic to consider when discussing the financial health of Baby Boomers.

32% of Baby Boomers have a written financial plan.

The fact that only 32% of Baby Boomers have a written financial plan is a telling statistic that speaks to the importance of financial planning for this generation. It displays the need for Baby Boomers to take a proactive approach to their financial future and to ensure that they have a plan in place to protect their assets and secure their retirement.

Baby Boomers have an average 401(k) account balance of $210,000.

Baby Boomers have an average net worth of $1.2 million.

This serves as a reminder of the importance of financial planning and investing for future generations, and provides a benchmark for other generations to strive for.

More than 40% of Baby Boomers still have a mortgage on their primary residence.

A large portion of this generation is still struggling to pay off their mortgages, despite being in the later stages of their lives. This statistic is a reminder that Baby Boomers need to be mindful of their financial decisions and plan for their retirement.

Baby Boomers spend an average of $3,800 per month in retirement.

This is an important piece of the puzzle when it comes to understanding the financial health of Baby Boomers and the impact they have on the economy.

56% of Baby Boomers plan to continue working past the age of 65.

A majority of Baby Boomers are planning to remain in the workforce beyond the traditional retirement age. This could have a major impact on the financial landscape of the Baby Boomer generation, as they may be able to continue to earn income and save for retirement, while also potentially delaying the need to draw down on their retirement savings.

41% of Baby Boomers expect Social Security to be their primary source of income in retirement.

It suggests that a large portion of this generation is relying on Social Security to provide the majority of their income in retirement, which could be a sign of inadequate savings or other financial issues. This statistic is important to consider when discussing Baby Boomer financial statistics, as it provides insight into the financial security of this generation.

Baby Boomers currently make up 21% of the U.S. population.

This speaks to the sheer size of the Baby Boomer generation and the impact they have on the economy, politics, and culture. This statistic is essential to understanding the financial implications of the Baby Boomer generation and how their decisions and actions affect the nation as a whole.

Baby Boomers have an average credit score of 731.

Thus, this generation is well-equipped to handle their finances responsibly and make sound financial decisions. This statistic is a testament to the financial success of Baby Boomers and serves as a reminder of their impressive financial acumen.

Baby Boomers are 33% more likely to fall victim to investment scams than other age groups.

As they are more likely to fall victim to investment scams, it is essential that they are aware of the risks and take steps to protect themselves. It is also important to note that Baby Boomers are not the only age group at risk of investment scams, and that all age groups should be vigilant when it comes to their finances.

Baby Boomers will make up 24% of the workforce by 2024.

As Baby Boomers make up an increasingly larger portion of the workforce, it is essential to be aware of their financial habits and needs in order to ensure their financial security.

Baby Boomers started 46% of all small businesses.

This statistic is a testament to the entrepreneurial spirit of Baby Boomers, demonstrating their ability to create and sustain small businesses. It speaks to their resourcefulness and resilience, and serves as a reminder of the immense economic contributions they have made to society.

Conclusion

In conclusion, Baby Boomers have a unique set of financial challenges and opportunities. They have a large amount of wealth, but they are also facing a number of financial issues such as rising healthcare costs, increased debt, and a lack of retirement savings.

Despite these challenges, Baby Boomers have the potential to be successful financially and to enjoy a comfortable retirement. With careful planning and the right strategies, Baby Boomers can make the most of their financial resources and secure a comfortable retirement.

References

1 – https://www.buxtonco.com/blog/the-lost-generation-baby-boomers

2 – https://www.businessinsider.com/typical-baby-boomer-net-worth-debt-real-estate-retirement-2021-12

3 – https://fortune.com/recommends/investing/baby-boomers-average-net-worth/

4 – https://www.axios.com/2021/07/03/baby-boomers-wealth-inheritance-millennials

5 – https://www.finder.com/baby-boomer-money-statistics

6 – https://sundayworld.co.za/news/business/baby-boomers-the-biggest-users-of-fintech-tools-followed-by-gen-x/

7 – https://www.alert-1.com/resources/baby-boomer-facts-and-statistics/426

8 – https://www.fool.com/retirement/2021/08/24/heres-baby-boomers-median-retirement-savings-balan/

9 – https://trustandwill.com/learn/generational-wealth-gap

10 – https://fortune.com/2022/10/27/millennials-versus-boomers-wealth-gap-doubled/

11 – https://www.businessinsider.com

12 – https://www.smartaboutmoney.org

13 – https://nonprofitquarterly.org

14 – https://www.fool.com

15 – https://www.bls.gov

16 – https://www.transamericacenter.org

17 – https://www.forbes.com

18 – https://www.experian.com

19 – https://www.valuepenguin.com

20 – https://www.gallup.com

21 – https://www.cnbc.com

22 – https://www.ftc.gov