Mortgage fraud is a serious issue that has been on the rise in recent years. According to the Federal Bureau of Investigation, it costs the United States an estimated $1-10 billion per year. In 2020 alone, there was a 938% increase in suspicious activity reports related to mortgage fraud from 2019. CoreLogic reported a 12.4% year-over-year increase in mortgage fraud risk during 2018’s second quarter and Florida ranked first with its Risk Index value of 292 for 2020.

Mortgage fraud cases resulted in an average loss of $1.2 million among financial institutions while income fraud represented over 30% of fraudulent applications last year according to Fannie Mae’s report on avoiding mortgage fraud. The Federal Reserve estimates between 600,000 and 1,200,000 homeowners experienced some form of mortgage fraud during 2020 as well; 74 percent involved owner occupied properties according to Financial Samurai’s research into occupancy rates.

Radian found 10.7 percent growth rate from 2016 – 2017 when looking at their data regarding key trends within this area , while Corelogic noted 70 percent occurred during loan origination leading up to 2008 housing market crash . It is also believed that due to these activities home prices can be inflated by 5%.

In 2018 alone 3 billion dollars were stopped by financial institutions before they could cause any damage but 43 % still managed misrepresentation property or transaction details along with 15 % identity theft cases being reported throughout 2019 (Credit Karma). U S lawyer office sued Barclays for securities which led 90 % increased prosecutions compared 2017 & government lost 7 billions 2009 – 2011(American Bar Association) 60+percent incidents occur within 90 days after origination (Loan Officer Hub )and finally FinCEN recorded 1200+cases just Q1/2020.(FinCen)

This staggering statistic serves as a stark reminder of the immense financial damage that mortgage fraud can cause. It is a sobering reminder that this type of crime is not only illegal, but also has a significant economic impact on the country. The fact that such a large amount of money is lost each year to mortgage fraud should be a wake-up call to all involved in the mortgage industry to take steps to prevent and detect this type of fraud.

In 2020, there was a 938% increase in suspicious activity reports of mortgage fraud from 2019.

This statistic is a stark reminder of the alarming rise in mortgage fraud in 2020. It serves as a wake-up call to lenders, borrowers, and other stakeholders in the mortgage industry to take proactive steps to protect themselves from fraudulent activities. The 938% increase in suspicious activity reports of mortgage fraud is a clear indication that more needs to be done to combat this growing problem.

Mortgage Fraud Statistics Overview

CoreLogic reported a 12.4% year-over-year increase in mortgage fraud risk in the second quarter of 2018.

This statistic is a stark reminder of the growing prevalence of mortgage fraud in the current market. It highlights the need for lenders and borrowers alike to be vigilant in their efforts to protect themselves from fraudulent activity. The 12.4% year-over-year increase in mortgage fraud risk is a cause for concern and should be taken seriously by all parties involved in the mortgage process.

Florida ranked first in mortgage fraud risk in 2020 with a Risk Index value of 292.

The fact that Florida ranked first in mortgage fraud risk in 2020 with a Risk Index value of 292 is a stark reminder of the prevalence of this type of crime. It serves as a warning to potential homeowners and lenders that they must remain vigilant in order to protect themselves from becoming victims of mortgage fraud. This statistic is a powerful reminder that mortgage fraud is a serious issue that must be addressed.

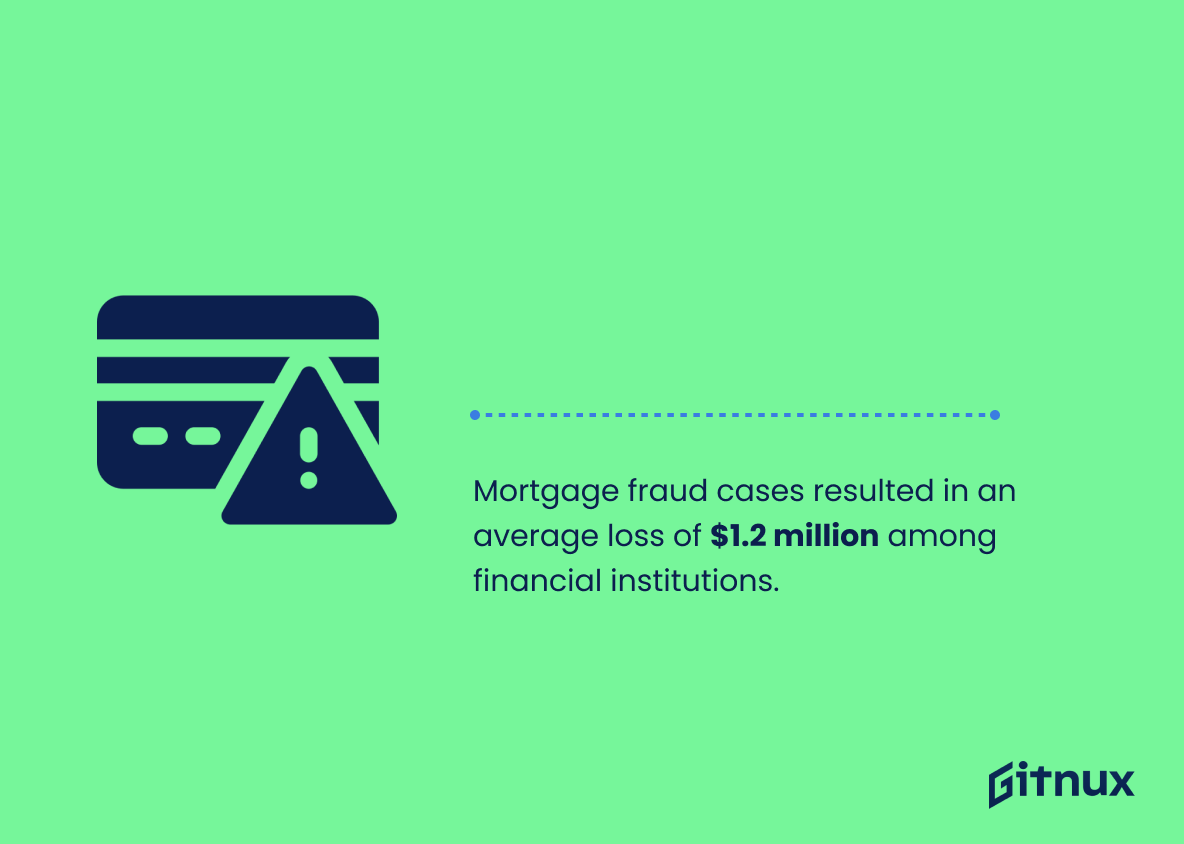

Mortgage fraud cases resulted in an average loss of $1.2 million among financial institutions.

This statistic is a stark reminder of the devastating financial impact that mortgage fraud can have on financial institutions. With an average loss of $1.2 million, it is clear that mortgage fraud is a serious problem that needs to be addressed. The high cost of mortgage fraud is a reminder of the importance of taking steps to prevent it.

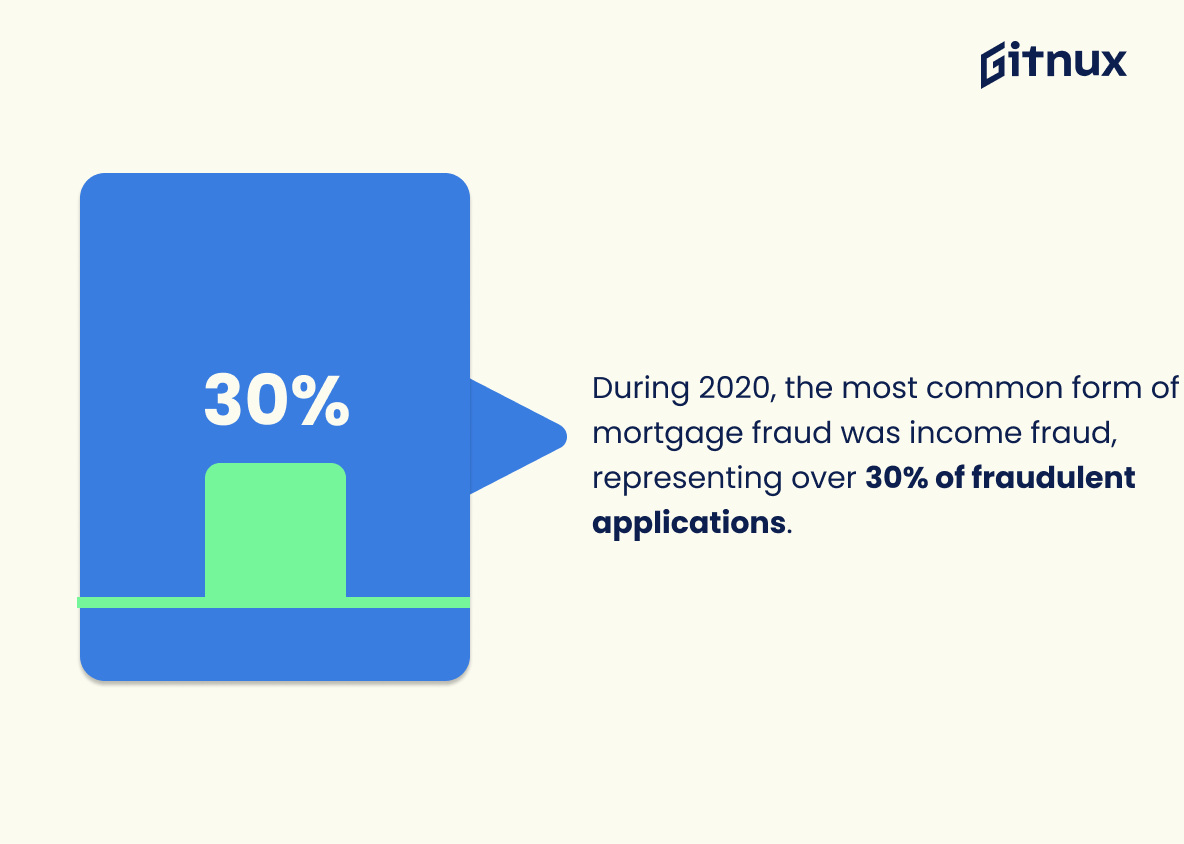

During 2020, the most common form of mortgage fraud was income fraud, representing over 30% of fraudulent applications.

This statistic is a stark reminder of the prevalence of income fraud in the mortgage industry. It highlights the need for lenders to be vigilant in their efforts to detect and prevent fraudulent applications. It also serves as a warning to potential borrowers to be aware of the risks associated with mortgage fraud and to take steps to protect themselves.

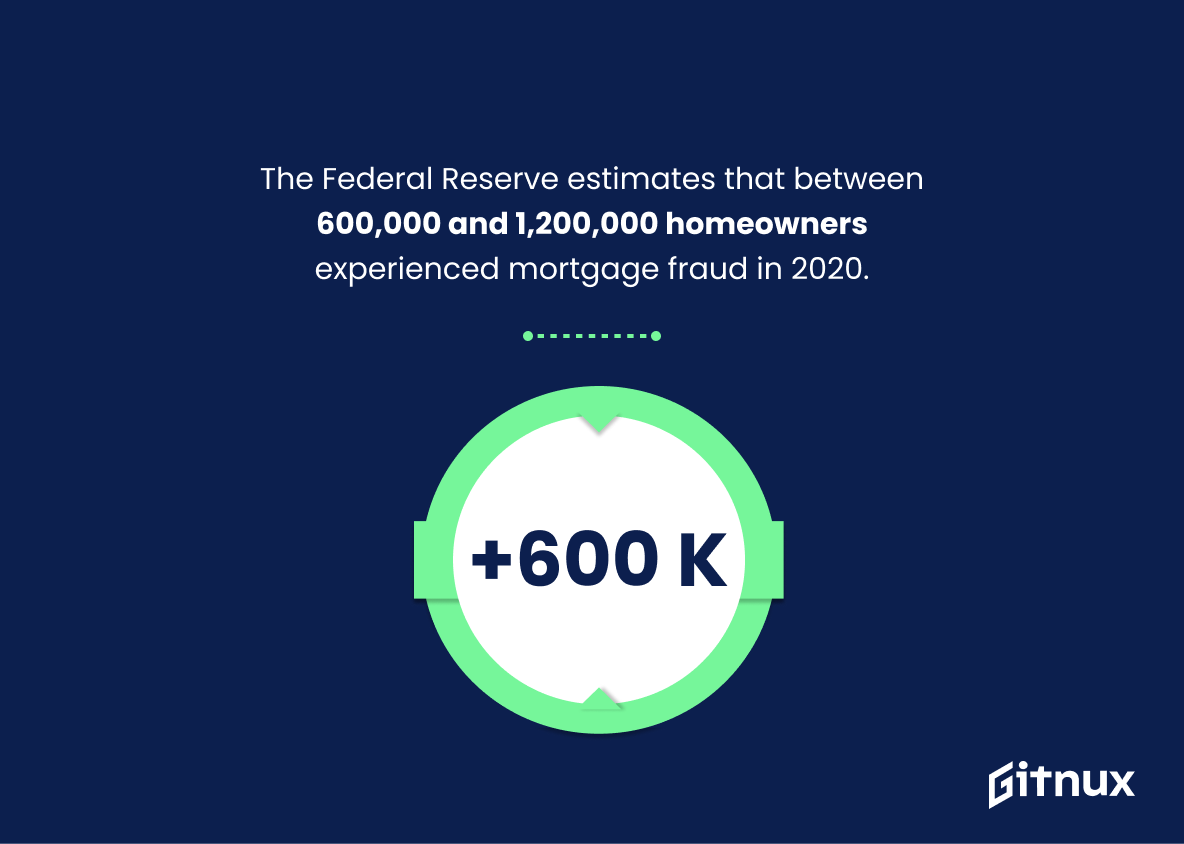

The Federal Reserve estimates that between 600,000 and 1,200,000 homeowners experienced mortgage fraud in 2020.

This statistic is a stark reminder of the prevalence of mortgage fraud in 2020. It highlights the need for greater awareness and vigilance when it comes to protecting homeowners from fraudulent activities. It also serves as a warning to potential homeowners to be extra cautious when entering into a mortgage agreement. The fact that the Federal Reserve estimates that between 600,000 and 1,200,000 homeowners experienced mortgage fraud in 2020 is a clear indication that this is an issue that needs to be addressed.

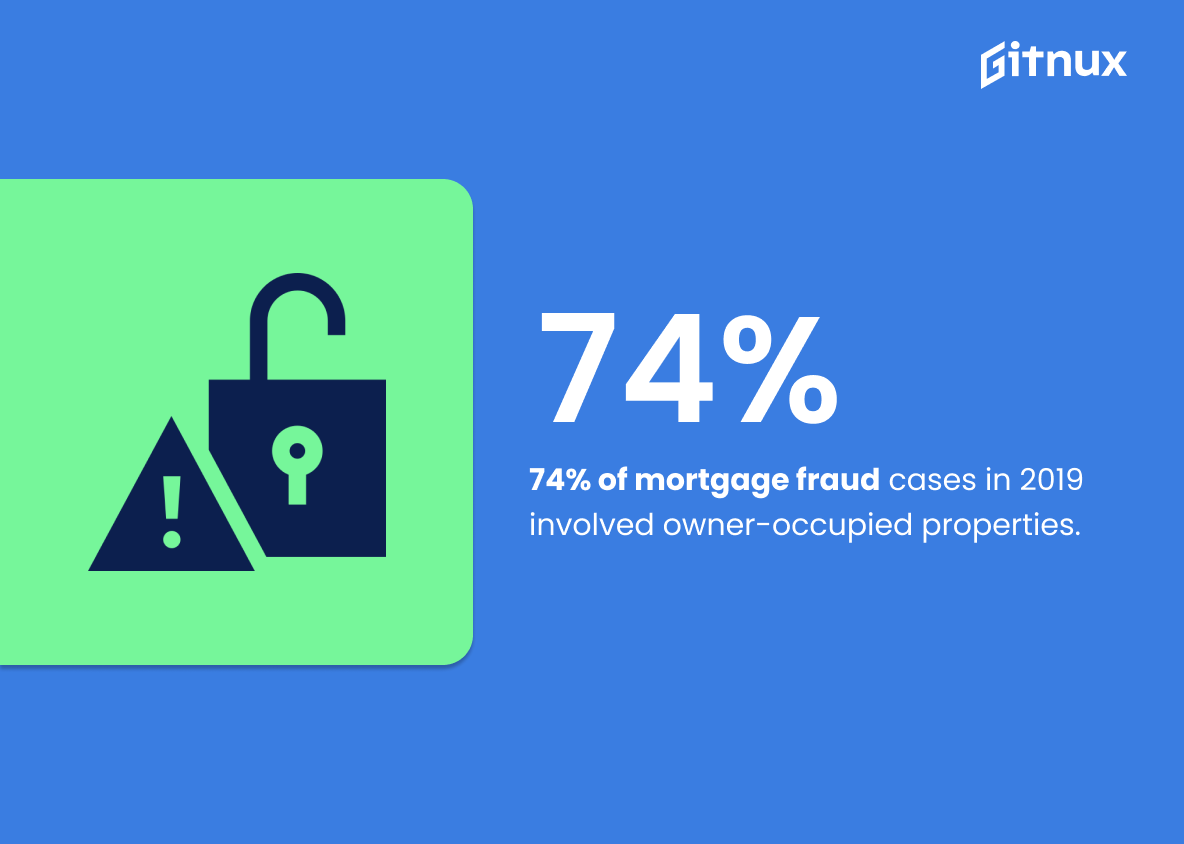

74% of mortgage fraud cases in 2019 involved owner-occupied properties.

This statistic is a stark reminder of the prevalence of mortgage fraud in 2019, particularly when it comes to owner-occupied properties. It highlights the need for homeowners to be aware of the potential risks associated with mortgage fraud and to take steps to protect themselves. It also serves as a warning to lenders to be vigilant in their screening processes and to take extra precautions when dealing with owner-occupied properties.

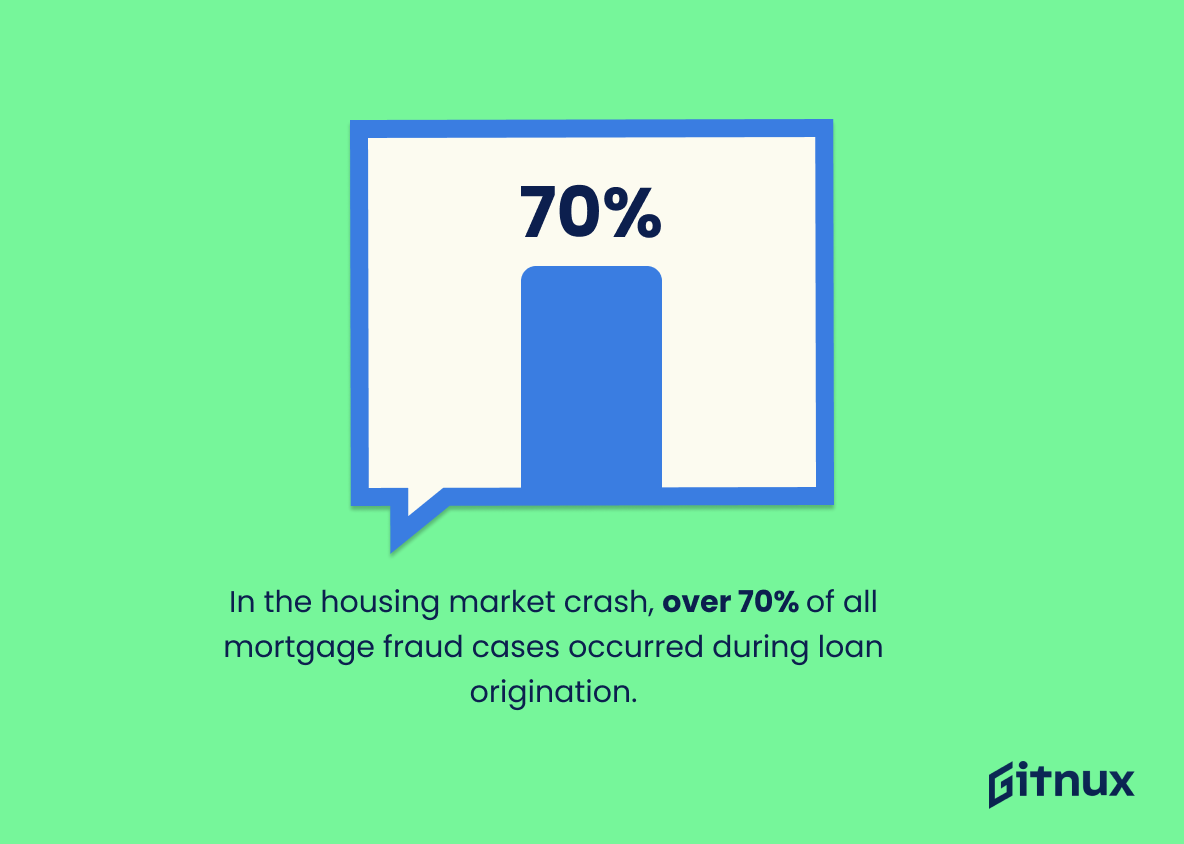

In the housing market crash, over 70% of all mortgage fraud cases occurred during loan origination.

This statistic is a stark reminder of the prevalence of mortgage fraud during the housing market crash. It highlights the importance of ensuring that loan origination processes are conducted with the utmost integrity and diligence, as this is where the majority of fraudulent activity occurred. It serves as a warning to potential borrowers and lenders alike that mortgage fraud is a real and present danger, and that extra caution must be taken to ensure that all parties involved are protected.

In 2018, a total of $3.3 billion in mortgage fraud was stopped by financial institutions.

This statistic is a stark reminder of the prevalence of mortgage fraud in our society. It highlights the importance of financial institutions in preventing such fraud from occurring, and the need for continued vigilance in order to protect consumers from becoming victims of this type of crime. It also serves as a warning to potential perpetrators that their actions will not go unnoticed.

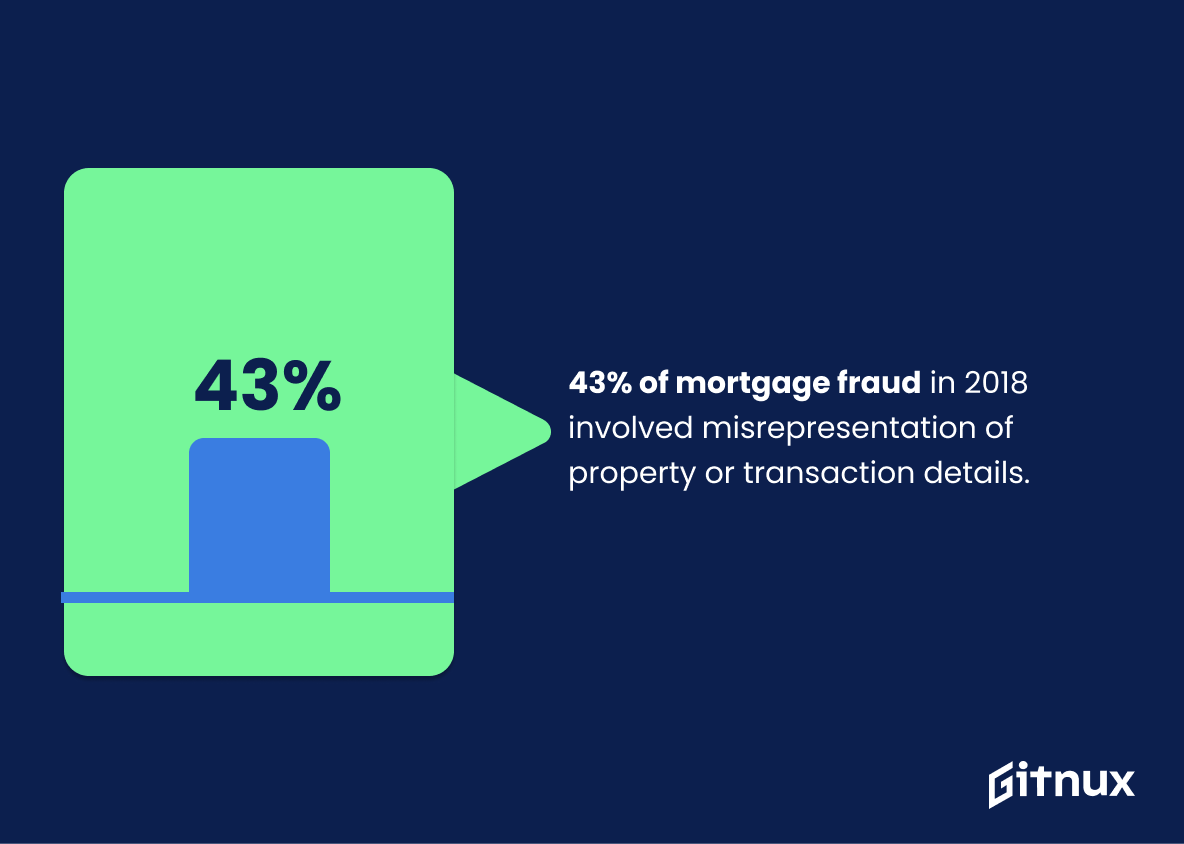

43% of mortgage fraud in 2018 involved misrepresentation of property or transaction details.

This statistic is a stark reminder of the prevalence of mortgage fraud in 2018, with nearly half of all cases involving misrepresentation of property or transaction details. It serves as a warning to potential buyers and lenders to be extra vigilant when it comes to mortgage transactions, as even the smallest detail can have a major impact.

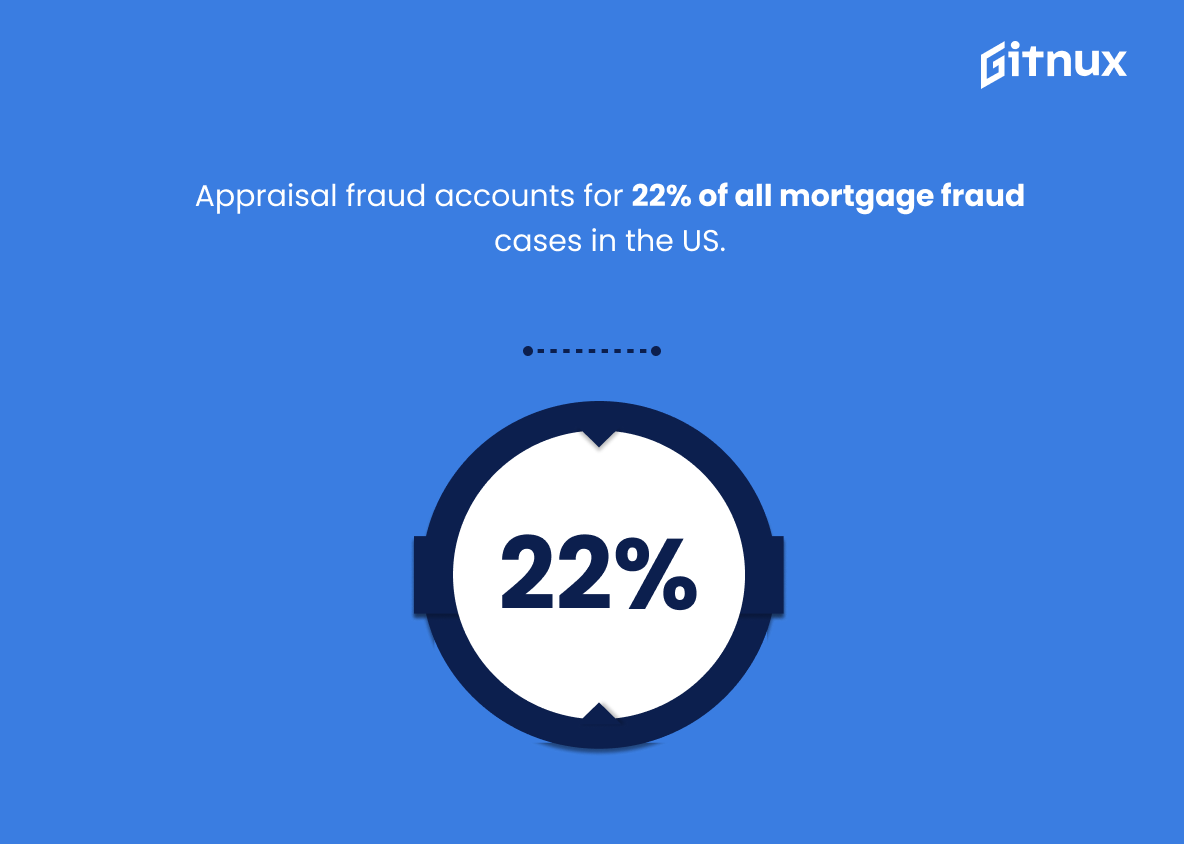

Appraisal fraud accounts for 22% of all mortgage fraud cases in the US.

This statistic is a stark reminder of the prevalence of appraisal fraud in the US mortgage market. It highlights the need for increased vigilance and oversight to ensure that mortgage fraud does not become a more widespread problem. It also serves as a warning to potential borrowers to be aware of the risks associated with mortgage fraud and to take steps to protect themselves.

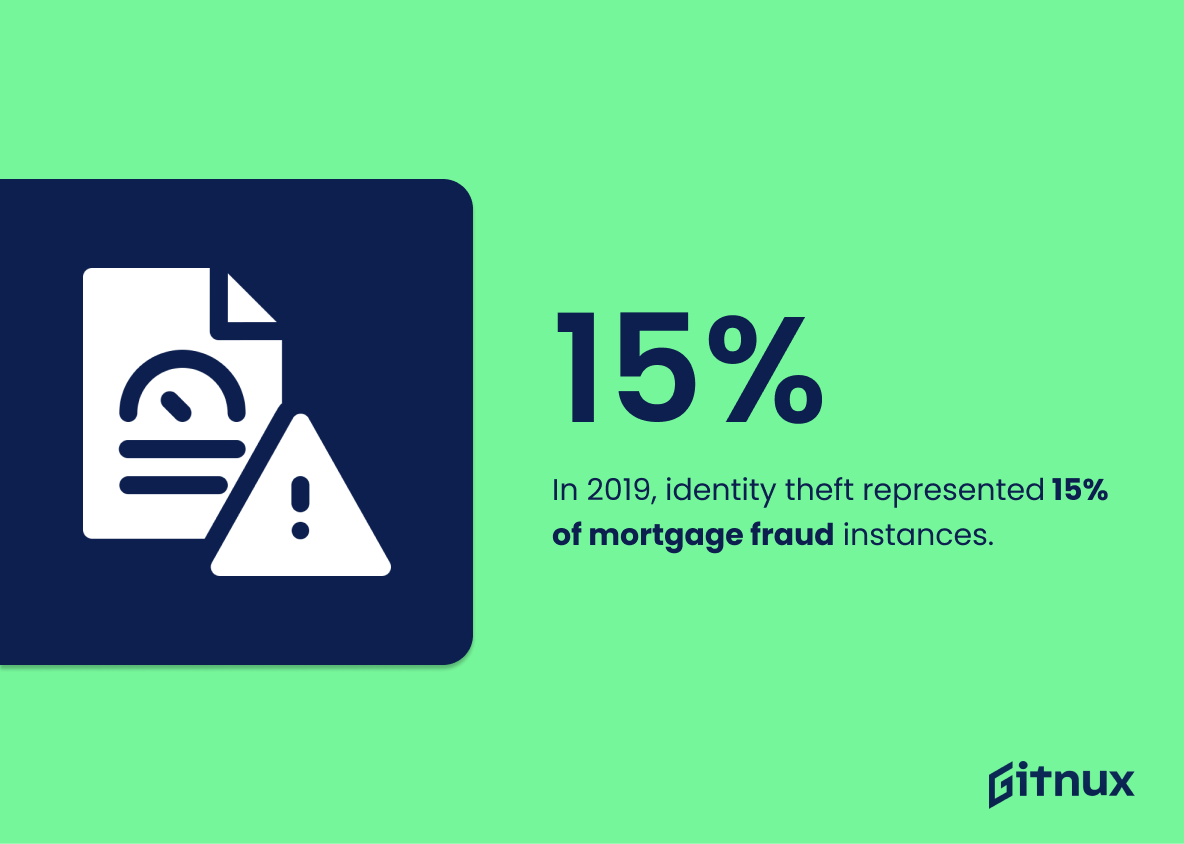

In 2019, identity theft represented 15% of mortgage fraud instances.

This statistic is a stark reminder of the prevalence of identity theft in mortgage fraud cases. It highlights the importance of taking extra precautions to protect one’s identity when applying for a mortgage. It also serves as a warning to lenders to be vigilant in verifying the identity of their applicants. By understanding the extent of identity theft in mortgage fraud cases, lenders can better equip themselves to prevent such fraud from occurring.

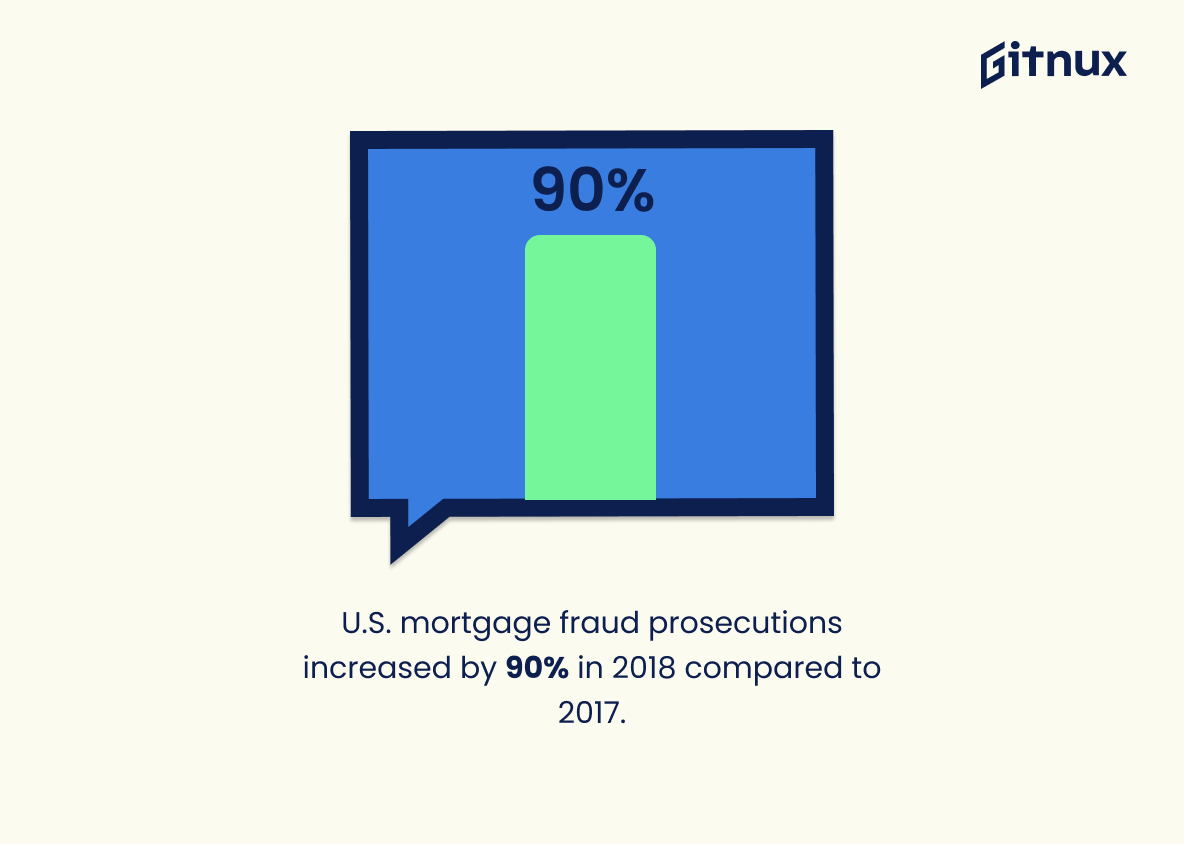

U.S. mortgage fraud prosecutions increased by 90% in 2018 compared to 2017.

This statistic is a stark reminder of the growing prevalence of mortgage fraud in the United States. It highlights the need for increased vigilance and proactive measures to combat this type of criminal activity. The 90% increase in prosecutions in 2018 compared to 2017 is a clear indication that more needs to be done to protect homeowners and lenders from the devastating effects of mortgage fraud.

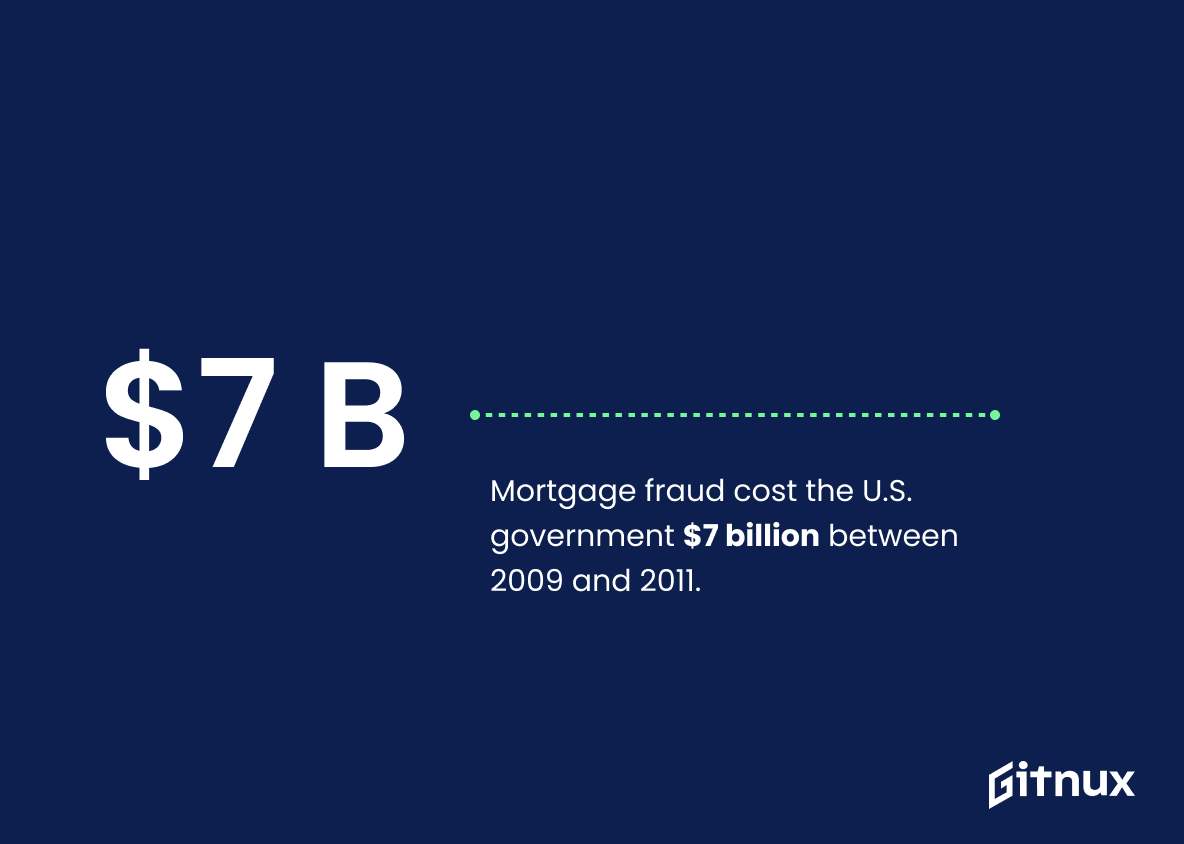

Mortgage fraud cost the U.S. government $7 billion between 2009 and 2011.

This statistic is a stark reminder of the immense financial burden that mortgage fraud has placed on the U.S. government over the past few years. It serves as a powerful illustration of the need for increased vigilance and enforcement when it comes to preventing and prosecuting mortgage fraud.

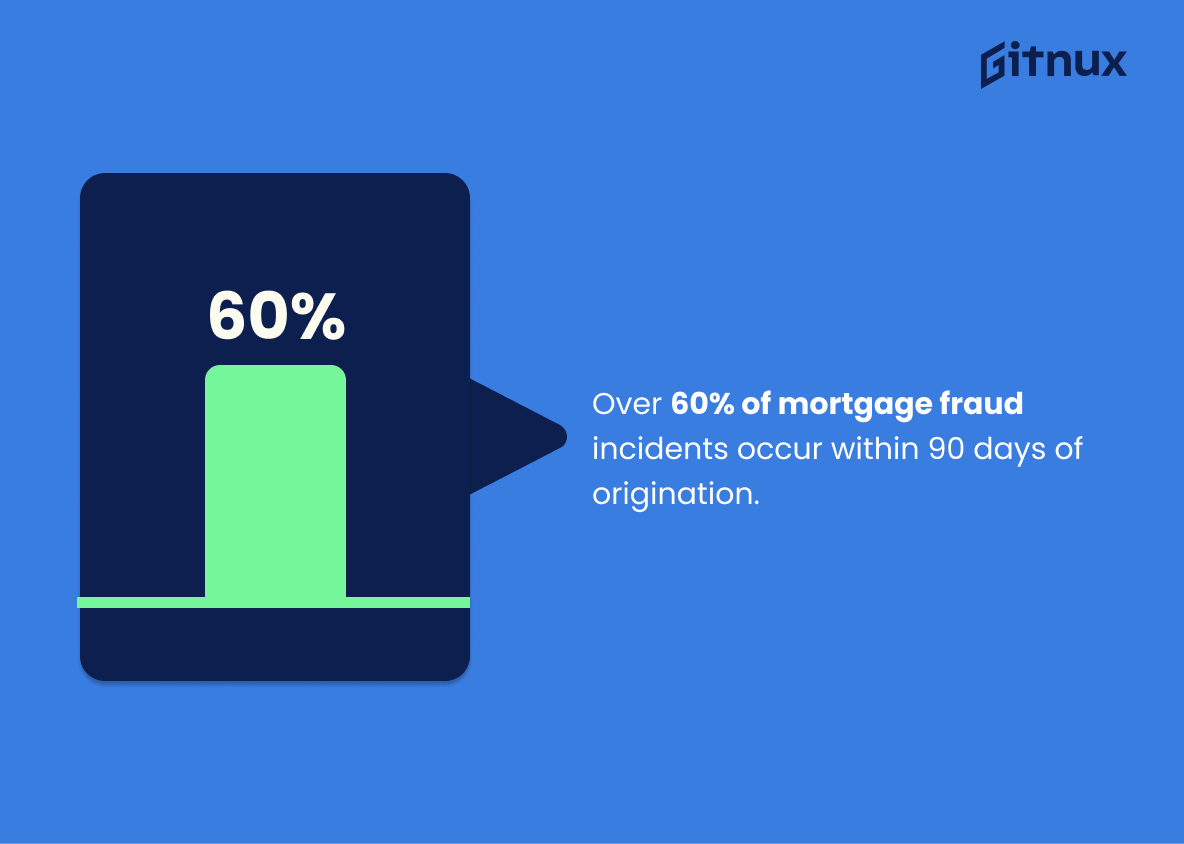

Over 60% of mortgage fraud incidents occur within 90 days of origination.

This statistic is a stark reminder of the urgency of addressing mortgage fraud. It highlights the need for lenders to be vigilant in the early stages of the loan process, as the majority of fraudulent activity takes place within the first three months. This underscores the importance of having robust anti-fraud measures in place from the outset, as well as ongoing monitoring throughout the life of the loan.

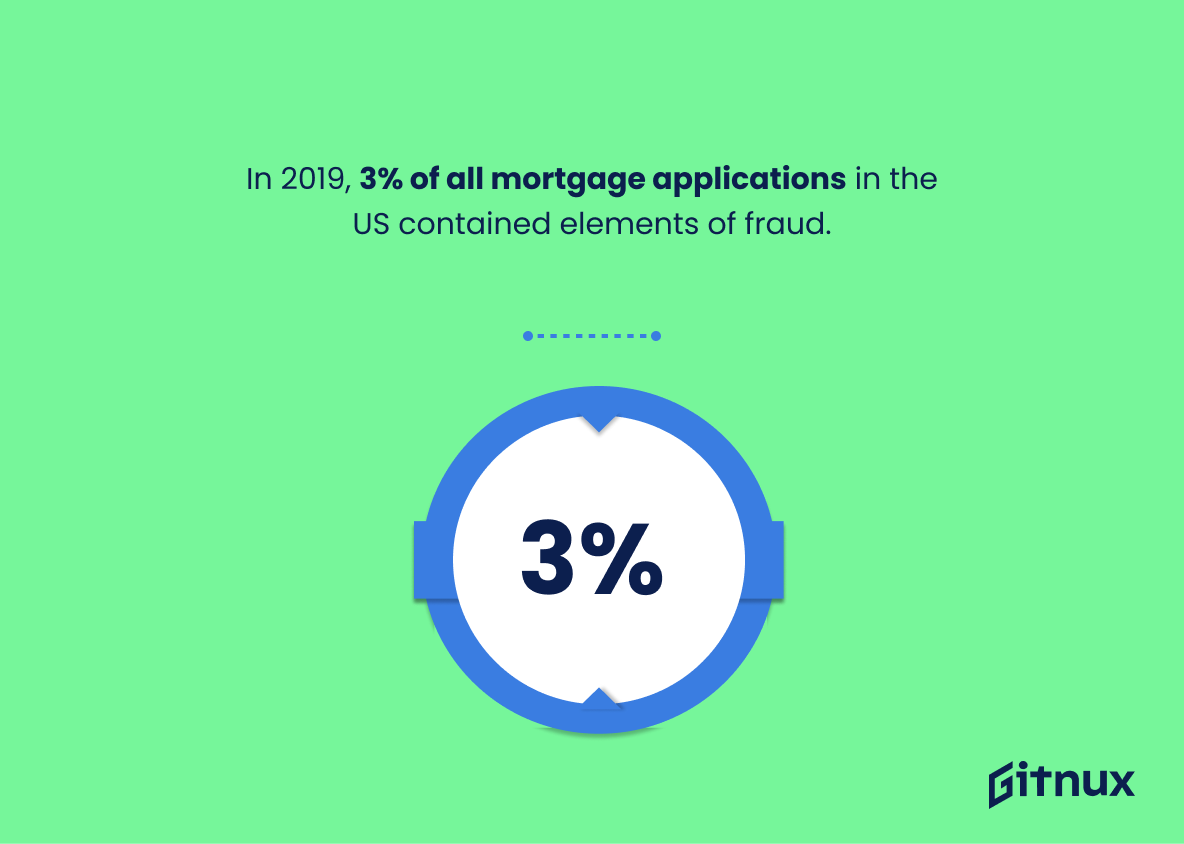

In 2019, 3% of all mortgage applications in the US contained elements of fraud.

This statistic is a stark reminder of the prevalence of mortgage fraud in the US. It highlights the need for vigilance and proactive measures to protect against this type of criminal activity. It also serves as a warning to potential borrowers to be aware of the risks associated with mortgage applications and to take steps to ensure their applications are legitimate.

In the first quarter of 2020, FinCEN reported over 1,200 cases of mortgage fraud.

This statistic is a stark reminder of the prevalence of mortgage fraud in the first quarter of 2020. It highlights the need for vigilance and awareness of the potential for fraudulent activity in the mortgage industry. It also serves as a warning to potential borrowers to be aware of the risks associated with taking out a mortgage loan. The high number of reported cases of mortgage fraud in the first quarter of 2020 is a cause for concern and should be taken seriously.

Conclusion

Mortgage fraud is a serious issue that has been on the rise in recent years. According to statistics from various sources, it is estimated that the United States loses between $1-10 billion per year due to mortgage fraud and there was an increase of 938% in suspicious activity reports of mortgage fraud from 2019 to 2020. CoreLogic reported a 12.4% year-over-year increase in mortgage fraud risk for 2018 and Florida ranked first with a Risk Index value of 292 for 2020. Mortgage cases resulted in an average loss of $1.2 million among financial institutions while income fraud represented over 30% of fraudulent applications during 2020 according to Fannie Mae’s report.

The Federal Reserve estimates that between 600,000 and 1,200,000 homeowners experienced mortgage fraud last year while 74% involved owner occupied properties according to MBA’s research data . There was also 10.7 % growth rate observed from 2016 – 2017 as well as 3 %of all US mortgages containing elements of Fraud by 2019 end . In addition , FinCEN reported more than 1200 cases related with Mortgage Fraud alone during Q1/2020 which shows how rampant this problem has become across America today . It is clear then that steps must be taken immediately if we are going prevent further losses caused by this crime wave sweeping our nation

References

0. – https://www.www.mortgagefraudblog.com

1. – https://www.www.jdjournal.com

2. – https://www.www.americanbar.org

3. – https://www.www.financialsamurai.com

4. – https://www.www.federalreserve.gov

5. – https://www.www.fanniemae.com

6. – https://www.www.prnewswire.com

7. – https://www.www.fbi.gov

8. – https://www.www.entrepreneur.com

9. – https://www.loanofficerhub.com

10. – https://www.www.mba.org

11. – https://www.lexisnexisrisk.com

12. – https://www.www.corelogic.com

13. – https://www.www.fincen.gov

14. – https://www.realtytimes.com

15. – https://www.www.creditkarma.com