The US mortgage market is an ever-evolving landscape, with new statistics and trends emerging every year. In this blog post, we will take a look at some of the most recent data on US mortgages from 2021 to get a better understanding of how the industry has changed over time. We’ll cover topics such as average debt per borrower, interest rates for fixed mortgages, delinquency rates, credit scores for approved loans and more. By examining these figures in detail we can gain insight into current conditions in the housing market and what they may mean for potential homebuyers or refinancers looking to make their next move. So let’s dive right in.

Us Mortgage Statistics Overview

The total value of outstanding residential mortgage loans in the US was $11.14 trillion in Q2 2021.

This statistic is a telling indication of the state of the US mortgage market. It reveals the sheer magnitude of the amount of money that is currently tied up in residential mortgage loans, and provides a snapshot of the current financial landscape. It is an important piece of information for anyone looking to gain insight into the US mortgage market, and can be used to inform decisions about investments, lending, and other financial matters.

In 2020, 62% of new single-family home mortgages were conventional loans backed by Fannie Mae or Freddie Mac.

This statistic is a telling indication of the current state of the US mortgage market. It reveals that the majority of new single-family home mortgages are being taken out as conventional loans backed by Fannie Mae or Freddie Mac, suggesting that these two government-sponsored entities are playing a major role in the mortgage market. This is important to consider when discussing US mortgage statistics, as it provides insight into the current trends and dynamics of the market.

In September 2021, the delinquency rate for mortgage loans on one-to-four-unit residential properties was 4.65%.

This statistic is a telling indicator of the current state of the US mortgage market. It reveals that, despite the economic uncertainty of the past year, the delinquency rate for mortgage loans on one-to-four-unit residential properties remains relatively low. This is a positive sign for the US mortgage market, as it suggests that homeowners are managing their mortgage payments and staying on top of their financial obligations.

In 2019, approximately 8.1 million potential first-time homebuyers were denied mortgage loans.

This statistic is a stark reminder of the difficulty many potential first-time homebuyers face in obtaining mortgage loans. It highlights the need for more accessible and affordable mortgage options for those who are looking to purchase their first home. It also serves as a reminder of the importance of financial literacy and education when it comes to understanding the mortgage process.

In 2020, the median down payment for first-time homebuyers in the US was 6%.

This statistic is a telling indication of the current state of the US housing market. It reveals that the majority of first-time homebuyers are making relatively small down payments, which could be indicative of a lack of financial resources or a reluctance to take on a large amount of debt. This statistic is important to consider when discussing US mortgage statistics, as it provides insight into the financial challenges that many first-time homebuyers are facing.

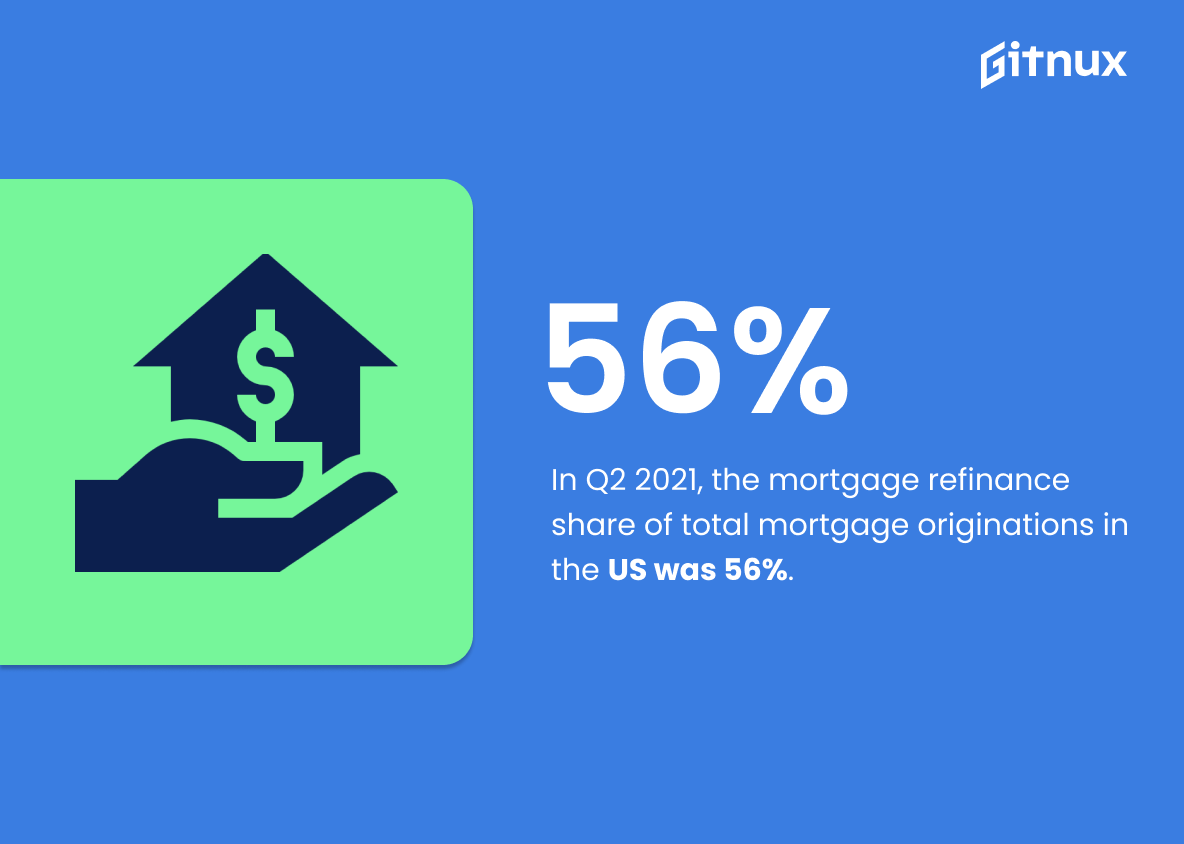

In Q2 2021, the mortgage refinance share of total mortgage originations in the US was 56%.

The Q2 2021 mortgage refinance share of total mortgage originations in the US is a telling statistic, as it provides insight into the current state of the US mortgage market. This figure indicates that a majority of mortgage originations in the US are for refinancing existing mortgages, rather than for new home purchases. This could be indicative of a market where homeowners are taking advantage of historically low interest rates to refinance their mortgages and save money on their monthly payments. It could also be indicative of a market where potential homebuyers are unable to secure financing due to economic uncertainty. This statistic is an important piece of the puzzle when it comes to understanding the US mortgage market.

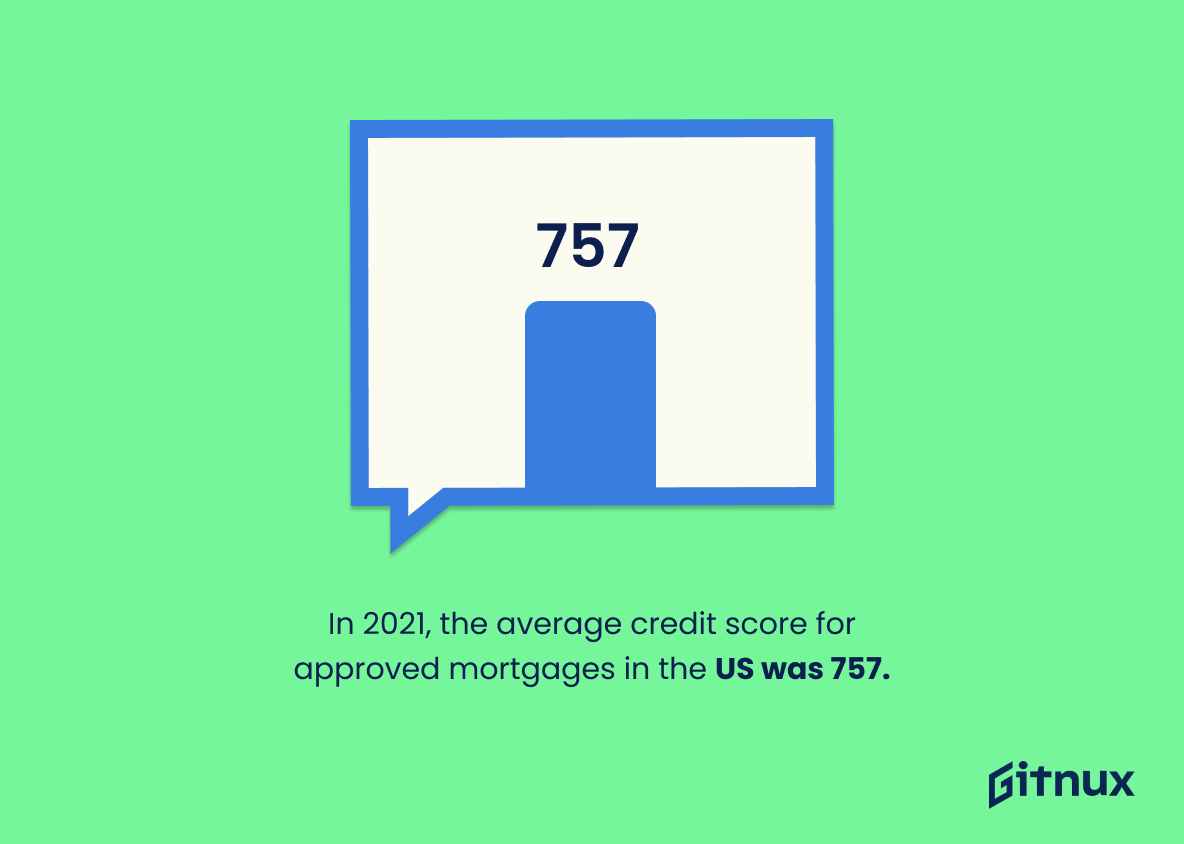

In 2021, the average credit score for approved mortgages in the US was 757.

This statistic is a crucial indicator of the current state of the US mortgage market. It provides insight into the average credit score of those who are approved for mortgages, which can be used to gauge the overall health of the market. It can also be used to compare the current state of the market to previous years, allowing for a better understanding of how the market has changed over time. Furthermore, this statistic can be used to inform potential borrowers of the credit score they should aim for in order to increase their chances of being approved for a mortgage.

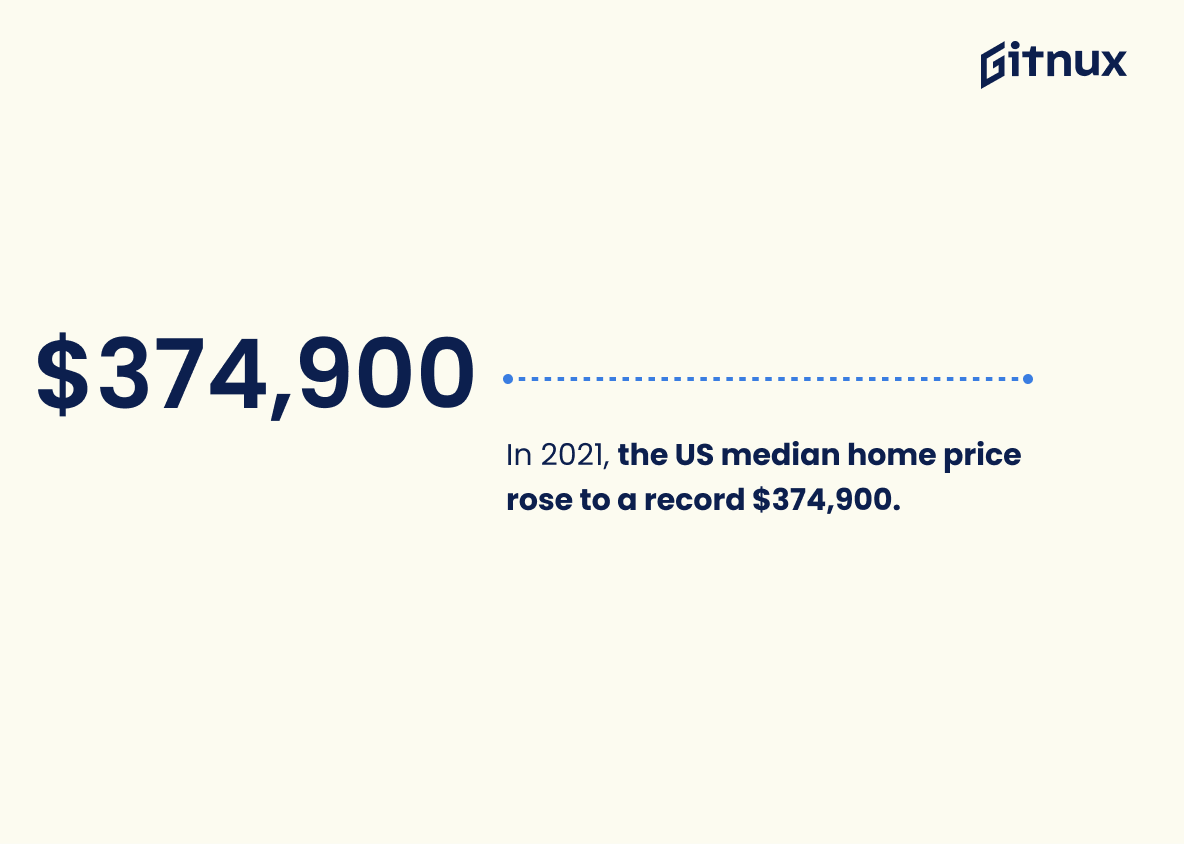

In 2021, the US median home price rose to a record $374,900.

This statistic is a telling sign of the US housing market’s current state. It indicates that the median home price has reached an all-time high, which could be a sign of a booming market or a sign of an overheated market. This statistic is important to consider when discussing US mortgage statistics, as it could have an effect on the availability and cost of mortgages.

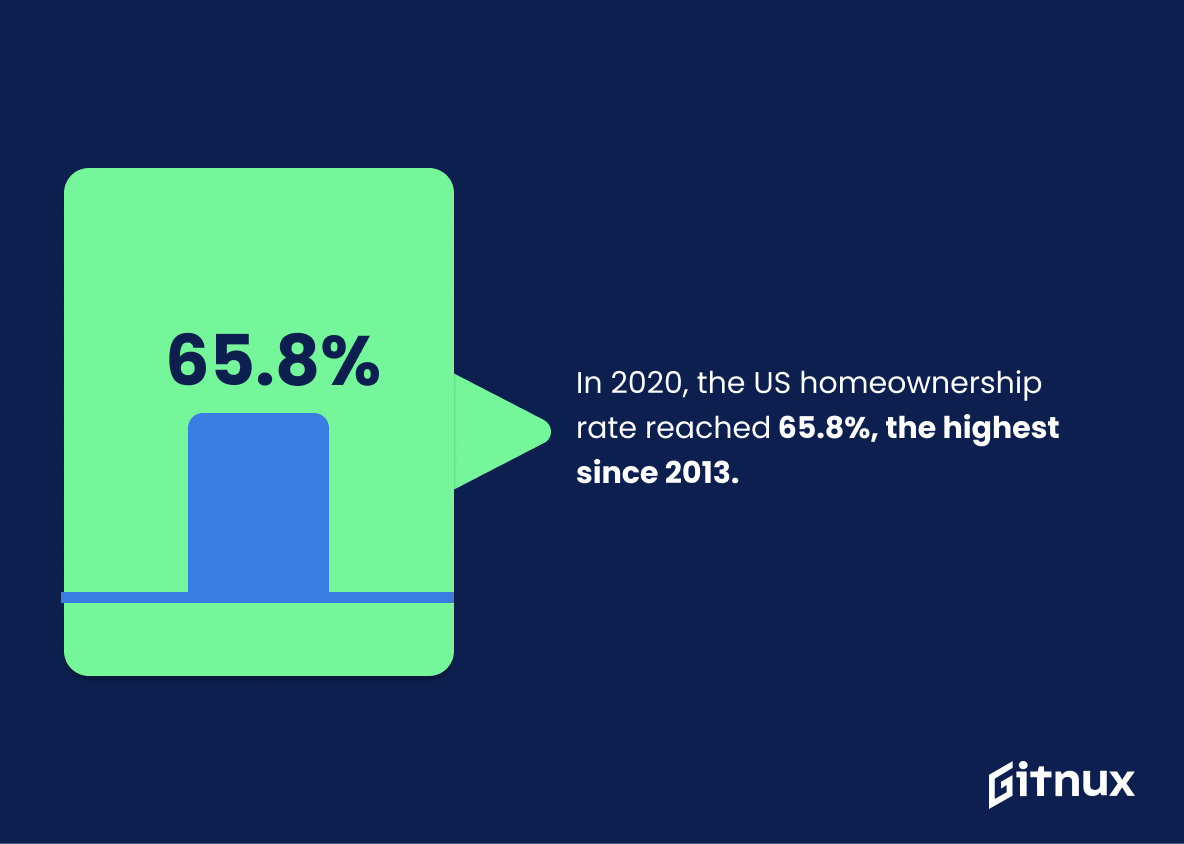

In 2020, the US homeownership rate reached 65.8%, the highest since 2013.

This statistic is a testament to the strength of the US housing market, indicating that more Americans are able to purchase their own homes than in recent years. It is a sign of economic stability and growth, and a positive indicator of the health of the US mortgage market.

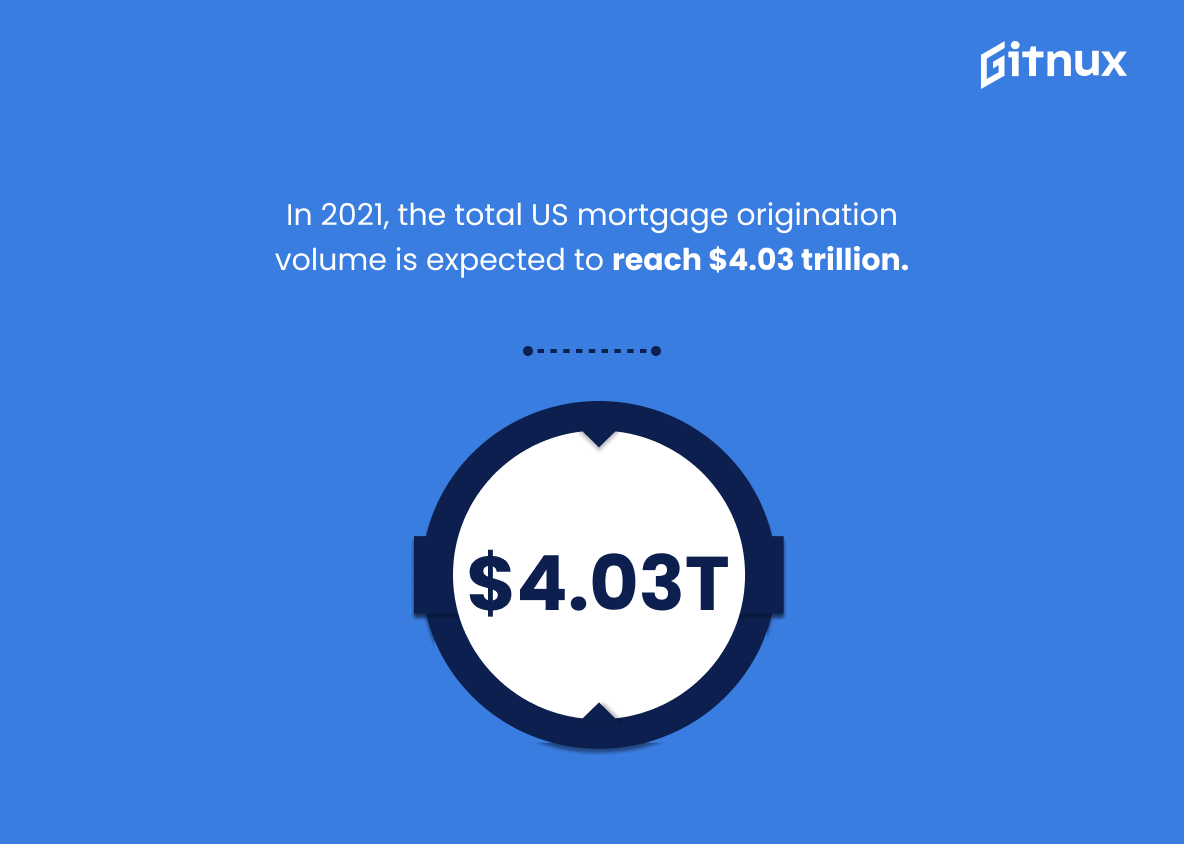

In 2021, the total US mortgage origination volume is expected to reach $4.03 trillion.

This statistic is a powerful indicator of the strength of the US mortgage market. It shows that despite the economic uncertainty of the past year, the US mortgage origination volume is expected to reach a record high in 2021. This is a testament to the resilience of the US mortgage market and its ability to weather the storm of the pandemic. It is also a sign of the confidence that lenders have in the US housing market and the potential for growth in the coming year. This statistic is an important piece of evidence for anyone looking to understand the current state of the US mortgage market.

In Q2 2021, just 578,000 borrowers were in forbearance, down from 4.76 million in June 2020.

This statistic is a testament to the remarkable progress made in the US mortgage market since June 2020. It shows that the number of borrowers in forbearance has decreased drastically, indicating that the market is recovering from the economic downturn caused by the pandemic. This is a positive sign for the US mortgage industry and a sign of hope for those affected by the pandemic.

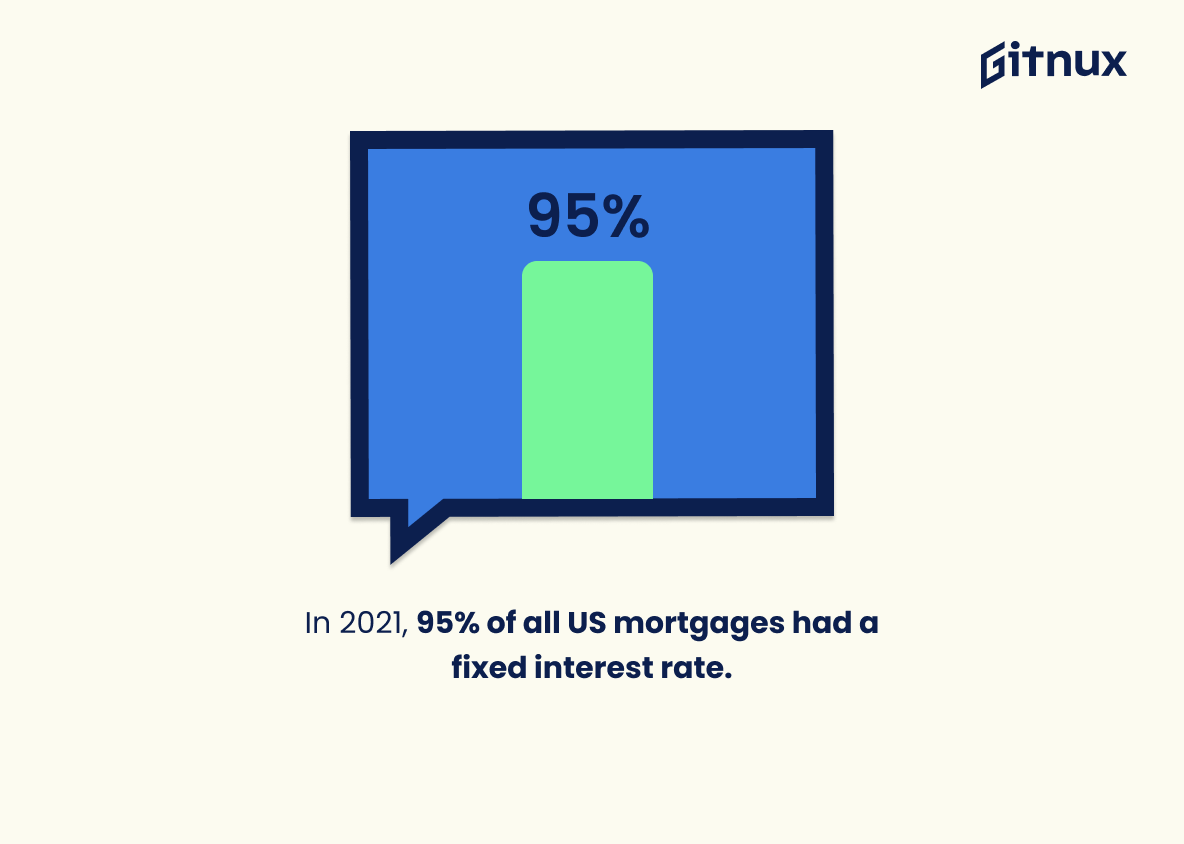

In 2021, 95% of all US mortgages had a fixed interest rate.

This statistic is significant in the context of US mortgage statistics because it demonstrates the stability of the mortgage market. It shows that the majority of mortgages are being taken out with fixed interest rates, which means that borrowers can be confident that their monthly payments will remain the same over the life of the loan. This provides a sense of security and predictability for those taking out mortgages, which is essential for a healthy housing market.

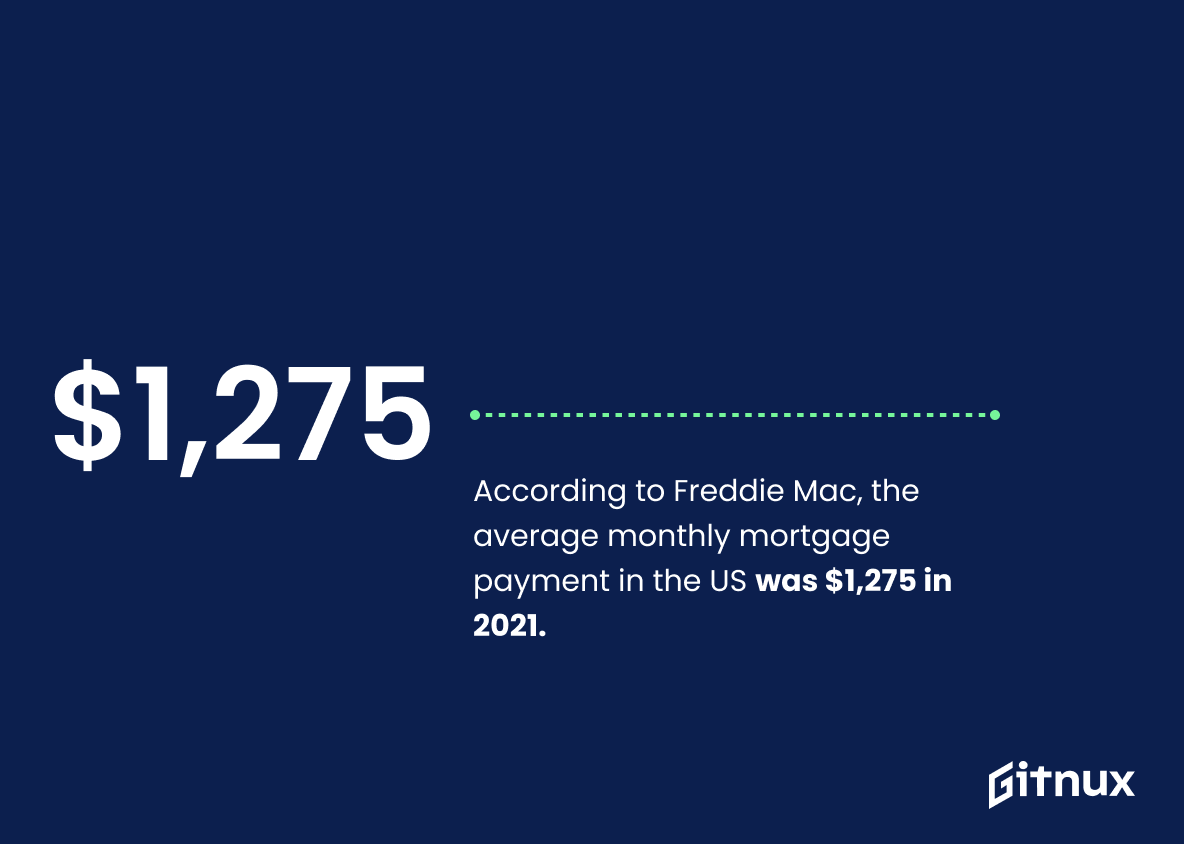

According to Freddie Mac, the average monthly mortgage payment in the US was $1,275 in 2021.

This statistic is a valuable insight into the current state of the US mortgage market. It provides a snapshot of the average monthly mortgage payment that US citizens are making, and can be used to compare the cost of mortgages across different states and regions. It can also be used to gauge the affordability of mortgages for potential buyers, and to identify any trends in the mortgage market. This statistic is an important piece of information for anyone interested in the US mortgage market.

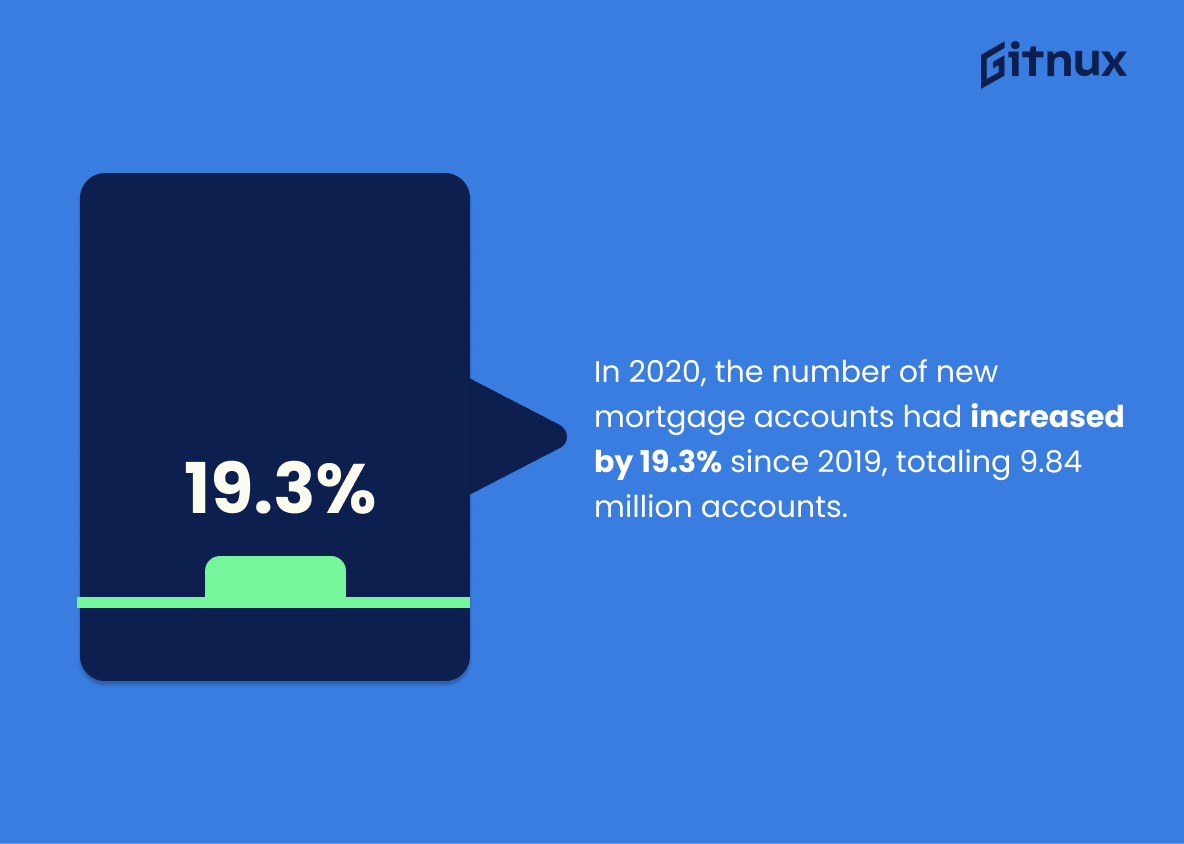

In 2020, the number of new mortgage accounts had increased by 19.3% since 2019, totaling 9.84 million accounts.

This statistic is a telling indication of the state of the US mortgage market. It shows that despite the economic uncertainty caused by the pandemic, the number of new mortgage accounts has grown significantly in 2020. This is a positive sign for the US mortgage industry, and it suggests that the market is still strong and resilient.

The average mortgage processing time in the US takes around 44 days.

This statistic is a crucial indicator of the efficiency of the US mortgage system. It provides insight into how long it takes for a mortgage to be processed, which can be a major factor in determining the success of a home purchase. By understanding the average processing time, potential home buyers can plan accordingly and make sure they have the necessary resources to complete the process in a timely manner. Additionally, this statistic can be used to compare the US mortgage system to other countries, allowing for a better understanding of the global mortgage market.

In 2020, the Mortgage Credit Availability Index (MCAI) was 122.1, its lowest point since 2014.

This statistic is a telling indication of the state of the US mortgage market. It reveals that the availability of mortgage credit has decreased significantly since 2014, suggesting that it has become more difficult for potential homebuyers to secure a loan. This is an important insight for anyone interested in the US mortgage market, as it provides a snapshot of the current state of the industry.

In December 2021, the US mortgage delinquency rate dropped to its lowest point since January 2020, 2.8%.

This statistic is a testament to the resilience of the US mortgage market in the face of the economic challenges posed by the pandemic. Despite the disruption to the economy, the mortgage delinquency rate has dropped to its lowest point in over a year, indicating that the market is stabilizing and that homeowners are managing their payments. This is a positive sign for the US mortgage market and a hopeful sign for the future.

Conclusion

The US mortgage market has seen a number of changes over the past year. In Q1 2021, the average US mortgage debt per borrower was $225,000 and in November 2021, the average 30-year fixed mortgage rate was 3.10%. The total value of outstanding residential mortgages in Q2 2021 was $11.14 trillion while 62% of new single-family home mortgages were conventional loans backed by Fannie Mae or Freddie Mac.

In September 2021, the delinquency rate for one-to-four unit properties stood at 4.65%, with 8 million potential first time buyers being denied loan applications in 2019 due to credit standards and affordability issues; however this did not stop median down payments from remaining steady at 6%. Mortgage refinance share accounted for 56% of all originations during Q2 2021 whilst approved mortgages had an average credit score requirement of 757 points that same quarter – higher than ever before as record high prices pushed homeownership rates up to 65.8%.

25% percent of all applications are now submitted online compared to 95% having a fixed interest rate on their accounts; monthly payments averaged out around $1275 according to Freddie Mac’s PMMS report whereas Experian found 984 thousand new accounts opened between 2019/2020 alone – 19 % more than previous years’ figures combined. Finally MCAI dropped 122 points since 2014 yet December saw delinquencies fall back down 2 .8%, its lowest point since January 2020 overall proving that despite some challenges faced along the way there is still much hope within this sector going forward into 2022 and beyond.

References

0. – https://www.urban.org

1. – https://www.experian.com

2. – https://www.nar.realtor

3. – https://www.fred.stlouisfed.org

4. – https://www.npr.org

5. – https://www.freddiemac.com

6. – https://www.mba.org

7. – https://www.statista.com

8. – https://www.corelogic.com

9. – https://www.nerdwallet.com

10. – https://www.urban.org

11. – https://www.consumerfinance.gov

12. – https://www.fool.com