Mortgage default rates are an important indicator of the health of a country’s economy. In this blog post, we will be exploring mortgage default rate statistics from around the world to gain insight into how different countries have been affected by economic downturns and pandemics in recent years. We’ll look at data from the US, South Africa, Ireland, Western Australia, Canada and Spain as well as other regions within these countries. Additionally, we’ll examine factors such as loan type and borrower demographics that can influence mortgage defaults. By understanding current trends in mortgage defaults across various nations and regions worldwide, it is possible to better prepare for potential future financial crises or recessions.

The statistic of the mortgage default rate in the US in Q4 2020 being 0.69% is a crucial indicator of the health of the US housing market. It provides insight into the financial stability of homeowners and the ability of lenders to provide mortgages. This statistic is a valuable tool for understanding the current state of the housing market and can be used to inform decisions about future investments.

Mortgage default rates hit a low of 0.4% in 2020 Q1 before the pandemic.

This statistic is a testament to the strength of the mortgage market before the pandemic, highlighting the fact that even in a time of economic uncertainty, the mortgage market was able to remain stable. It serves as a benchmark for comparison to the current mortgage default rate, which can be used to measure the impact of the pandemic on the mortgage market.

Mortgage Default Rate Statistics Overview

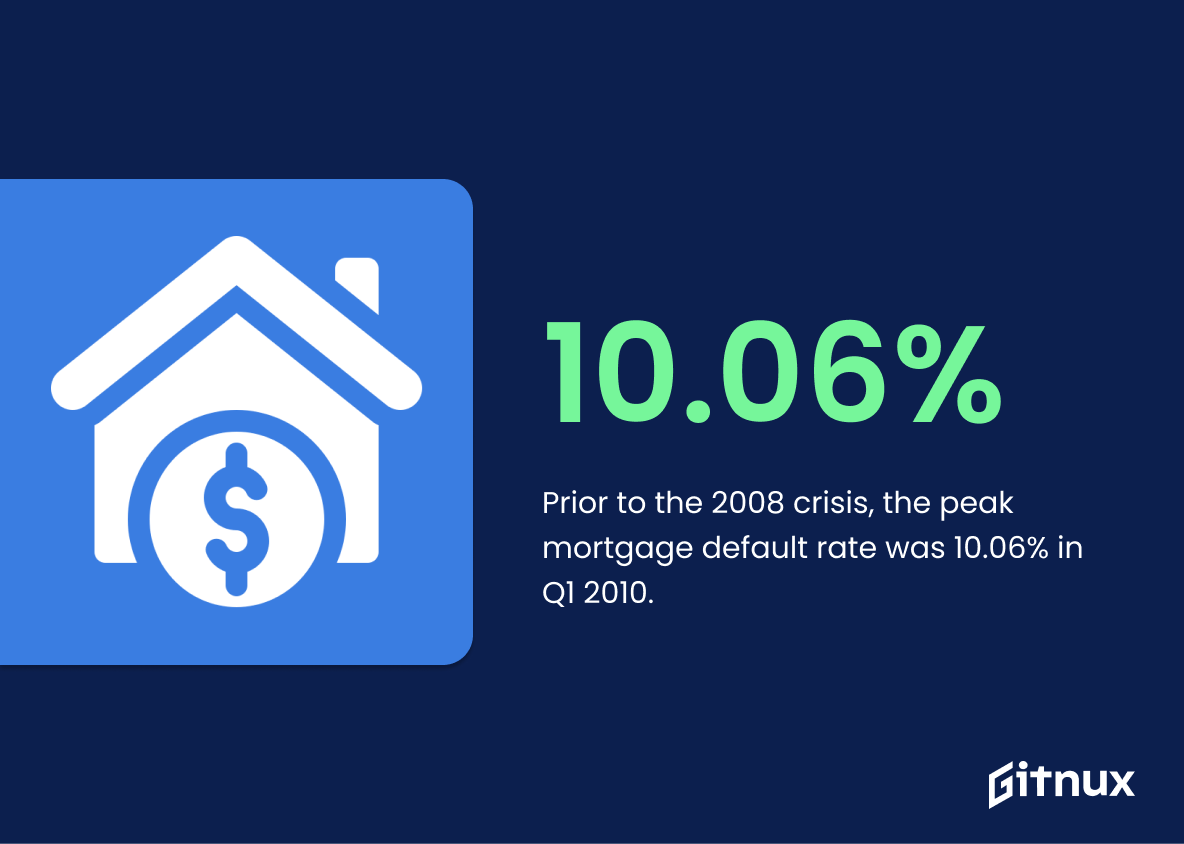

Prior to the 2008 crisis, the peak mortgage default rate was 10.06% in Q1 2010.

This statistic serves as a stark reminder of the devastating effects of the 2008 crisis on the mortgage default rate. It highlights the fact that the rate had reached its highest point in the aftermath of the crisis, demonstrating the far-reaching implications of the economic downturn.

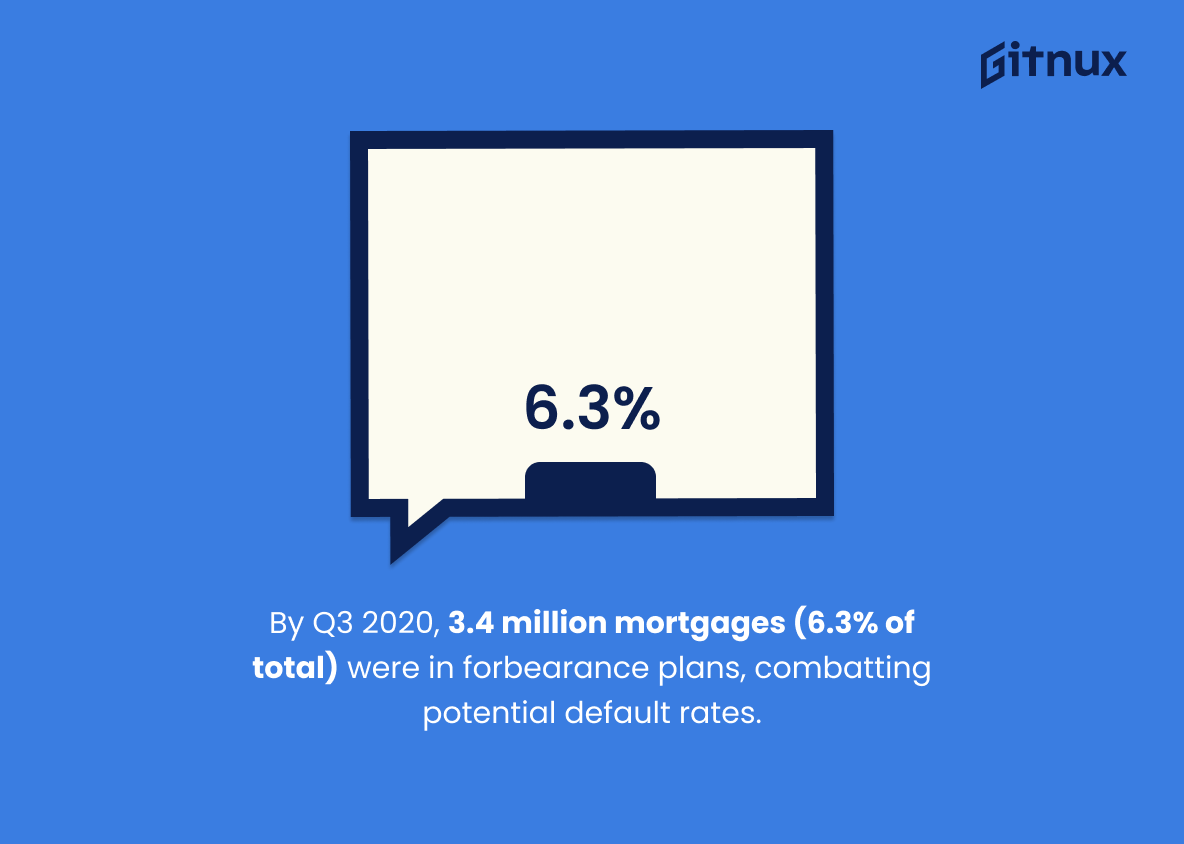

By Q3 2020, 3.4 million mortgages (6.3% of total) were in forbearance plans, combatting potential default rates.

This statistic is a crucial indicator of the success of efforts to combat potential default rates. It shows that, despite the economic downturn caused by the pandemic, 3.4 million mortgages have been able to stay afloat through forbearance plans. This is a testament to the effectiveness of these plans in helping to keep people in their homes and preventing a surge in mortgage defaults.

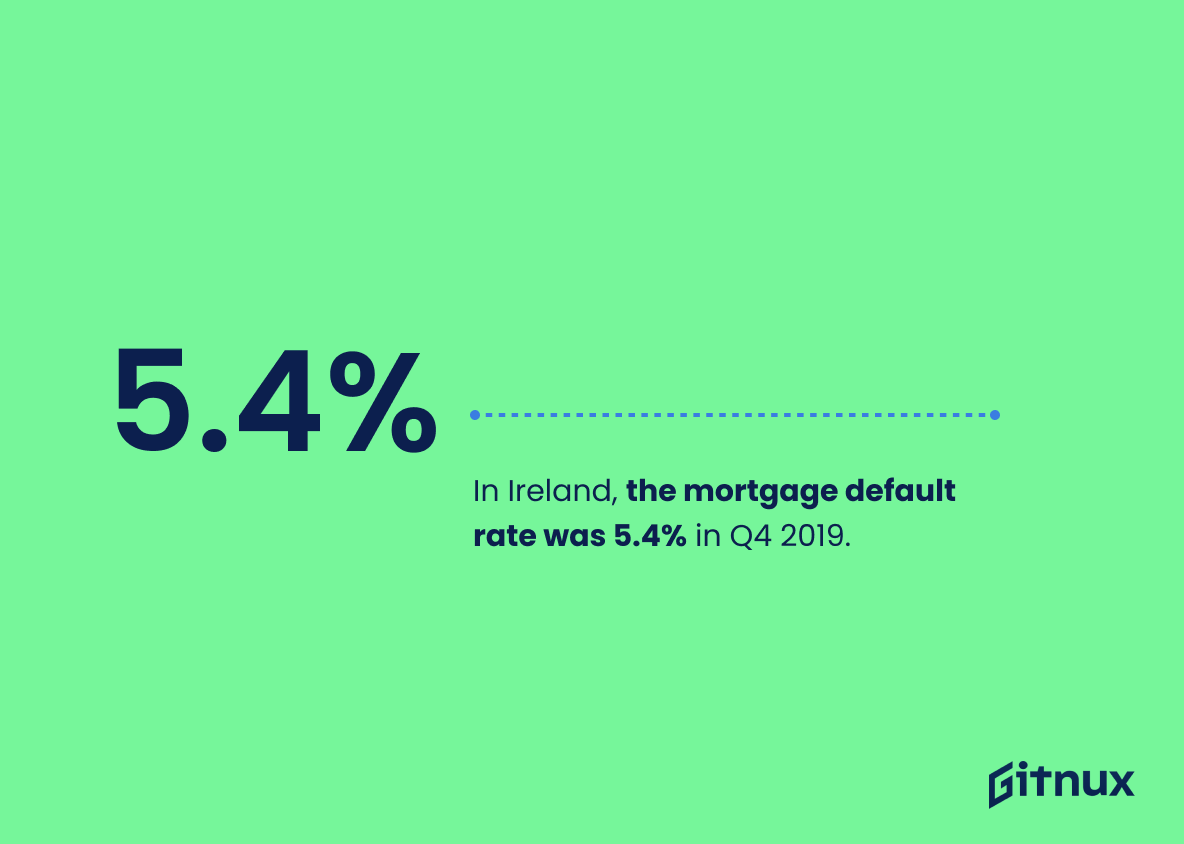

In Ireland, the mortgage default rate was 5.4% in Q4 2019.

The statistic of Ireland’s mortgage default rate in Q4 2019 is a crucial indicator of the country’s economic health. It provides insight into the ability of individuals and businesses to meet their financial obligations, and can be used to gauge the overall stability of the housing market. By understanding the mortgage default rate, we can better understand the financial health of the country and make more informed decisions about our own investments.

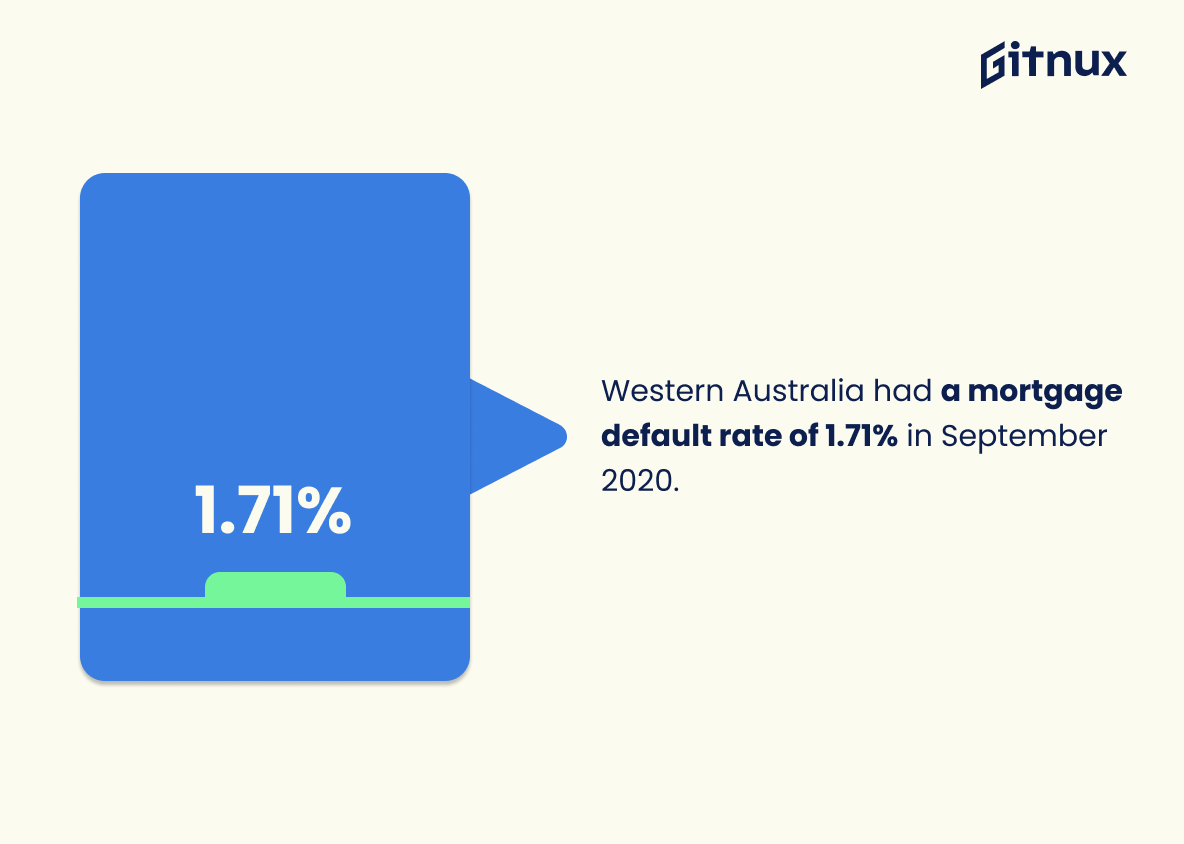

Western Australia had a mortgage default rate of 1.71% in September 2020.

The statistic of Western Australia’s mortgage default rate of 1.71% in September 2020 is a crucial indicator of the state’s financial health. It provides insight into the stability of the housing market and the ability of homeowners to meet their financial obligations. This data can be used to inform decisions about the future of the housing market, as well as to assess the effectiveness of current policies and regulations. Furthermore, it can be used to compare the mortgage default rate of Western Australia to other states and countries, providing a valuable benchmark for comparison.

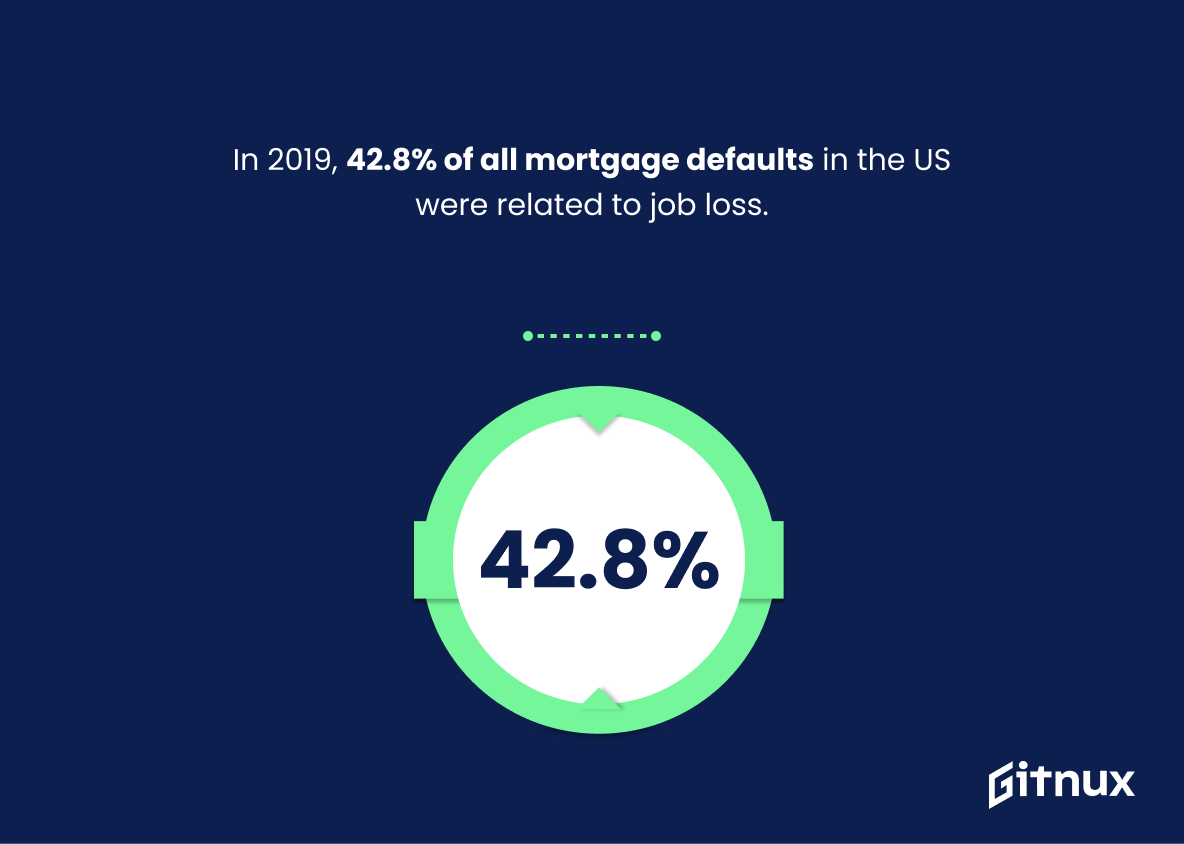

In 2019, 42.8% of all mortgage defaults in the US were related to job loss.

This statistic is a stark reminder of the fragility of the US economy and the vulnerability of homeowners. It highlights the importance of having a stable job and income in order to avoid defaulting on a mortgage. It also serves as a warning to potential homeowners to be aware of the risks associated with taking out a mortgage and to be prepared for the possibility of job loss.

FHA-backed loans had a default rate of 2.07% in Q4 2020.

The fact that FHA-backed loans had a default rate of 2.07% in Q4 2020 is a testament to the strength of the mortgage market. This low rate of default indicates that borrowers are taking on mortgages responsibly and that lenders are providing loans that are appropriate for the borrower’s financial situation. This is a positive sign for the housing market and a sign that the economy is on the right track.

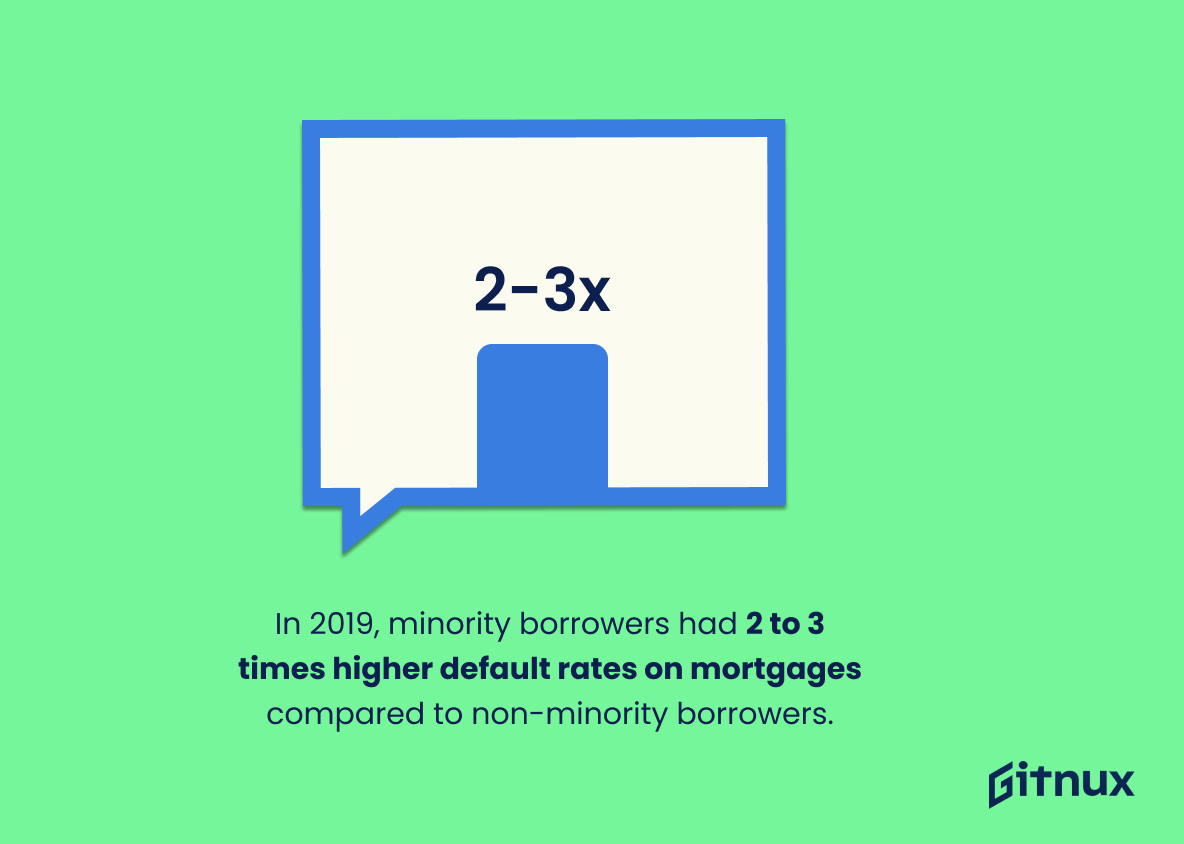

In 2019, minority borrowers were more likely to default on mortgages than non-minority borrowers, with default rate differences being 2 to 3 times higher.

This statistic is a stark reminder of the systemic inequalities that exist in the mortgage industry. It highlights the fact that minority borrowers are disproportionately affected by default rates, with the gap between them and non-minority borrowers being two to three times higher. This is a concerning issue that needs to be addressed, as it could have long-term implications for the financial security of minority borrowers.

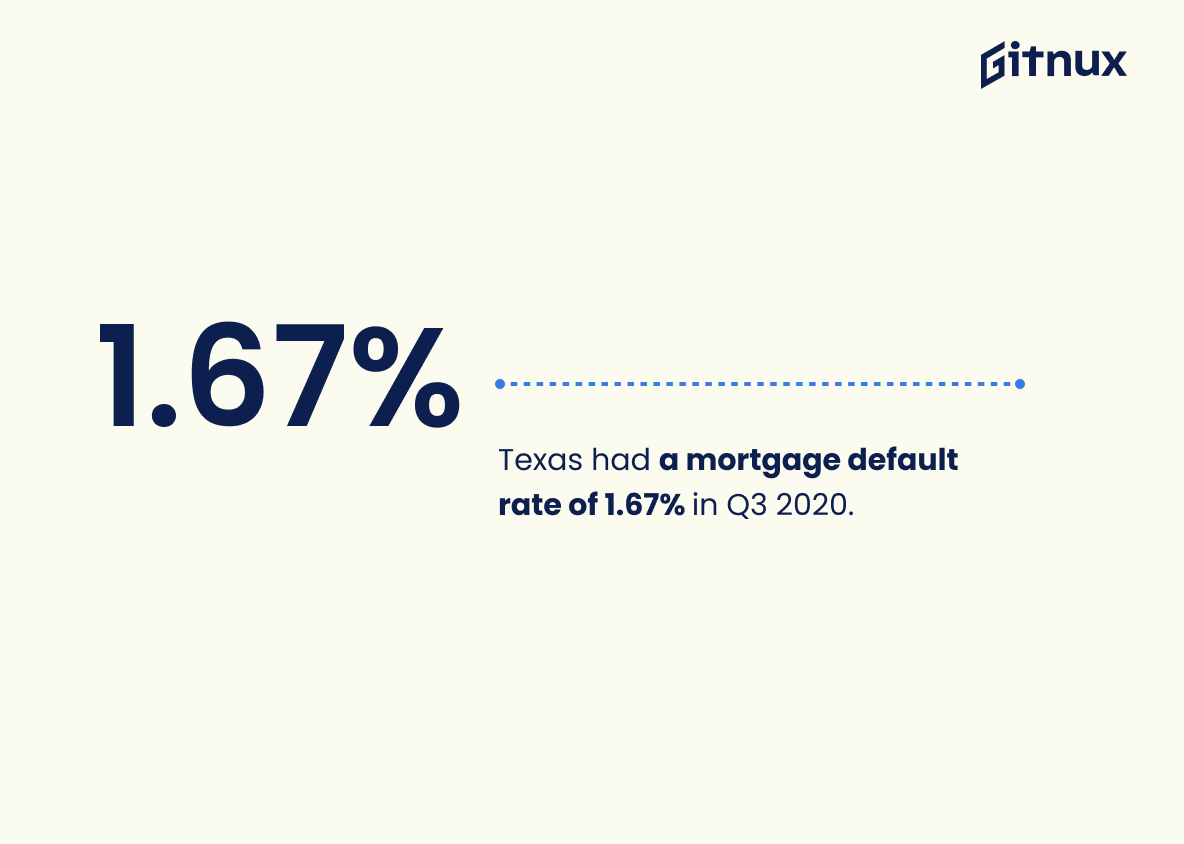

Texas had a mortgage default rate of 1.67% in Q3 2020.

The statistic of Texas having a mortgage default rate of 1.67% in Q3 2020 is a crucial piece of information when discussing mortgage default rate statistics. It provides a snapshot of the current state of the housing market in Texas, and can be used to compare the mortgage default rate in Texas to other states or to the national average. This statistic can also be used to identify trends in the housing market, such as whether the mortgage default rate is increasing or decreasing over time. Furthermore, this statistic can be used to inform policy decisions related to the housing market, such as whether to implement measures to reduce the mortgage default rate.

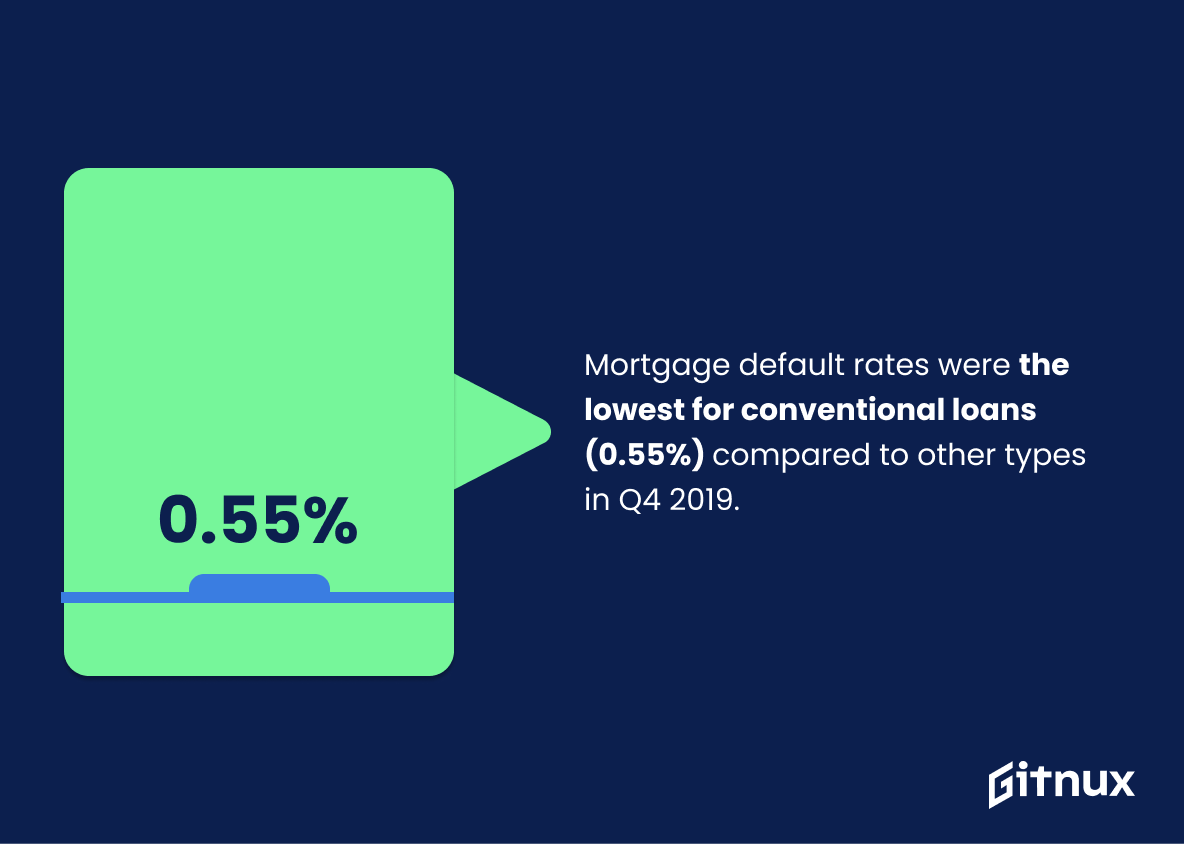

Mortgage default rates were the lowest for conventional loans (0.55%) compared to other types in Q4 2019.

This statistic is significant in the context of Mortgage Default Rate Statistics because it demonstrates that conventional loans are the most reliable option for borrowers. With a default rate of 0.55%, conventional loans are the safest bet for those looking to secure a mortgage. This statistic is a testament to the stability of conventional loans and provides assurance to potential borrowers that they are making a sound investment.

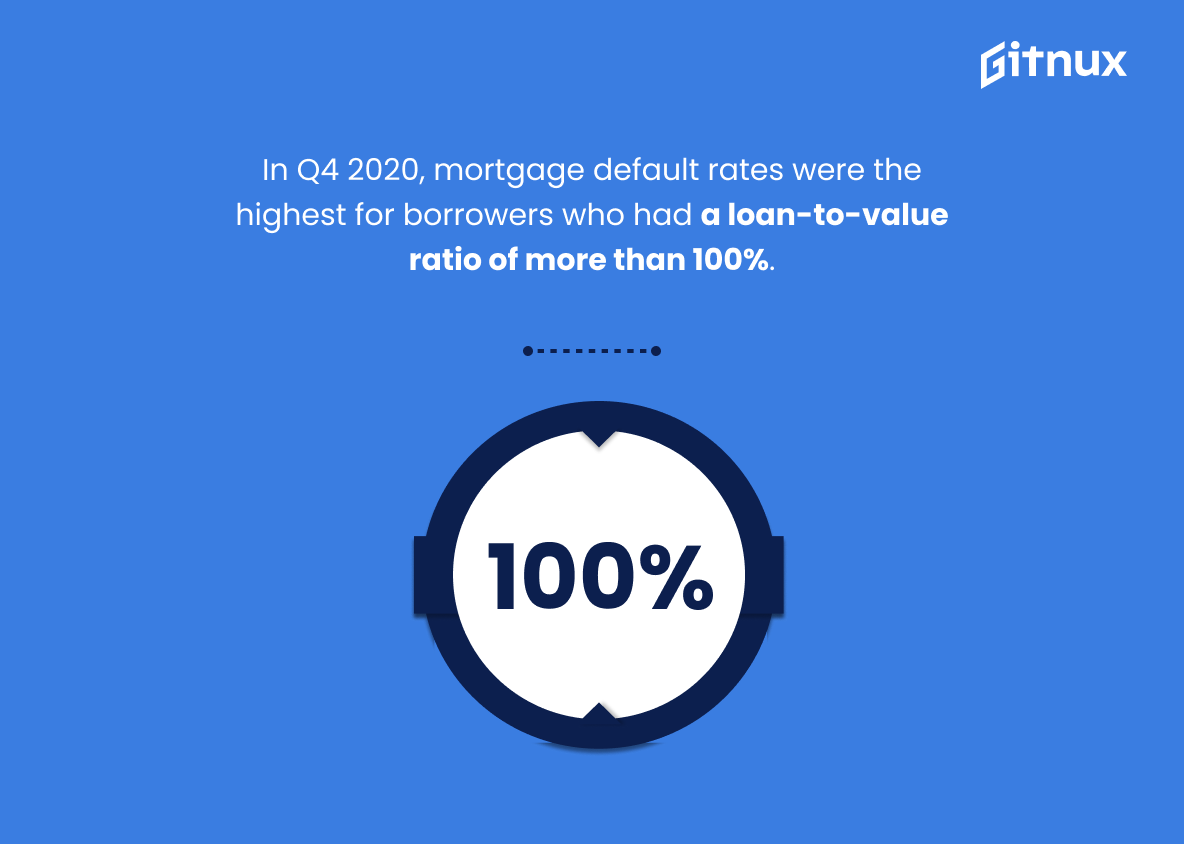

In Q4 2020, mortgage default rates were the highest for borrowers who had a loan-to-value ratio of more than 100%.

This statistic is a telling indicator of the financial health of borrowers with a loan-to-value ratio of more than 100%. It suggests that these borrowers are more likely to default on their mortgages, which could have serious implications for their financial stability. This statistic is important to consider when discussing mortgage default rate statistics, as it provides insight into the financial health of a particular segment of borrowers.

Rural areas reported a 5.5% mortgage default rate as of June 2020.

This statistic is a telling indication of the financial health of rural areas, as of June 2020. It provides insight into the number of people who are unable to keep up with their mortgage payments, and the potential economic impact this could have on the area. This data can be used to inform policy decisions and help identify areas that may need additional support. Additionally, it can be used to compare the mortgage default rate of rural areas to other areas, providing a more comprehensive picture of the overall mortgage default rate.

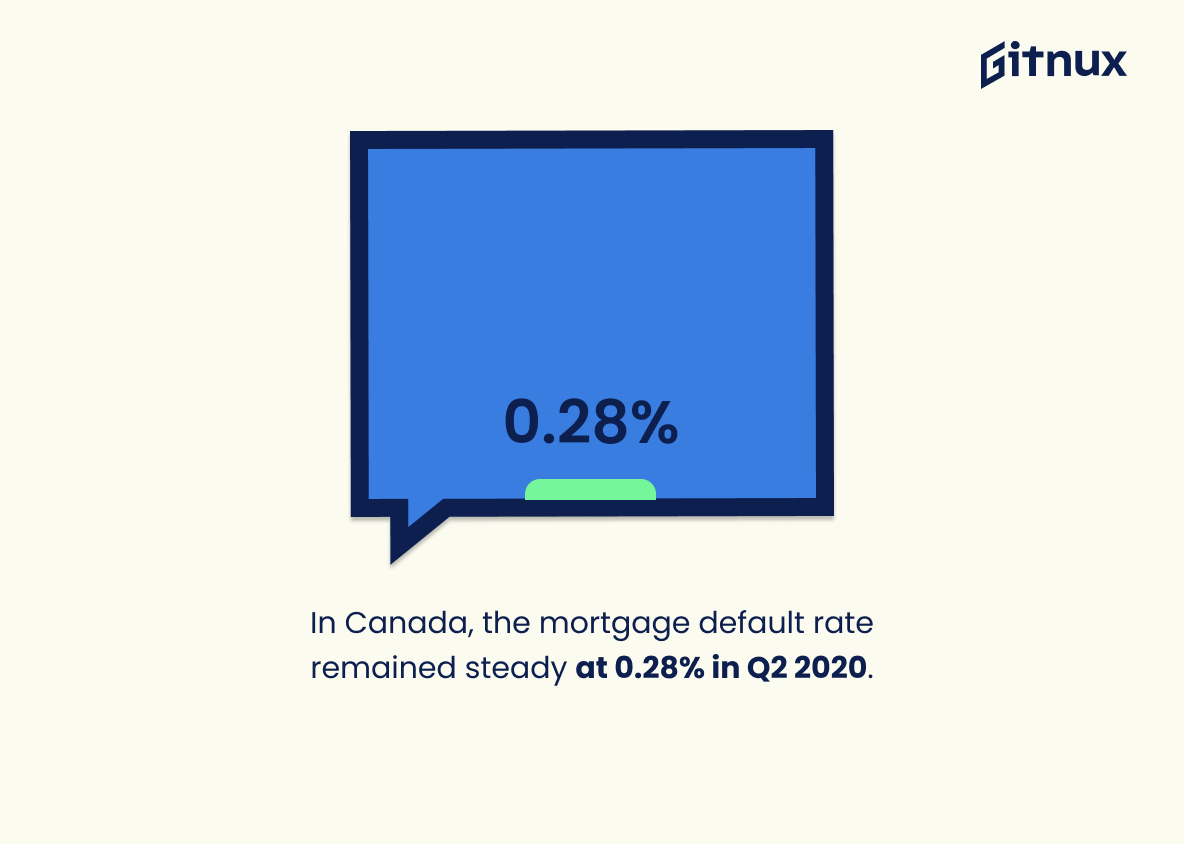

In Canada, the mortgage default rate remained steady at 0.28% in Q2 2020.

The fact that the mortgage default rate in Canada remained steady at 0.28% in Q2 2020 is a testament to the resilience of the Canadian economy in the face of the global pandemic. This statistic is a reminder that, despite the economic uncertainty, Canadians are still managing to keep up with their mortgage payments. This is a positive sign for the future of the Canadian housing market and a sign of hope for those looking to purchase a home.

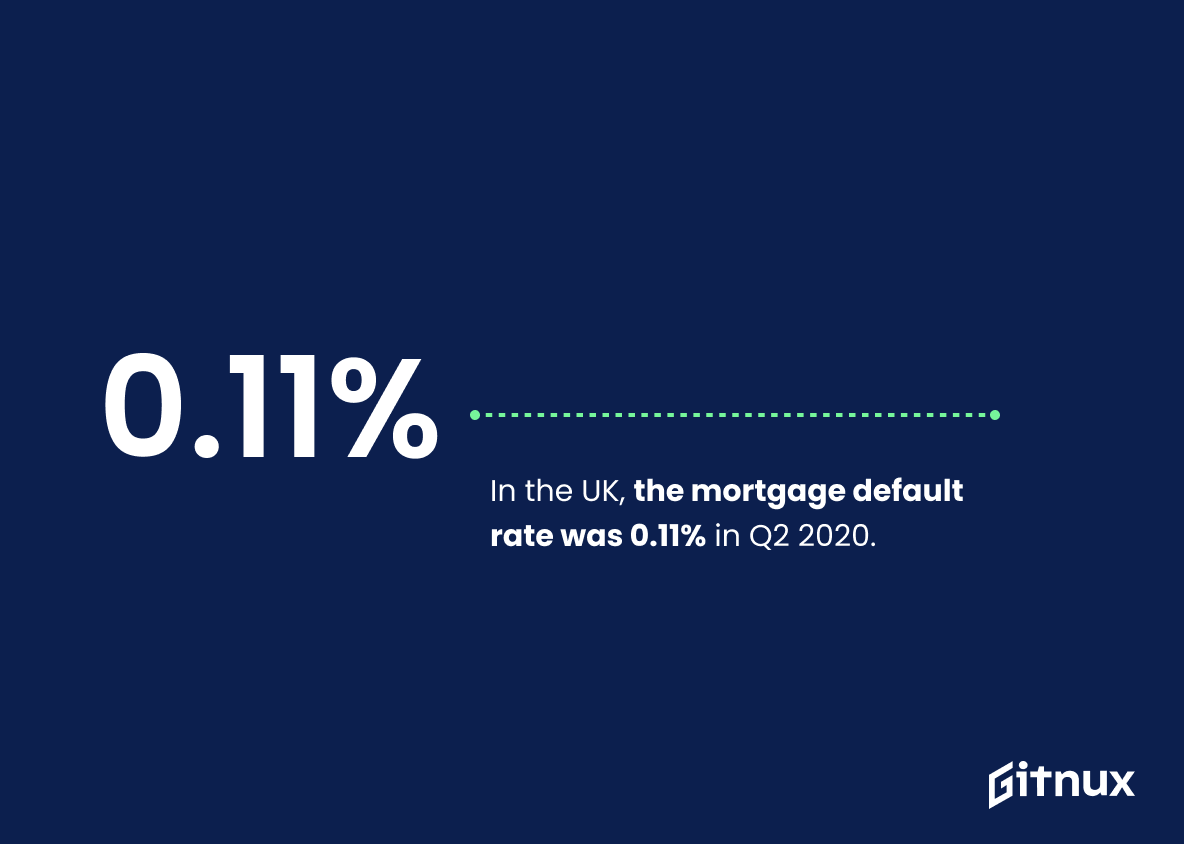

In the UK, the mortgage default rate was 0.11% in Q2 2020.

The Q2 2020 mortgage default rate of 0.11% in the UK is a testament to the strength of the country’s economy and the resilience of its citizens. This low rate of default indicates that borrowers are able to meet their financial obligations and that lenders are able to provide the necessary funds to support them. This statistic is a valuable insight into the current state of the mortgage market and provides a useful benchmark for comparison with other countries.

Conclusion

The data presented in this blog post shows that mortgage default rates vary significantly across countries and regions. In the US, the rate was 0.69% in Q4 2020, while South Africa experienced a 5.5% rate during the same period – one of the highest among all loan types globally. The UK had an exceptionally low default rate of 0.11%, whereas Spain’s stood at 5%. Additionally, job loss has been identified as a major cause for defaults among prime borrowers in 2019 (42.8%). Forbearance plans have also helped to combat potential defaults by providing relief to millions of homeowners affected by COVID-19 pandemic related financial challenges since March 2020 (3.4 million mortgages). It is clear from these statistics that there are many factors influencing mortgage default rates around the world and it will be interesting to observe how they evolve over time with changing economic conditions and policies implemented by governments worldwide

References

0. – https://www.www.urban.org

1. – https://www.www.mfaa.com.au

2. – https://www.www.housingwire.com

3. – https://www.www.canadianmortgagetrends.com

4. – https://www.www.mba.org

5. – https://www.www.statista.com

6. – https://www.fred.stlouisfed.org

7. – https://www.www.corelogic.com

8. – https://www.www.consumerfinance.gov

9. – https://www.www.sifma.org

10. – https://www.www.myhome.ie